Back to the Beginning

The creation story of IFRS 17 for insurance contracts June/July 2017Author’s Note: This is a condensed history of the International Accounting Standards Board’s (IASB’s) Insurance Contracts project. Not every issue is discussed completely herein or in some cases at all, nor is every milestone noted. For a more complete history, visit the IASB website.

In the beginning, the International Accounting Standards Board (IASB) created International Financial Reporting Standards (IFRS). No international standards existed, and it was chaos across the face of the earth. Users saw a great darkness in insurance reporting, from which useful information could not be derived.

It seemed that each country had its own set of standards for public reporting, and it was not obvious how to compare one company’s reporting with another. Those companies listed on the New York Stock Exchange were required to report their results using U.S. generally accepted accounting principles (GAAP), while companies listed on non-U.S. stock exchanges used whatever standards those exchanges required. For many of the largest companies, therefore, U.S. GAAP became the de facto standard for insurance reporting, but there was still no generally accepted international standard.

Early Steps—The DSOP

The establishment of the European Union (EU) in 1993 changed everything and created the need for a common international accounting standard. One of the early decisions the EU made was that all companies listed on a European stock exchange needed to report using International Accounting Standards, as the work of the International Accounting Standards Committee (IASC), the predecessor to the IASB, was called.

The IASC took up the insurance project in 1997. It produced two sets of papers, the first being a two-volume paper on insurance issues, and the second known as the Draft Standards of Practice for insurance accounting, or DSOPs. The DSOPs, based on comments received on the insurance issues papers, were an incomplete standard, lacking, among other things, a proposal for participating contracts. Nevertheless, they set the stage for the lengthy process that eventually produced a final standard.

The DSOP proposed accounting for insurance using a fair value principle. The liability for each contract was to be equal to the present value of future cash flows using market assumptions, including a current interest rate curve. This caused great concern among interested parties for a variety of reasons.

First, it allowed a gain to be recognized at issue for every profitable contract sold. The markets were just recovering from problems at companies like Enron that recognized profits on issue of contracts that eventually turned out to be unprofitable. In the view of many users, recognizing the present value of all future profits immediately on issue created the opportunity for serious manipulation by management because there was no way to determine a fair value except through the use of assumptions set by the company’s actuaries.

For their part, many actuaries were concerned about this proposal because it meant they needed to develop “market-based” assumptions when no such thing existed—or what did exist (e.g., those assumptions used for purchase accounting) would not be applicable to a specific company.

Companies also objected to the use of fair value since it seemed that it would create significant volatility in the earnings statement, as interest rates moved, sometimes significantly, between each reporting period. Companies were concerned that extensive volatility would cause analysts to downgrade their financial standing and reduce the value of their shares.

The Insurance Industry Response

In response to the formation of the EU, the IASB and the publication of the DSOPs, the European industry formed the CFO Forum (CFOF), a group of companies, each represented by its CFO. The CFOF worked initially on Solvency II, the new solvency regulation the EU was developing. It also produced a set of principles for deriving European embedded values (EEVs) that were put forth as an improvement over normal accounting reports.

Partly in response to the European formation of the CFOF, several large North American companies formed the Group of North American Insurance Entities (GNAIE), with the goal of presenting a common position on international accounting for insurance. In 2004, GNAIE published a set of accounting principles for long- and short-duration insurance contracts.

Eventually, members of the CFOF and GNAIE, together with the four largest Japanese life insurers, came together to form the HUB group. This group also prepared position papers on IASB proposals and eventually adopted common accounting principles that it presented to the IASB in 2005.1

The one area where consensus was not reached was on the issue of discounting claim reserves for short-duration contracts. From the beginning, U.S. property and casualty (P&C) insurers were quite happy with their current accounting system that used undiscounted calculations, whereas the European insurers were locked into a discounted system as part of Solvency II. Therefore, this issue is not addressed in the HUB group’s principles.

