Building Climate Resilience

Why actuaries should play an active role in a changing climate and support the Task Force on Climate-related Financial Disclosures (TCFD)

March 2021Photo: iStock.com/Sergey.Tinyakov

It is rather remarkable how the COVID-19 pandemic has increased societal resilience and accelerated the need to adapt to a new reality in a relatively short period of time. Yet, building even further resilience and adapting to a warming global climate may not be a foregone conclusion. With 2020 behind us—and a longer time horizon over which climate change will evolve in view— actuaries may be tempted to fall into complacency and put our risk assessment tools related to climate risks on the shelf. Meanwhile, insurance and pension regulators around the globe are engaging their stakeholders to better understand their climate-related risk readiness and are looking to build oversight capabilities. Insurers and investment funds are, therefore, recruiting climate champions and modeling experts, like actuaries, who will step forward and support the organization in examining complex risk issues. Given the far-reaching impacts that a changing climate is expected to have, it will be important for actuaries to transform their analysis toolkit and consider climate-related risks in their work sooner than later.

The Task Force on Climate-related Financial Disclosures (TCFD) published its recommendations and framework for helping organizations disclose high-quality and relevant information on the potential financial impacts of climate change.1 Through the assessment of climate-related risks and opportunities, actuaries can leverage the benefits of this fundamental exercise and feed into designing sustainable products, incentivizing consumer behaviors, allocating risk-based capital and strategic planning. When performed across multiple time horizons and climate pathways, scenario analysis can not only help build climate-resilient organizations for the future but for the present, too. This article discusses the developing role of actuaries in a changing climate and presents relevant considerations for insurers and pension plans to help meet the expectations of regulators and investors concerned about protecting the balance sheet.

Why Are the TCFD Recommendations Relevant to Actuaries?

Physical, Transition and Liability Risks

The TCFD disclosure framework sits on four pillars:

- Governance

- Strategy

- Risk management

- Metrics and targets of climate-related risks and opportunities

Actuaries can indeed play a role in all four pillars of TCFD and should not be limited to risk management only. Irrespective of actuarial practice area, three types of climate-related risks may occur: physical, transition and liability risks.

Physical risk includes the “direct effects of climate change, such as changes in the frequency or severity of catastrophe events”2 like hurricanes, droughts, wildfires, floods and extreme heatwaves, to name a few. A deep appreciation of physical risk is likely to come from an integration of external climate science models—those developed by the Intergovernmental Panel on Climate Change (IPCC) or the International Energy Agency (IEA), for instance.3

Transition risk is associated with the financial impact of the transition to a lower-carbon economy led by regulatory (e.g., carbon tax), market (e.g., changes in consumer preferences or behaviors) and technology-enabled forces (e.g., new investments in green and sustainable infrastructure). Arguably, a disorderly transition4 could have far-reaching consequences on the strategic, investment, market, operational and reputational risks of an organization.

Finally, liability risk refers to the risk of future claims from those affected by climate change seeking compensation from those they hold responsible because of inaction or negligence. Overall, all three risks may impact organizations over several time periods, with large regional and sectoral variability.

Scenario Analysis

In the context of climate change, scenario analysis is an exploratory exercise that relies on assumptions about multiple plausible climate futures—for instance, 1.5, 2, 3 or 4+ degree warming compared to preindustrial levels. For each scenario, it can provide a vector for the direction and magnitude of the financial impact of selected climate risks onto an organization’s key financial metrics relative to its exposure. Looking at how the current pandemic has unfolded, climate change will also bring about winners and losers. Strategic foresight, preparedness and scenario analysis thus may become valuable tools in navigating uncertainty in a constantly evolving landscape.

The forward-looking requirement will lead actuaries to use novel techniques to capture the evolving nature of climate risks and their key drivers. As historical data becomes less relevant and where data is simply not available (e.g., transition risks), climate risk assessment and monitoring may at times rely on qualitative analysis with expert judgment overlay from actuarial and climate expert perspectives. Indeed, some risk drivers may be hard to condense into single risk metrics. The findings from scenario analysis nevertheless can provide value and be integrated with existing actuarial processes.

