Insights: Assisted Dying

Navigating ethics, risk and regulation as societal debate evolves

April 2026Humans have long sought to understand death, whether caused by natural factors such as aging or disease, or by unnatural events such as accidents or wars, through various fields, including biology, pathology, philosophy, metaphysics, spirituality, psychology, sociology, law, ethics, technology and economics.

Besides natural and unnatural causes, suicide—the voluntary and deliberate act of ending one’s own life—has long been a topic of intense debate and reflection. In recent decades, this and other articles have shown, the issue of assisted dying, which involves providing professional support to individuals suffering from disabling or terminal illnesses to end their lives, has gained increasing attention in public conversation, medical ethics and legislation.

This article doesn’t delve into the religious and cultural opposition to assisted dying and is limited in its discussion of the psychological and societal impacts. It’s not meant to advocate for or against assisted dying, but rather to examine its potential implications for insurers under varying legal frameworks.

ON DEATH AND DYING

In earlier centuries, when medical science was far less advanced than it is today, death loomed over people at every stage of life. Infectious diseases frequently contributed to widespread mortality, sometimes decimating entire populations. Wars and conflicts added to the death toll, as did malnutrition and famine. As the data show, the average global life expectancy at birth in 1900 was just over 32 years.

Over the past century, however, extended periods of relative peace, improved sanitation, public health initiatives and significant advances in medicine (including diagnosis, prognosis, therapy, and palliative care) have dramatically increased human longevity worldwide. By 2024, the global average life expectancy at birth had risen to approximately 73.3 years, more than double the figure recorded a century earlier.1

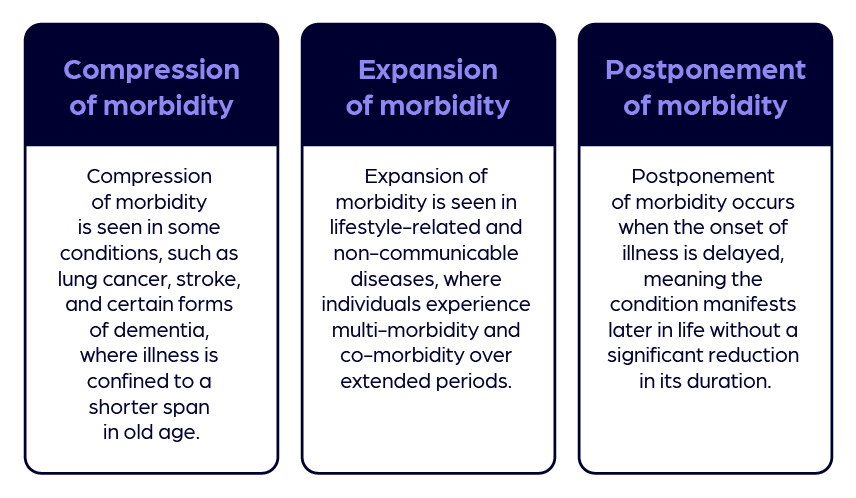

The world is now confronting a new challenge: the implications of longer lifespans. The World Health Organization projects that the population aged 80 years and older will nearly triple between 2020 and 2050, reaching approximately 426 million.2 Early epidemiological optimism suggested that this increase in longevity might lead to a “compression of morbidity,” the idea that the burden of illness would be concentrated and compressed into a relatively short period near the end of life.3 However, three distinct morbidity pathways are now unfolding (see Figure 1).4 For conditions such as myocardial infarction, a dual trend has been noted: compression among older adults but expansion among middle-aged populations.

Figure 1: Increasing life expectancy and burden of illness

Source: Authors via PresentationGo.com

Alongside rising longevity, some societies are undergoing a broader “epidemiological transition;” a shift from the predominance of acute infectious and deficiency diseases to chronic, noncommunicable conditions.5 When this transition is overlaid with longer lifespans and the expansion of morbidity, the result is prolonged survival but often with compromised health, multimorbidity and comorbidity. This trajectory of epidemiological manifestation diminishes both the quality and dignity of life.

Across cultures and belief systems, many individuals express the desire to die peacefully and with dignity, though what that means may vary. For some individuals, living with a terminal illness, severe incapacity, or an inability to perform activities of daily living independently raises issues of quality of life and autonomy. Others may find value in seeking treatments and preserving life despite the physical and emotional distress associated with terminal illness or loss of independence.