The Actuarial Profession’s Response

As noted, the actuarial profession was concerned about this project from the beginning. The International Actuarial Association (IAA) formed an Insurance Accounting Committee in 1997 to provide input to the IASC (and in turn the IASB), and provided valuable advice to the IASB throughout the course of the project. The American Academy of Actuaries (the Academy) also was heavily involved through its Financial Reporting Committee.

Early on, it was a challenge for actuaries to prove that they had something valuable to say about accounting standards—many IASC and IASB board members initially thought that actuaries did whatever the companies told them to do. There was a belief that actuaries often manipulated the results according to their employers’ wishes. It was an important challenge that was only overcome through extensive discussion and very well thought-out comment papers.

For the remainder of the project, both the IAA and the Academy provided extensive and detailed comments on all exposure drafts, occasionally exceeding 20 pages in length. The primary concerns of both groups were:

- Avoiding creation of noneconomic earnings volatility—mainly by consistent measurement of assets and liabilities (this had important implications for defining the discount rate to be used)

- Developing guidance both for accountants and actuaries that would be practical for preparers to implement in a cost-effective way

- Providing users with the information they need without simply producing numbers for numbers sake

Both groups had personal meetings with staff and board members to explain their positions and educate the boards and staff on the importance of actuarial science to the insurance business in general, and to accounting in particular.

The Development of IFRS 4

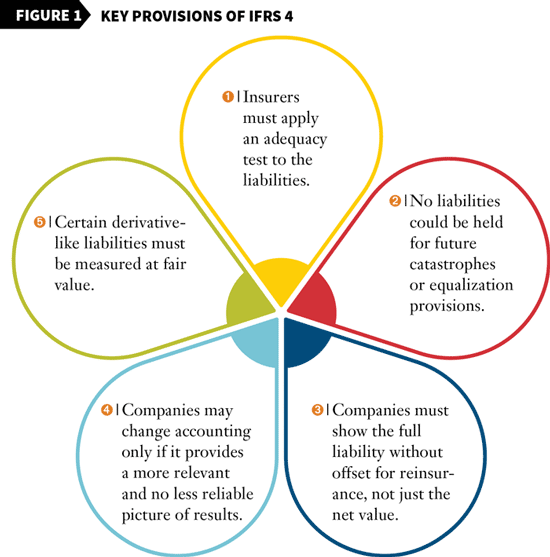

In light of the evident lack of agreement among the IASB, users and insurers, the IASB recognized the need to come up with a stopgap standard to meet the EU’s target of using International Accounting Standards by 2005. This standard, IFRS 4, adopted March 31, 2004, essentially said that companies could continue to use whatever standard they had been using with a number of exceptions. See Figure 1 for the most important of those exceptions.

Phase II of the Insurance Contracts Accounting Project

The IASB officially reopened the Insurance Contracts Project in 2005, producing an Issues Paper in May 2007. The Issues Paper reflected not only the DSOP, but also presentations and proposals made by the CFOF, GNAIE, IAA and the Academy, as well as other groups.

To facilitate discussion of the various issues, the ISAB created an Insurance Working Group (IWG) consisting of roughly 20 members from the user and preparer communities. Both the CFOF and GNAIE had representatives on the IWG, as did the major accounting firms and other national representatives. From the beginning, Sam Gutterman represented the IAA on the group and was the only actuary on the IWG until I joined as a representative of GNAIE in 2010. The IWG met roughly twice a year until 2012, with open discussion of the key issues benefiting the board members.

In August 2007, responding to suggestions from the industry, the Financial Accounting Standards Board (FASB) published an invitation to comment that included the current IASB Issues Paper, asking whether it should join the project. Responding to the comments received, the FASB decided to join the Insurance Project in October 2008 in an attempt to produce a joint standard.

At first this process went well, with both boards making concessions to bring their viewpoints closer together. They produced two common exposure documents, the last ones in 2013, which received robust comments from all interested parties. In the end, unfortunately, the two boards disagreed strongly on a few major issues, such as inclusion of the risk adjustment and discounting of P&C claim liabilities. The FASB withdrew from the project in 2014,2 citing its existing standard and its belief it could live with only limited modifications rather than the complete rewrite a joint standard would require.