Applications for Insurers: ORSA, Risk Appetite and Stress Testing

First, for insurers, there are many similarities between complying with TCFD recommendations (including scenario analysis) and the own risk solvency assessment (ORSA) process, where climate risks may be considered already in varying degrees. As insurers build their preparedness, resilience and strategies through an explicit articulation of their risk appetite, more explicit language needs to be added in the ORSA and risk appetite framework alongside the development of relevant risk monitoring metrics. For instance, material exposure to long-duration financial instruments at risk of a rapid movement to a low- or zero-carbon economy should warrant a statement at a minimum in the ORSA on both its exposure to transition but also liability risks linked to such investment activities.

Stress testing and scenario analysis approaches also may be added in the discussion of the ORSA. In a way, actuaries are, can and will be making significant contributions to the development and execution of these stress tests in relation to climate risks. As insurers become more familiar with how particular risk exposures may translate into financial risks across plausible climate futures, there may soon be little doubt about the value of going beyond the assessment of the direct impacts of climate risks. Including second- and even third-order effects, consistent with the compound nature of climate risks and the COVID-19 pandemic, could provide richer competitive opportunities to insurers and become more than a disclosure or regulatory reporting exercise.

Finally, the opportunities from the climate change transition risks also are part of the upside for insurers. Careful consideration will be necessary to articulate the possible benefits of such opportunities in the insurers’ risk appetite statements as well as in the description and measurement of risk limits for these new investment opportunities. These additional disclosures on risks may spur insurers to engage in climate mitigation and adaptation.

Applications for Pensions and Investments

There is no doubt that actuaries active in the pension world also have a large role to play in the global climate efforts. Examples include providing advice to regulators in crafting new climate-related regulations, leading large pension plans in managing climate risks (e.g., physical and transition risks) within their chosen investment strategies or advising institutional investors on integrating climate risks into their funding or investment policies.

In Canada, Ontario is the only province that requires a pension plan’s Statement of Investment Policy & Procedures (SIPP) to disclose whether environmental, social and governance (ESG) factors are integrated into the investment process. Current and proposed regulation in Europe goes much further, so a future where plan sponsors identify, manage and disclose climate-related risks in line with TCFD recommendations may be foreseeable due to growing pressure from the regulatory environment, investors and other stakeholders.

Aligning incentives also can be a very powerful tool in raising climate awareness. The CDPQ, one of Canada’s largest asset managers ($CAD 365B), now imposes a carbon budget on its investment teams, thus incentivizing a rebalancing of portfolio exposure from investments in carbon-intensive assets to low-carbon assets. It also includes climate metrics in the compensation calculation of its portfolio managers. More broadly, the world’s largest asset manager, BlackRock, is committed to supporting net-zero greenhouse gas emissions by 2050 and is helping investors realign their portfolios for this future, including capturing opportunities created by the net-zero transition. Indeed, there will be opportunities, and the pension world, through its asset management arm, should be paying attention.

Insurability and Affordability of Insurance Coverage

The Value of Resilience Building, Climate Adaptation and Stakeholder Partnerships

One of the actuarial profession’s key opportunities—closing the insurance protection gap—may seem to be under strain at a time when damage from extreme weather is rising considerably in various regions of the world. However, this situation may present the insurance industry with a renewed role to play in a changing climate.

First, model risk will increase as the reliance on historical data for future ratemaking becomes compromised. Looking at physical risks, for instance, the increased uncertainty around the frequency, severity and duration of extreme weather likely will be embedded in the pricing of some property and casualty (P&C) insurance offerings, with potentially severe implications for long-term insurability and affordability of high-risk areas. In turn, this also could adversely impact the protection gap. Thus, the impetus to control claim costs will continue to be strong, consistent with the collective mission of closing the protection gap.

One of the tools that can help reduce losses while supporting resilience to climate change impacts is climate adaptation.5 Looking at flood risk as an example, the Sendai Framework for Disaster Risk Reduction6 states that it is preferable to act on flood risk before it materializes into financial losses. In other words, offering financial products and services that explicitly encourage investments in individual or commercial flood risk protection measures and building climate-resilient infrastructure can contribute to societal resilience to climate change and reduce the variability of future claims.

Stakeholder partnerships—including local, provincial and federal governments; insurers; and local communities—also have an important role to play in preventing the protection gap from significantly increasing. That is, leaving vulnerable communities at risk of considerable financial hardship while also addressing affordability concerns in high-risk areas. To this effect, the high-quality research work of the Intact Centre on Climate Adaptation proposes novel adaptation aimed at de-risking the negative impact of extreme weather like flooding, while the Flood Re scheme in the United Kingdom is an example of public/private partnerships.

