Retirement Risks

A look at the societal impact of living longer

August/September 2017An era promptly ended earlier this year with the death of Emma Morano. Morano, an Italian supercentenarian whose birthday celebrations were broadcast live across Italy, passed away at the age of 117. She credited her longevity success in some part to eating raw eggs, consuming chocolate and positive thinking. With her passing, no one who was born in the 19th century is alive today.

Morano is an example of the increasing number of people who follow the theme of the Society of Actuaries (SOA) signature retirement and longevity program titled Living to 100. While we don’t currently have a “Consumption of Raw Eggs” longevity study underway, we increasingly are studying and featuring technical mortality results and the societal impact of living longer. A few years ago, the SOA formed a Longevity Advisory Group to create new projects aimed at the study of longevity, mortality modeling, and new techniques for assessing and predicting future mortality improvement results. This group complements other SOA practice research committees, sections and experience studies committees that similarly are pursuing new and innovative research. New projects on mortality topics at the SOA have quickly branched out to all parts of the SOA’s research work.

A Rich History

As I noted during a presentation at the Living to 100 Symposium in January, the study of mortality at the SOA quickly exceeds more than 100 years—if you include the work done by the two predecessor organizations (the Actuarial Society of America and the American Institute of Actuaries) that combined to form the SOA in 1949. Baked right into the “Reason for Being” statement from the Actuarial Society of America was the intent to gather actuaries across companies and practice areas to study aggregated mortality for use by members. From that history evolved milestones like the first studies focusing on the impact build and blood pressure on mortality in the 1920s, and a variety of annuitant tables issued from the late 19th century through the 1930s. One of the final steps the two predecessor organizations teamed up to create, prior to forming the SOA in 1949, was developing the 1941 Valuation Basic Table (VBT) and Commissioners’ Standard Ordinary (CSO) Table.

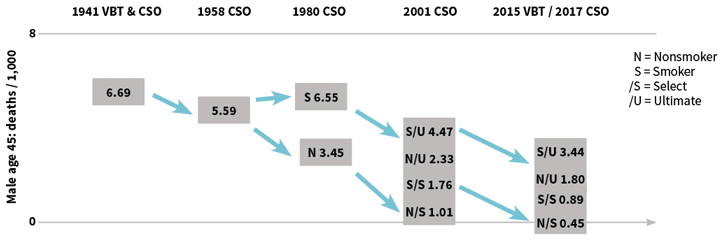

It’s interesting to think about the common vocabulary we use as actuaries today. When someone asks, “What table are you using?” the question really implies a broad group of tables you might be drawing from to set valuation assumptions. With the 1941 VBT and CSO, however, the answer to the question would actually be correct to note one distinct table, as the table combines male and female mortality into one single table and was only created on an age nearest birthday (ANB) basis. The table was based upon the experience of the 16 principal life insurers in the United States and Canada at the time, stemming from experience between 1931 and 1940. As a reference, the mortality rate for a male at attained age 45 in the table was 6.69 deaths per 1,000—approximately the same rate as an 83-year-old male nonsmoker being selected for life insurance in the 2015 VBT.

As mortality analysis and underwriting grew through the second half of the 20th century, our work at the SOA quickly adapted. The 1958 CSO project includes four main tables as gender-specific mortality was created, and tables were created on both an ANB and age last birthday (ALB) basis. The male attained age 45 mortality rate in the 1958 CSO moved down to 5.59 deaths per 1,000. With tobacco use becoming a more prominent underwriting factor, the 1980 CSO project included a set of 12 main tables, and male nonsmoker rates vaulted down to 3.45 deaths per 1,000.

The 2001 CSO project expanded to recognize the use of select and ultimate mortality, extended term tables and gender blends to get the number of tables to be more than 100, and mortality of a male nonsmoker selected at age 45 moved to 1.01 deaths per 1,000. Finally, with the evolution of relative risk tables, the number of tables in a project has grown even further with the most recent 2015 VBT/2017 CSO project. And that’s even prior to thinking about tables that will evolve for preneed, guaranteed issue and simplified issue business. A male nonsmoker selected at age 45 has a mortality rate of 0.45 deaths per 1,000 in the 2015 VBT. It’s been very helpful for SOA experience studies committees, often in conjunction with American Academy of Actuaries (the Academy) committees and input and guidance from insurance regulators, to produce the types of information needed to assess and value complex individual life insurance liabilities. See Figure 1.

Similarly, annuity tables have evolved over the years, leading to the most recent set of analysis produced by the SOA. We recently completed a set of annuity mortality studies, aimed at assessing aggregated U.S. industry results across product lines like individual and group payout annuities, as well as structured settlements. Results are compared to several former studies, especially to identify if any eroding margin is occurring in current U.S. statutory valuation standards. With group annuity exposures in recent years also coming from pension risk transfers exchanged between employer sponsors and life insurance companies, results also are compared to commonly used pension valuation tables. And as the individual life insurance market in the United States continues to have a wide variety of product types, underwriting techniques and distribution methods, mortality tables are keeping pace with industry needs.

Looking to the Future of Longevity

We continue to expand our set of studies. The anticipated release of the first U.S. public plans mortality study is in 2018, with the hope of potentially producing tables down to variables like occupation class. With increasing aggregated information on the longevity of participants in public retirement plans, actuaries can have additional insights to produce valuation assumptions and funding discussions with plan sponsors.