As previously noted, the IASB produced a revised exposure draft in 2013. After considering the 194 comment letters it received and doing additional fieldwork, the IASB revised its draft standard for the final time and decided the completed standard would be produced by June 30, 2017. The IASB held discussions of sweep issues in November 2016 and February 2017 to finalize the details of the standard.

There were numerous key issues identified from the beginning. The remainder of this article will outline the development of the IASB’s position on some of the most important ones.

Basic Model for Liabilities

From the beginning, the IASB adopted the general approach of the DSOP, setting the basic liability equal to the present value of future cash flows (PVFCF) using current assumptions and current discount rates. This approach was named the building-block approach (BBA). It turned out, however, that stating that principle was easier than defining the details.

Short-Term Contracts

From the outset, U.S.-based P&C insurers strongly objected to both the use of the BBA for pre-claim liabilities and discounting for claim liabilities, particularly those with a relatively short claim period (e.g., auto and homeowners). They pointed out that internationally, almost every insurer used the unearned premium approach for pre-claim liabilities and undiscounted cash flows for claim liabilities other than those of a long duration, where the payments were fixed and determinable (e.g., workers’ compensation indemnity payments).

Eventually, the IASB agreed to allow the unearned premium approach, now called the premium allocation approach (PAA), considering it a simplification of the BBA. There was a long debate about discounting the claim liabilities, with U.S.-based firms objecting strenuously. But the IASB held firm, buttressed by the requirement for discounting already included in Solvency II.

Inclusion of a Risk Adjustment

The standard for liabilities under Solvency II included a provision for a risk adjustment to the basic PVFCF. Many U.S. firms failed to see the value of this adjustment, however, and it was one of the major disagreements between the IASB and FASB. Nevertheless, European companies and regulators were determined to keep IFRS consistent with Solvency II for this item, and the IASB held firm despite the United States’ disagreement.

Gain at Issue

This was one of the major problems to which most parties objected with the DSOP. Very early in the process, the IASB concluded that there should be no gain on issue. This was not a problem for short-duration contracts measured under the PAA. For long-duration contracts, this was solved by the introduction of a margin, eventually named the contractual service margin (CSM). The CSM was set equal at issue to the present value of future premiums less the present value of future outflows and the risk adjustment, thereby setting the gain at issue to zero. For claim liabilities, there was no CSM.

The BBA thus set liabilities equal to the present value of future cash flows plus the risk adjustment plus the CSM. The only remaining concern was how to amortize the CSM. Eventually, the IASB decided to simply amortize it over the lifetime of the contracts.

The Details

Once the basic models were agreed upon, the details occupied most of the lengthy discussion. In some cases, the discussions were theoretical in nature, and in others practical. The essential goal of all parties was to develop a methodology that gave a faithful representation of actual performance without creating noneconomic volatility. It was also important that the final result should permit comparisons among insurers without major use of “non-GAAP” measurers.

Setting the Discount Rate

One of the early proposals was to use a risk-free rate for discounting future cash flows. Insurers immediately objected to this since it would create a very large liability relative to the liability they had held previously. The Academy wrote a paper to the IASB and FASB recommending instead that the insurer be allowed to choose one of two methods.

One method, the bottom up, started with a risk-free rate and added a spread for illiquidity. The other method, called the top-down method, started with the actual earnings rate of the assets behind the liabilities and subtracted a provision for credit defaults and a few other items. In theory, the two interest rates should be equal (or very similar). The IASB adopted this proposal as a practical solution to the problem.

Setting Market-Level Assumptions for Long-Duration Contracts

Actuaries objected to the use of market-level assumptions for setting future cash flows on the grounds that no such assumptions could be identified that were both relevant and practical. The concept of an entry price approach was also suggested. Insurers noted that when there is an actual sale of insurance liabilities, the assumptions used for setting the liabilities were based on the best estimate of future experience of the companies involved. As a result, the IASB adopted the concept of fulfillment cash flows. For this, the assumptions were those that would be needed to fulfill the insurer’s obligations under the contract. The assumptions would be set by each preparer based on its own expectations of future experience.