The “right to life” is a fundamental human right enshrined in legal systems worldwide. In recent years, legal and ethical debates have emerged over whether an individual’s autonomy at the end of life should include the option to seek assistance in dying. Proponents argue this reflects respect for self-determination, while opponents contend that the right to life does not entail a corresponding right to assisted death. These competing interpretations continue to shape legislative and judicial outcomes.6 This discourse arises from the conviction that individuals possess the autonomy to make fundamental decisions about their lives, including the choice to end their lives with dignity.

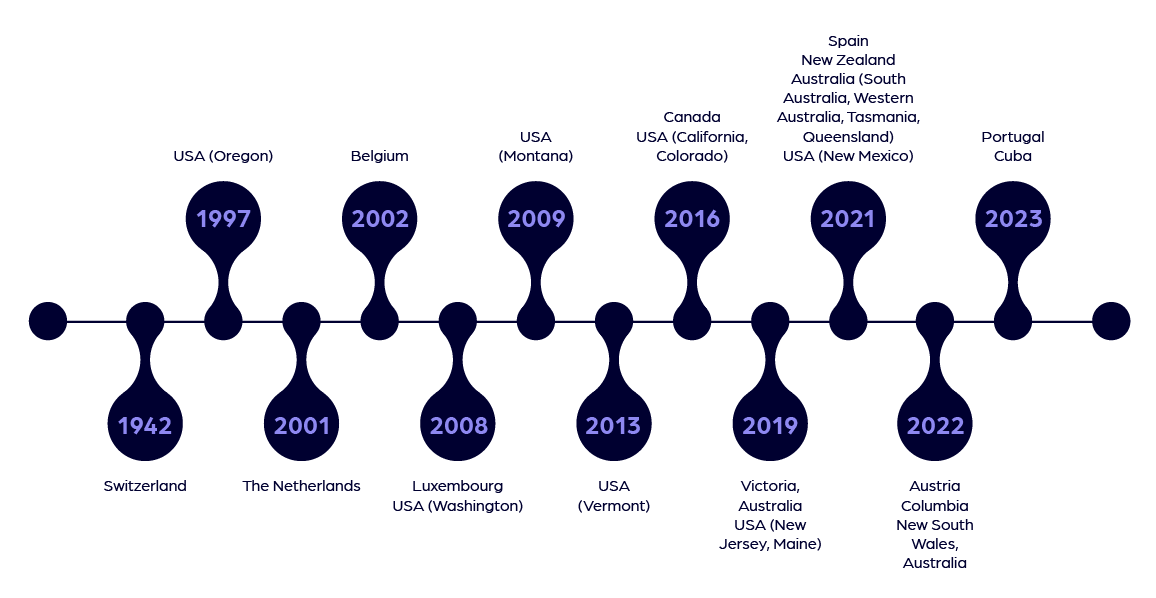

Over the past two decades, several countries and sub-national jurisdictions have enacted or proposed laws permitting some form of assisted dying, while others have reaffirmed or strengthened prohibitions. The resulting legal landscape remains uneven and politically contested, reflecting differing societal values, legal traditions, and ethical priorities, with some countries and states moving to legalize the practice (see Figure 2).7

Figure 2: Global legalization timeline of assisted dying practices

Source: Authors

Recent developments include the introduction of a bill in the United Kingdom’s House of Commons to legalize assisted dying for terminally ill, mentally competent adults in England and Wales, as well as the passage of a draft law by the French National Assembly that would permit terminally ill or gravely injured patients the right to die.

