From Pension Risk to Alignment

How stakeholder engagement shapes informed decisions

May 2026As reports and articles detail, Canada’s retirement system is evolving, driven by shifting demographics, market conditions, and longer lifespans, all of which are reshaping what retirement looks like and how Canadians and their employers prepare for it.

In this environment, innovation in plan design, investment strategy and plan management is a key pillar that helps ensure the long-term sustainability of pension plans. However, without a stakeholder-first mindset—an approach that combines transparent messaging with genuine engagement and support—even the best-designed retirement strategies can fail to build trust or achieve alignment. Now, I believe more than ever that how organizations communicate, listen to and support people through decisions that affect their financial futures is important.

Changing landscape in Canada

With half of retirement-age Canadians expected to live to 90, many will spend a third or more of their lives in retirement. That creates a very different planning horizon than previous generations had: Retirement income needs to last longer, demand for health and long-term care is rising, and the design of public programs and workplace pensions must account for decades of income, not just for a few years after age 65.1

The World Economic Forum highlights that many countries face a growing “retirement savings gap” driven by longer lifespans, rising health costs, and changing labor markets, and that closing this gap will require system-level innovation and better engagement with individuals.2

Against this backdrop, employees may encounter several interconnected challenges:

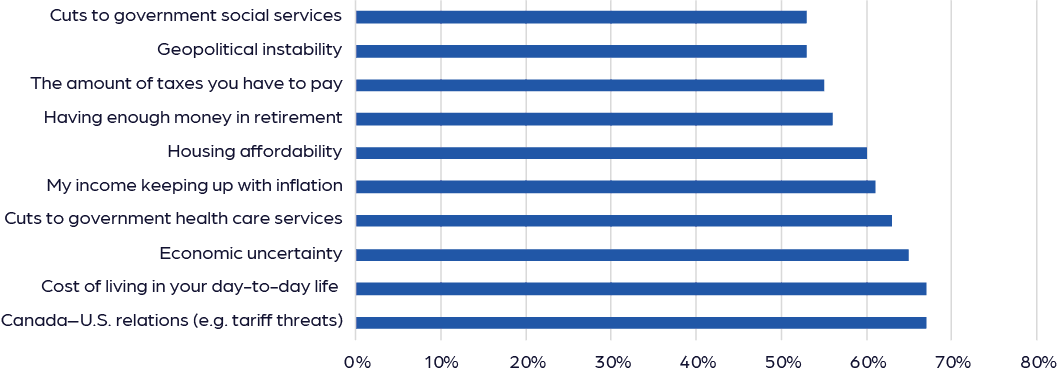

Affordability and competing priorities. As retirement stretches over a longer period, many Canadians are still struggling to get through the month. Day-to-day financial pressures from rising living costs and housing affordability are top concerns for Canadians, with broader economic uncertainty and potential health care cuts also on the rise.3 All of these might make it harder to set aside enough for the future.

Figure 1: Cost of living concerns

Source: 2025 Canadian Retirement Survey

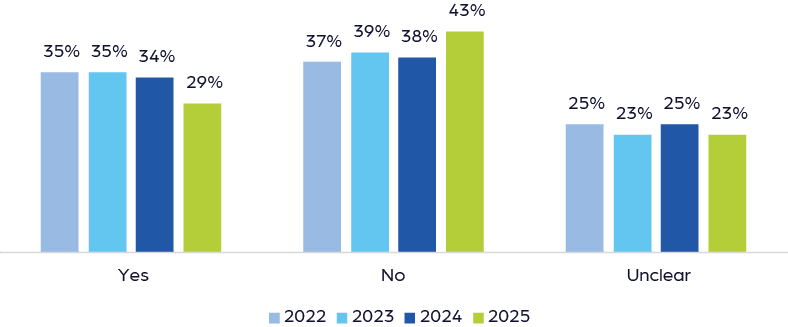

Longevity and uncertainty. Longer lifespans and volatile markets make it harder to answer the basic question, “Will I have enough money in retirement?” Canadians are often challenged to balance competing retirement priorities of maximizing income, managing risks (such as outliving assets and sustaining purchasing power) and maintaining some flexible access to retirement funds. In fact, the percentage of older Canadians who can afford to retire at their desired age hovers around 30% and has continued to decline over the last few years.4

Figure 2: Affordable retirement levels

Source: The 2025 Aging in Canada Survey

Employers, for their part, are facing a difficult balancing act. On the one hand, they need to attract and retain talent, address skills shortages and manage a multigenerational workforce; while on the other, they are under intense pressure to control costs. In fact, 72% of employers cite cost constraints as the top barrier to achieving total rewards success,5 even as they try to compete for talent and invest in workforce resilience. This combination of talent pressures, workforce management challenges and budget mandates are driving organizations to rethink how they design and communicate their benefit and retirement programs.