While this was different in perspective from market assumptions, it could be viewed as what the market would use in the event of an actual transaction.

Treatment of Participating Contracts

As noted, the DSOP didn’t include a proposal for par contracts, and the initial IASB work didn’t either. Both the IASC and the IASB worked initially on the non-par issues, assuming that once those were resolved, the par issues would follow in a straightforward manner. They realized that this would not be the case when the IAA presented a summary showing the great variation in contract types available worldwide.

Europe’s unit-linked contracts, while seemingly similar to variable contracts in the United States and Canadian segmented fund products, actually had a significant difference in that their assets were in the insurer’s general account. Europe’s traditional par contracts either split earnings based on a formula (e.g., 90 percent of earnings go to policyholders) or paid very large terminal dividends.

The IASB first proposed a mirroring concept in which the liability equaled the assets supporting the liabilities. This would have worked reasonably well for unit-linked and variable contracts, but not for most other participating contracts.

Eventually, the IASB adopted the variable fee approach for most participating contracts. This approach applies only to direct participating contracts that meet the following requirements:

- The policyholder participates in a share of a clearly identified pool of underlying assets.

- The company expects to pay policy-holders a substantial share of the return from those underlying assets.

- The contract’s cash flows expect to vary substantially with underlying assets.

Under this approach, the measurement of the liability reflects the change in the fair value of all underlying assets, and the fulfillment cash flow is calculated consistent with the general model. Exactly which contracts this will apply to and how it will work in detail is still being discussed at this writing and may not be clear until after implementation.

Use of OCI for Liabilities

One of the more difficult issues the IASB had to deal with was the effect of changes to interest rates on liabilities because, as rates change, there could be a major impact on earnings for the reporting period. In response to complaints from insurers, the IASB agreed that the effect of interest rate changes on earnings should flow to other comprehensive income (OCI) as they do for unrealized gains and losses on assets. This approach greatly limits the volatility in the income statement but means that preparers need to calculate liabilities using two separate interest rates, one for the balance sheet and one for the income statement.

Revenue

Some members of the IASB objected to the use of premiums for life insurance and annuities as revenue in the income statement, noting that much of it effectively went to a deposit fund rather than to pay immediate benefits. In the course of the insurance project, the IASB and FASB agreed on a revenue standard that was very different from the traditional use of premium for insurance revenue.

After another long discussion, the IASB agreed on an actuarial approach to the subject. Revenue would include only the expected charges for benefits and expenses included in premium for the year. Amounts that created “deposits,” such as cash values on whole life polices, would be removed from premiums and treated as an amount on deposit. This means that the amounts shown as income and benefit expenses for the income statement would be significantly less than traditionally shown for long-duration contracts.

As a result of these and other decisions, almost every figure on the insurance company income statement and balance sheet is now actuarially determined rather than determined by an inventory, cash flow or other traditional accounting method.

Conclusion

Over the decade and a half that the IASB worked on the insurance contracts project, the actuarial profession was always involved, but that involvement significantly deepened and broadened over time. It became increasingly clear to all that actuarial input was essential to assure both the technical correctness and clarity of the final standard. As a secondary effect, the U.S. actuarial profession has become far more internationally focused than it was due to the need to develop common positions with jurisdictions in Europe and Asia. We will need to maintain this focus in the future and to always remind everyone that insurance accounting is too important to be left just to the accountants!

References:

- 1. Siegel, Henry. “A Groundbreaking Agreement on International Accounting.” Contingencies. Nov/Dec 2006. 34–41. ↩

- 2. The Financial Accounting Standards Board (FASB) subsequently adopted only minor changes to disclosures for short-duration contracts (including disclosure of the discounted value of liabilities). It is still discussing targeted changes for long-duration contracts. ↩

Copyright © 2017 by the Society of Actuaries, Schaumburg, Illinois.