ASSISTED DYING ACROSS THE WORLD

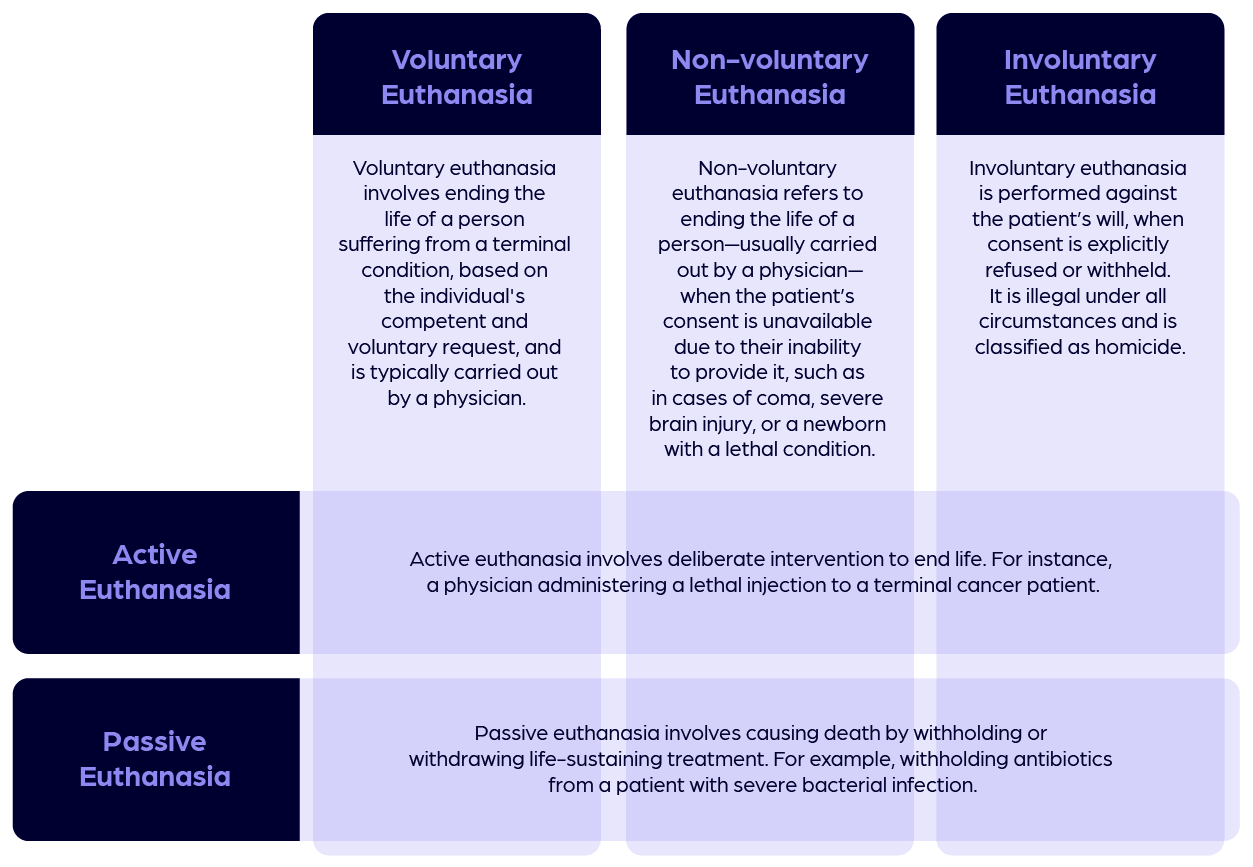

Although individuals in many jurisdictions have sought assistance in dying—typically in the context of terminal illness—there remains little consistency across countries in terminology, legalities and permitted practices. The widely recognized term “euthanasia,” also known as mercy killing, originates from the Greek word meaning “a good death.” Depending on whether the individual provides informed consent, euthanasia is classified into three categories: voluntary, non-voluntary, and involuntary. However, based on the method used, these are further divided into active and passive forms (see Figure 3).8

Figure 3: Types of euthanasia

Source: Authors

A few other terms used across the world are “medical assistance in dying” in Canada, “physician-assisted dying” or “medical aid in dying” in the United States, “euthanasia” in Belgium and the Netherlands, and “voluntary assisted dying” in Australia.

The term “assisted dying” carries different meanings across the world. In some countries, it is used synonymously with voluntary euthanasia; in others, it refers specifically to assisted suicide; and in still others, it serves as an overarching term encompassing both practices. The distinction between the two is based on the role of the physician. In voluntary euthanasia, a doctor is directly involved in administering the lethal medication. In assisted suicide, by contrast, the individual is provided with the means, typically a prescription for lethal drugs, but must self-administer the medication to end their life. Throughout this article, the term “assisted dying” is broadly used to indicate both

The subject of assisted dying is highly sensitive and evokes a wide range of emotions and arguments. The legal landscape worldwide remains highly uneven, with significant variation in the permissions granted for voluntary and non-voluntary euthanasia, whether by active or passive means. The distinction between active and passive causation of death is often the key determinant in whether assisted dying is legally permitted.