Amid all of this, organizations are turning to innovation in how they structure retirement programs, manage risk and support employees’ financial lives.

STAKEHOLDER ENGAGEMENT AT THE HEART OF INNOVATION

When considering large-scale changes such as restructuring benefits, consolidating plans, or joining larger sector‑wide arrangements, I believe actuarial modeling, familiarity with legislative requirements and an in-depth understanding of tradeoffs are essential.

But, in my experience, how an organization engages with stakeholders can be just as important as what it decides. In my view, stakeholder engagement means ensuring employees, unions, retirees, boards, regulators and partners are active participants in the process, not passive recipients of a decision.

This includes communicating early and clearly about options, constraints and tradeoffs; providing opportunities for questions and feedback before decisions are finalized; and supporting people with information, tools, and governance structures that help them understand and live with the outcomes.

In my view, practical, effective stakeholder engagement often rests on three principles:

- Transparency. Honest, timely, plain‑language explanations of what is changing and why, including the financial and regulatory constraints that shape the options.

- Participation. Structured opportunities for stakeholders to ask questions, raise concerns, provide input throughout the process and influence decisions.

- Support. Concrete steps to help stakeholders understand the implications of the change and trust that their interests are being stewarded over the long term.

Grand River Hospital’s pension plan de-risking journey and transition toward participation in the Healthcare of Ontario Pension Plan (HOOPP) offers a practical example of these principles in action.

THE GRAND RIVER HOSPITAL CASE STUDY: CONTEXT AND CATALYST

The KW Pension Plan was established more than 60 years ago by what is now Grand River Hospital Corporation (GRH) to provide a defined benefit pension to employees at the hospital’s main downtown Kitchener site. Over time, mergers and historical choices created a two-tier structure: Most staff at the main site participated in the KW Plan, while employees at another site participated in HOOPP.

Over the years, the desire for equitable, harmonized benefits for all within HOOPP has been expressed. The two-tier structure posed recruitment challenges for GRH. Various options surrounding the KW Plan and a possible merger of the plan into HOOPP were examined.

In fact, when Ibrahim Toor, director of pension at Waterloo Regional Health Network (formerly Grand River Hospital), was hired in late 2022, it was with a mandate from the network to strengthen the KW Pension Plan and identify potential de-risking solutions.

In 2024, the merger of Grand River and St. Mary’s General Hospital, already a HOOPP employer, was approved, creating a new organization, the Waterloo Regional Health Network (WRHN), effective April 2025. A two‑tier structure within the new organization would have amplified equity concerns. At the same time, as Toor revealed, Grand River Hospital’s board expressed a long‑term desire to exit the pension management business to focus resources on healthcare delivery.

Once the establishment of WRHN was announced, employees asked about the future of the KW Pension Plan, and interest in merging with HOOPP intensified, Toor indicated.

This created both an imperative and an opportunity to re‑examine the KW Plan and consider de‑risking and consolidation options.

OPTIONS AND CONSTRAINTS: SETTING THE STAGE FOR ENGAGEMENT

In late 2024, several options were formally considered:

- Status quo: Keep the KW Plan open to new KW site employees; other site employees will remain in/join HOOPP.

- Full merger with HOOPP: Transfer all past service into HOOPP

- Merger of active employees’ past service only

- HOOPP for future service: Freeze future service accruals in the KW Plan and enroll all KW Plan active employees in HOOPP effective April 1, 2025, with no transfer of past service

Each path involved trade‑offs. No option perfectly balanced equity, affordability, simplicity and risk. In my view, this is where stakeholder engagement moved from concept to practice.

STAKEHOLDER ENGAGEMENT IN ACTION: TRANSPARENCY, PARTICIPATION, SUPPORT

Transparency. During a town hall, these options were openly shared, including approximate cost estimates for each. Members could see:

- The potential significant cost of a full past‑service merger with HOOPP

- The more modest but still meaningful cost of a merger for active members only

- The projected budget impact of freezing the KW Plan and offering HOOPP for future service

At the town hall, it was emphasized that, although the plan freeze option was under serious consideration, no final decision had been made. The purpose was to explore options and keep staff informed and engaged throughout the process.