As important as mortality studies are, however, the growing focus across many practice areas is in the area of mortality improvement. Research committees at the SOA have been investing an increasing amount of time in gathering data and building mortality improvement models for actuaries to use. In the pension area, the SOA’s Retirement Plans Experience Committee (RPEC) has made annual updates to the RPEC_2014 mortality improvement model. This model, along with a set of assumptions researched and selected by the committee, produced the MP-2016 improvement scale in October 2016.

The model, however, also can be used with a wide variety of individually selected assumptions. Actuaries may review the trends and characteristics of the cohort they are studying, select a set of model parameters they think is appropriate, and develop a mortality improvement scale that fits their purpose. The SOA continues to look at how mortality improvement is changing across national populations and in smaller selected cohorts, such as pension plans and different groups of insured lives. With recent stagnation in mortality improvement in the United States and around the world, it’s an important topic for actuaries to understand and develop.

Longevity analysis, however, doesn’t just start and stop with evaluating insurance mortality risk. We continue to have a strong group of industry volunteers emphasizing education and noting retirement risks in our Committee on Post-Retirement Needs and Risks. This group frequently has its work highlighted in major media publications and often fields requests to speak on longevity at a broad set of industry meetings. See the “Findings” sidebar for some of the highlights of this group’s recent work.

SOA COMMITTEE ON POST-RETIREMENT NEEDS AND RISKS RESEARCH

The SOA Committee on Post-Retirement Needs and Risks has produced a number of reports and research

projects on retirement risks. Highlights of the group’s most recent work include …

CONTINUE READING

One of the goals of our research areas is to fulfill an objective of providing more data and tools for our members. We recently renewed an annual grant to the University of California–Berkeley to continue supporting the work of the Human Mortality Database (HMD). HMD recently extended its work to include cause of death analysis for eight countries and looks to expand to more countries in 2017. It also aims to study mortality tables down to the state level within the United States. With this information, actuaries can be more easily equipped with trends in diseases and mortality. We also have been very pleased with the success of the Longevity Illustrator, a tool developed in partnership with the Academy. This tool allows the public to better assess and measure longevity risk, and plan better with objective data provided by the actuarial profession.

Retirement Preparedness

The Longevity Illustrator also highlights the growing need for the actuarial profession around the world to promote retirement plans that include lifetime income options. We continue to face a world where longevity risk is analogous to a raging fire hiding within the walls of a house. It’s very difficult for the public to notice the risk growing as they age, and it’s not until the smoke begins billowing out of the walls that action is taken. By that time, it’s far too late to escape the danger. Even when the risk is discussed, many practitioners still talk in terms of a life expectancy metric, noting mainly the increase in life expectancies from birth that have occurred over time.

Longevity risk, however, is a much more delicate issue than simply noting the average ages that might be obtained across a population. First, actuaries need to change the public’s vocabulary to switch from “expectancy from birth” to “retirement preparedness.” I often use the statistic I call “life preparancy” in my longevity presentations, borrowing the comfortable sound of the phrase “life expectancy” but also injecting the need for preparing for the future. A life preparancy age might be commonly defined as the age to which 10 percent of a population that has already reached age 65 is expected to live in the future.

Just as life expectancies have generally increased across the world in recent decades, so have life preparancy ages. Figure 2 shows results from evaluating static population data from the Human Mortality Database in the United States, Canada, and England and Wales during past decades.

| Figure 2: Sample Life Preparancy Ages in England and Wales, Canada and the United States | ||||||

|---|---|---|---|---|---|---|

| England & Wales | Canada | United States | ||||

| Year | Female | Male | Female | Male | Female | Male |

| 1940 | 87.0 | 84.5 | 89.1 | 87.5 | 88.5 | 86.6 |

| 1950 | 88.9 | 86.1 | 90.0 | 88.1 | 90.6 | 87.9 |

| 1960 | 90.2 | 86.7 | 91.4 | 88.9 | 91.3 | 88.2 |

| 1970 | 91.2 | 87.0 | 93.0 | 89.5 | 92.5 | 88.6 |

| 1980 | 92.0 | 87.7 | 94.5 | 90.3 | 94.1 | 89.8 |

| 1990 | 93.5 | 89.3 | 95.2 | 91.1 | 95.0 | 90.9 |

| 2000 | 94.2 | 90.9 | 95.5 | 92.0 | 94.6 | 91.5 |

| 2010 | 95.7 | 93.3 | 96.8 | 93.9 | 96.0 | 93.5 |

Source: Human Mortality Database

The life preparancy age for the populations routinely has been higher than many may have expected, even at early dates in the analysis, with notable gains in recent decades. Recent stagnation in mortality improvement since 2010 likely will slow the pace of growth, but the ages help provide mortality data to consider alongside the retirement risks that were discussed at our Living to 100 Symposium.

When Emma Morano passed away, she passed the torch of longevity to others who will follow in her footsteps and perhaps challenge current longevity records. With the assistance of SOA mortality studies and corresponding longevity research, we aspire to keep the people of the world prepared to face their retirement risks head on.