A LOOK AT ASSISTED DEATHS

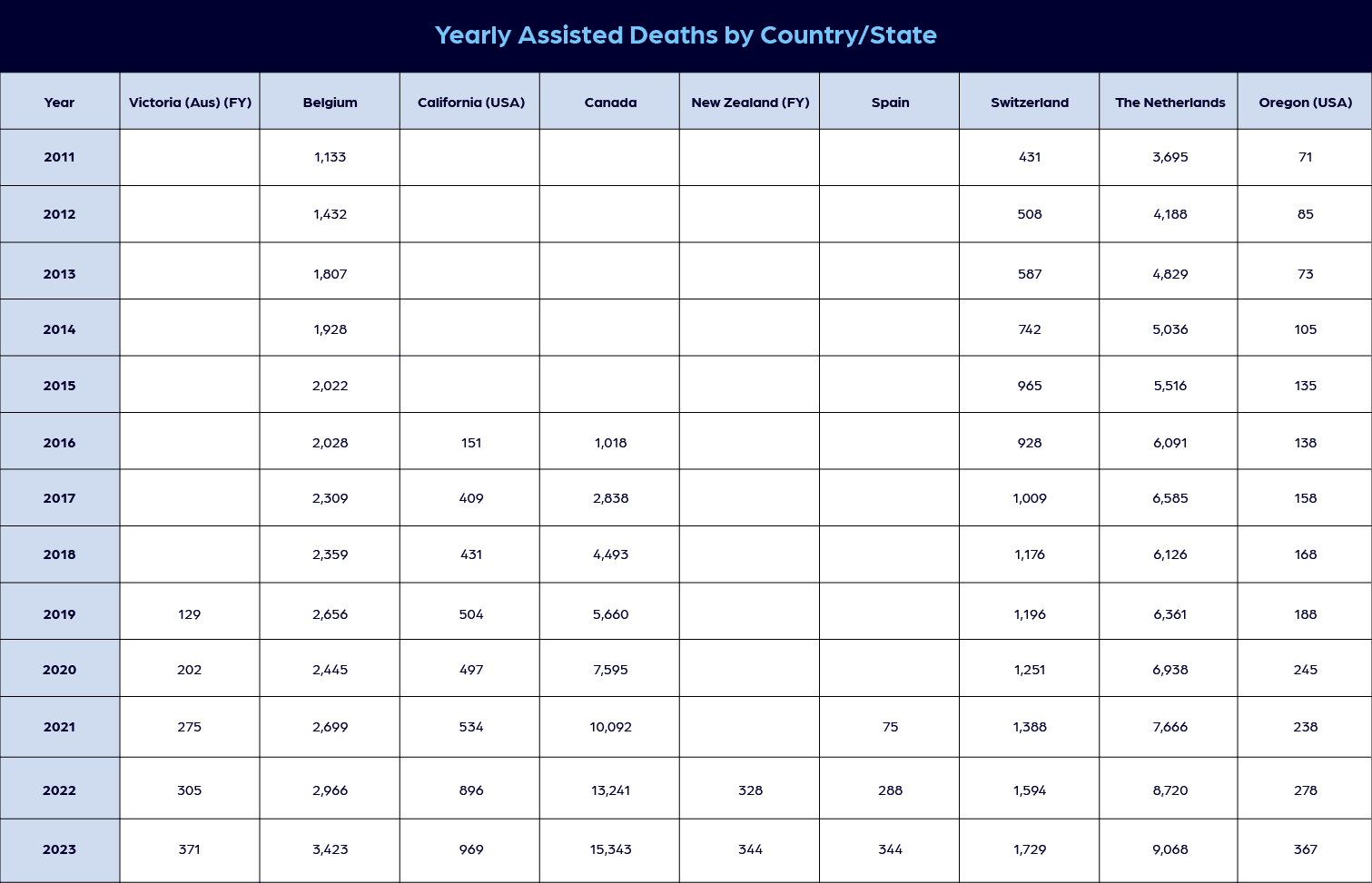

Assisted dying, as a concept and a means of death, is evolving. It remains in the early stages of legal and social recognition. The permitted reasons for assisted dying are continually expanding to include new health conditions and mental health disorders. For the insurance industry, although the number of people opting for assisted dying to end their lives is on the rise (see Table 1), it is, from our experience, generally still not considered statistically significant enough to be treated as a distinct type of death, warranting changes to policy conditions that contain explicit provisions either including or excluding voluntary euthanasia or assisted suicide.

Table 1: Annual assisted deaths in selected jurisdictions

Source: Authors, with citations 9,10,11,12,13,14

Currently, from what we’ve seen, insurers typically apply existing clauses, principles and doctrines to address assisted dying. The treatment of assisted dying by the insurance industry varies depending on whether it is legally permitted in a country and, if so, whether voluntary euthanasia or assisted suicide is allowed.

Life insurance policies generally include a suicide clause, which remains in effect for a specified exclusion period, typically ranging from one to three years after the policy is purchased. This clause limits payments to beneficiaries if the policyholder dies by suicide during the exclusion period. In such cases, the insurer may either refund the premiums paid or pay the mathematical reserve (the accumulated value up to the date of death).15 If suicide occurs after the exclusion period, insurers typically pay the full death benefit as per the policy terms. The rationale for this restriction is to prevent individuals from purchasing life insurance with the immediate intent of self-inflicted death to secure benefits for their dependents.

Insurance contracts may be governed by the doctrine of uberrima fides, or utmost good faith. This principle requires both parties—the insurer and the insured—to act with complete honesty and transparency. The policyholder is therefore obligated to disclose all material facts, conditions and risks relevant to the contract. Any failure to disclose such information, including known pre-existing health conditions, may render the policy void.