In ensuing information sessions and FAQs, GRH focused on the questions that mattered most to members, such as:

- Why isn’t past service being merged with HOOPP?

- Will the KW Plan run out of money after April 1, 2025?

- What happens if the plan becomes underfunded in the future?

Transparency does not eliminate concern, but it can help reduce speculation by providing more factual information about the options and the hospital’s constraints.

Participation. Stakeholder engagement also meant giving employees and their representatives structured ways to influence the process.

When management began evaluating the plan freeze, the proposal was first socialized with the Pension Advisory Committee, which includes representatives from each labor group and a retiree representative. This early engagement was intended to assess initial reactions, surface potential concerns and allow management to address questions before advancing the proposal further.

GRH invited feedback via:

- Live tools to collect questions and comments in real time during townhalls and sessions

- A dedicated email address for pension questions; and

- Follow‑up discussions with unions and local staff representatives

While participation does not change the underlying financial mathematics, it can change how the process feels to stakeholders: less like an imposed decision, more like a conversation in which their voices are heard.

Support. Finally, stakeholder engagement was reinforced by concrete support. GRH scheduled various member information sessions, both virtually and in person, at different times of day to ensure maximum flexibility and accessibility for attendees.

These sessions gave members multiple opportunities to hear a detailed explanation of the proposed changes, ask questions during live sessions and understand how their own situation might be affected.

“While formal pension information sessions for the broader active membership were helpful and effective, people leaders from specific teams reached out to me and said their staff had several questions and concerns regarding the proposal,” said Toor. “I offered to come in and have one-hour in-person candid conversations with the team. These one-hour sessions provided an opportunity to address concerns in detail, clarify misunderstandings, and reinforce trust through open dialogue.”

FOR MORE

Read The Actuary Canada article, “Small Details, Big Impact.”

Read the report, “Pension Risk Transfer in Canada and the U.S.,” at SOA.org.

GRH also engaged HOOPP early on and kept them fully informed of developments, providing regular updates. The hospital also planned several in‑person and virtual pension information sessions in collaboration with HOOPP so members could learn directly about the plan they would join for future service.

What Grand River’s experience shows

Grand River Hospital’s KW Pension Plan journey illustrates that, in the face of demographic pressures, market uncertainty and legacy inequities, stakeholder engagement may be a stabilizing force.

Three key lessons that stood out to me:

- Transparency builds credibility. In my experience, sharing real numbers, constraints and tradeoffs allowed members to understand why certain options were not feasible and how the chosen path was selected.

- Participation may help bolster legitimacy. Early engagement with the PAC and multiple feedback channels gave employees and unions meaningful roles in the process.

- Support fosters trust. Information sessions, collaboration with HOOPP, and strengthened governance structures demonstrated that GRH was not merely making a one‑time decision but committing to stewarding the plan and its members over the long term.

In a world of ongoing demographic, economic and workplace change, I believe organizations willing to invest in genuine stakeholder engagement may be better equipped to navigate complex choices and maintain trust through whatever developments and challenges come next.

Statements of fact and opinions expressed herein are those of the individual authors and

are not necessarily those of the Society of Actuaries or the respective authors’ employers.

References:

- 1. 2025 Projection Assumption Guidelines. April 2025. FP Canada Assumption Guidelines ↩

- 2. World Economic Forum. Future-Proofing the Longevity Economy: Innovations and Key Trends. WEF, with Mercer. March 2025. WEF_Future_Proofing_the_Longevity_Economy_2025.pdf ↩

- 3. HOOPP. 2025 Canadian Retirement Survey. June 2025. 2025 Canadian Retirement Survey | HOOPP ↩

- 4. National Institute on Ageing. Perspectives on Growing Older in Canada. January 2026. Perspectives-on-Growing-Older-The-2025-Ageing-in-Canada-Survey_Report.pdf ↩

- 5. AON. 2026 Human Capital Outlook: 5 Forces to Act On. January 2026. https://www.fpcanada.ca/projection-assumption-guidelines ↩

Copyright © 2026 by the Society of Actuaries, Chicago, Illinois.