Regardless of whether assisted dying is legally permitted in a particular jurisdiction, if the insured knowingly conceals or misrepresents information about a terminal illness, such nondisclosure in some cases could be treated as insurance fraud. In such circumstances, the insurer may invoke the contestability clause to deny the claim. This clause provides that if the insured dies within the contestability period, typically two to three years after the policy is issued or reinstated, the insurer has the right to investigate the application and, if discrepancies or undisclosed health conditions are found, to void the policy or reject the claim.

In practice, as an example from this report shows, insurers may apply the standard suicide exclusion clause when assessing claims related to assisted dying. jurisdictions where assisted dying is legally permitted, insurers may assess related claims in accordance with existing policy definitions, regulatory guidance and case law. In some cases, such deaths are treated similarly to deaths from natural causes, while in others, they are evaluated under suicide or specific exclusion clauses.16 However, insurers still typically investigate to confirm that the policyholder did not withhold any material information at the time of purchasing the policy. If the terminal illness was unknown to the insured at the time of application, the nondisclosure is disregarded, and the claim is settled.

In jurisdictions where voluntary euthanasia or assisted suicide remains illegal, insurers treat such deaths as unlawful, deny claims, and in some cases classify them as murder or participation in an illegal act. If the policy wording includes an explicit exclusion for death resulting from unlawful activity, insurers can invoke this clause to reject a claim. As this report shows, such denials may be subject to judicial review, as beneficiaries may contest them in court, regardless of when the death occurs.

One area of concern we’ve seen for insurers is when the individual who assisted or facilitated the act is also the named beneficiary or stands to gain, directly or indirectly, from the estate. This scenario creates a potential conflict of interest. To address this, insurers draft policy wordings with clear distinctions between beneficiaries who provide legitimate emotional or logistical support and those who may exert undue influence or coercion.17 Such clarity is essential, given the risk that a terminally ill person could be made to feel guilty for not choosing assisted dying and, as a result, be implicitly or explicitly pressured into it. However, it may be difficult to legally prove such cases of coercion.

With respect to the current common suite of riders and standalone products such as critical illness coverage, accelerated benefit payouts for terminal illness, and long-term care insurance, the procedural and financial implications for insurers depend on the nature of illness, the timing of the claim submission and the point at which the insured opts for assisted dying. For example, critical illness riders typically impose a waiting period from the date of diagnosis before benefits are payable. Terminal illness benefits often define an eligible condition as one where the insured is expected to live for a period of 12 months or less.18

Long-term care policies vary widely in their benefit periods and eligibility criteria. Consequently, insurers must evaluate whether the insured elects assisted dying before or after these benefits are triggered and paid. In the context of health insurance, assisted dying could reduce overall claim exposure, as benefit payments cease upon the insured’s death. Under these policies, insurers would otherwise have been obligated to continue covering healthcare costs had the insured remained alive. (Any such effects are incidental and do not influence coverage decisions, which are governed by ethical standards and regulations).

At present, where assisted dying is legally permitted, the number of people opting for it remains relatively low, and insurers have not yet been required to significantly adjust their actuarial models. For example, a report from Canada shows that in 2023, 15,343 people in Canada died via Medical Assistance in Dying (MAID), representing 4.7 percent of all deaths (out of 326,571 total deaths). In the Netherlands, a report on the Termination of Life on Request and Assisted Suicide indicates that in 2023, 9,068 people died by euthanasia, accounting for 5.1 percent of all deaths (169,363 in total).

The incremental cost of settling claims earlier, compared to a natural death occurring only a few months or years later, is immaterial. Consequently, insurers have not introduced significant changes in the premiums they charge. Future developments in assisted dying may depend on legal safeguards, societal values, medical practice standards and political processes within each jurisdiction. While some societies may expand access, others may maintain or reinforce existing restrictions. If the number of individuals opting for assisted dying increases significantly, insurers may be compelled to reassess their risk models to account for the randomness of early death claim payouts, beyond what standard mortality calculations typically predict.

Most countries that currently permit assisted dying restrict access to their own citizens. However, nations such as Switzerland and Belgium extend eligibility to nonresidents—a practice that has led to the rise of so-called “suicide tourism,” where terminally ill individuals travel abroad to end their lives. From the perspective of standard travel insurance policies, which typically cover accidental death, emergency medical expenses, repatriation of remains or funeral costs, this trend is unlikely to significantly impact coverage. These policies almost universally include exclusions for pre-existing illnesses or medical conditions contributing to death, which directly apply in cases of assisted dying. Furthermore, the principles of randomness and unpredictability, fundamental to insurable risk, are compromised when death is premeditated through assisted suicide, further limiting applicability under existing travel insurance.

Looking forward, as assisted dying may become more widely accepted, insurers may explore new product designs. Health insurance policies could evolve to include coverage for expenses related to assisted death, and specialized insurance contracts and riders may emerge with deferred commencement of risk to cover costs linked to assisted dying.

CONCLUSION

Choosing to actively bring one’s life to an end, rather than enduring prolonged or painful suffering, may be the most profound decision an individual can make. As French philosopher and novelist Albert Camus is attributed as saying, “There is but one truly serious philosophical problem, and that is suicide. Judging whether life is or is not worth living amounts to answering the fundamental question of philosophy.”

As populations age and the prevalence of chronic and terminal illness increases, debates surrounding assisted dying are likely to persist. With elderly populations in some countries expanding rapidly and the rise of chronic and terminal illnesses intensifying, existing caregiving systems may come under severe stress. Against this backdrop, the debate over assisted dying is likely to gain momentum. In the coming years, we believe it may continue to be debated and, in some jurisdictions, further considered for legalization.

We believe the insurance industry plays a pivotal role in navigating these uncharted waters, striking a balance between ethical responsibilities and the financial sustainability of its business. To respond effectively, insurers may establish clear, transparent guidelines and continuously reassess their risk models. These steps are essential to ensure that the industry can responsibly accommodate the growing societal acceptance and demand for assisted dying.

Assisted dying may, in some jurisdictions, become more formally incorporated into healthcare and legal frameworks, while remaining restricted or prohibited in others. We believe this makes it imperative for all stakeholders, including medical professionals, lawmakers, and insurers, to work collaboratively in shaping systems that are legally robust, ethically governed and aligned with societal values. However, as the number of people opting for assisted dying increases, there is a real risk that safeguards designed to protect autonomy could erode into perfunctory checklist rituals. When this happens, the sanctity of patient autonomy may slip through procedural gaps, leaving room for coercion. Robust legal guardrails and vigilant monitoring systems could ensure that dignity, consent and individual wishes remain at the very center of assisted dying practices.

Statements of fact and opinions expressed herein are those of the individual authors and

are not necessarily those of the Society of Actuaries or the respective authors’ employers.

References:

- 1. Herre, Bastien. Global average life expectancy has more than doubled since 1900. Our World in Data, February 2025. Global average life expectancy has more than doubled since 1900 (accessed October 5, 2025). ↩

- 2. Staff. Aging and Health. World Health Organization, October 2025. Aging and Health (accessed October 5, 2025). ↩

- 3. Permanyer, Inaki. Healthy lifespan inequality: morbidity compression from a global perspective. National Library of Medicine, May 2023. Healthy lifespan inequality: morbidity compression from a global perspective (accessed October 5, 2025). ↩

- 4. Villavicencio, Francisco, et al. Is morbidity compressing around the globe? Neodemos, June 2023. Is morbidity compressing around the globe? (accessed October 5, 2025). ↩

- 5. Bramhankar, Mahadev, Dhar, Murali. Diseases Burden and epidemiological transition status at the national and sub-national level in India: a contemporary perspective. Springer Nature, February 2025. Diseases Burden and epidemiological transition status at the national and sub-national level in India: a contemporary perspective (accessed October 5, 2025). ↩

- 6. Kaur, Jessica, Mishra, Naincy. Article 21 of the Indian Constitution: Right to Live and Personal Liberty. iPleaders, February 2024. Article 21 of the Indian Constitution: Right to Live and Personal Liberty (accessed October 5, 2025). ↩

- 7. Staff. Assisted Dying Around the World. Campaign for Dignity in Dying, January 2025. Assisted Dying Around the World (accessed October 5, 2025). ↩

- 8. Staff. Euthanasia and Assisted Dying. The Medic Portal, February 2024. Euthanasia and Assisted Dying (accessed October 5, 2025). ↩

- 9. Staff. Annual Report. Voluntary Assisted Dying Review Board, July 2023 to June 2024. Voluntary Assisted Dying Review Board Annual Report (accessed October 5, 2025). ↩

- 10. Staff. Biennial report for 2022–2023. The Federal Commission for the Control and Evaluation of Euthanasia, January 2025. Press Release from the Federal Commission for the Control and Evaluation of Euthanasia – FCCEE (accessed October 5, 2025). ↩

- 11. Staff. California End-of-Life Option Act 2024 Data Report. California Dept. of Public Health, July 2025. California End of Life Option Act 2024 Data Report (accessed October 5, 2025). ↩

- 12. Summary statistics. Dignitas—to live with dignity—to die with dignity. Swiss Federal Statistic Office, December 2024. Life Expectancy, Suicide, Assisted Suicide, Deaths, Population, in Switzerland (accessed October 5, 2025). ↩

- 13. Multiple authors. Euthanasia in Figures: Arguments for the debate. Compiled report, November 2022. Euthanasia in Figures (accessed October 5, 2025). ↩

- 14. Multiple authors. Regional Euthanasia Review Committees. Compiled report, May 2022. Regional Euthanasia Review Committee (accessed October 5, 2025). ↩

- 15. Barrett, Peter; Calder Brown, Jennie. Claims management considerations. RGA Publications, September 2015. Global Claims Views: Assisted Suicide and Euthanasia (accessed October 5, 2025). ↩

- 16. Rubin, Sammy. Assisted Dying and Life Insurance. YuLife article, February 2025. What are the Implications of Assisted Dying on Life Insurance? (accessed October 5, 2025). ↩

- 17. Barrett, Peter; Calder Brown, Jennie. Claims management considerations. RGA Publications, September 2015. Global Claims Views: Assisted Suicide and Euthanasia (accessed October 5, 2025). ↩

- 18. Multiple authors. Assisted Dying Legislation. SCOR article, September 2024. The Impact of Assisted Dying Legislation on Life and Health Protection (accessed October 5, 2025). ↩

Copyright © 2026 by the Society of Actuaries, Chicago, Illinois.