Overall, building climate resilience—given the increasing loss trend in extreme weather events—is likely to become part of the P&C insurance industry’s sustainability mandate. This huge opportunity may also help position (re)insurers as partners rather than payers only.

Climate Impacts Include Physical Damage and Beyond

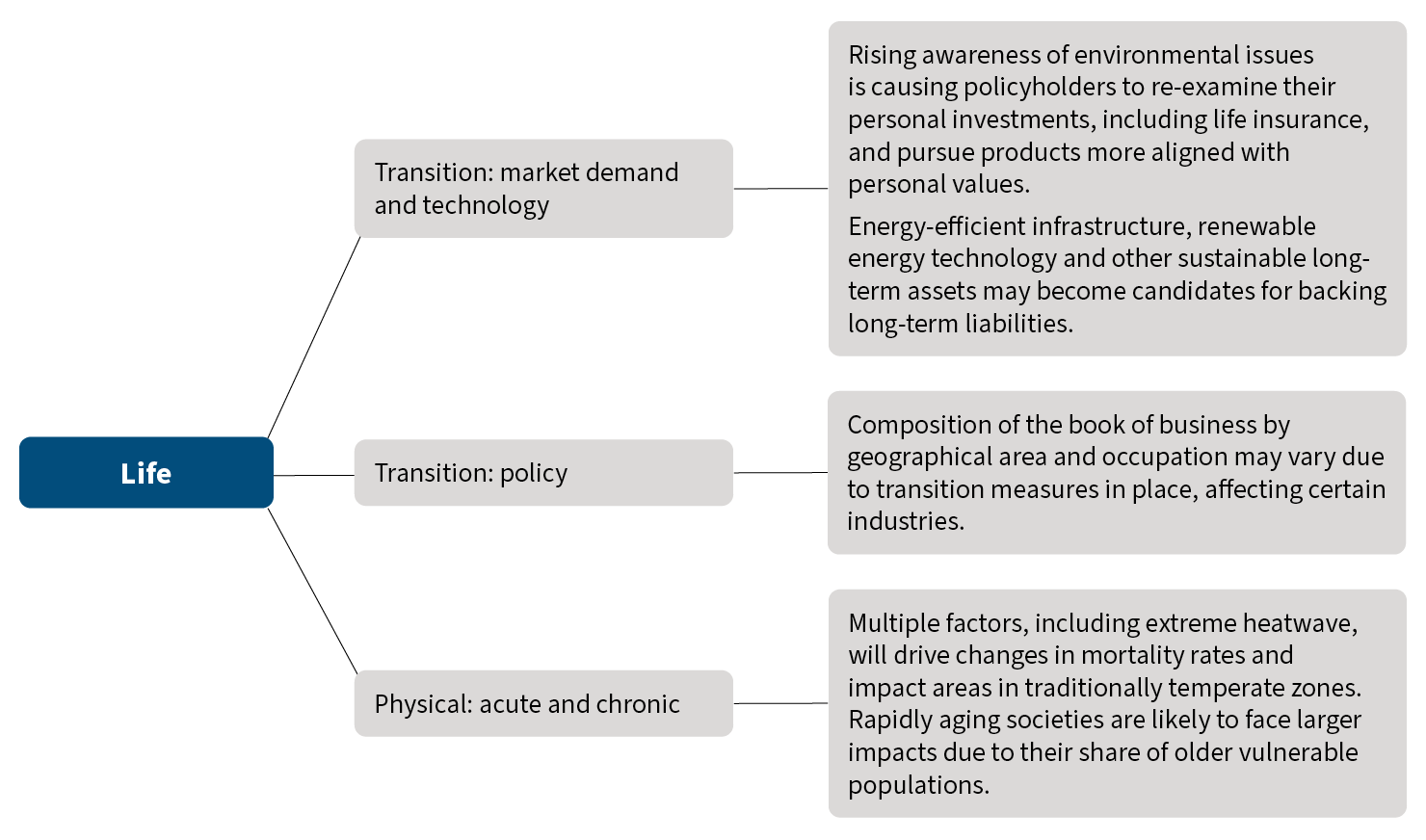

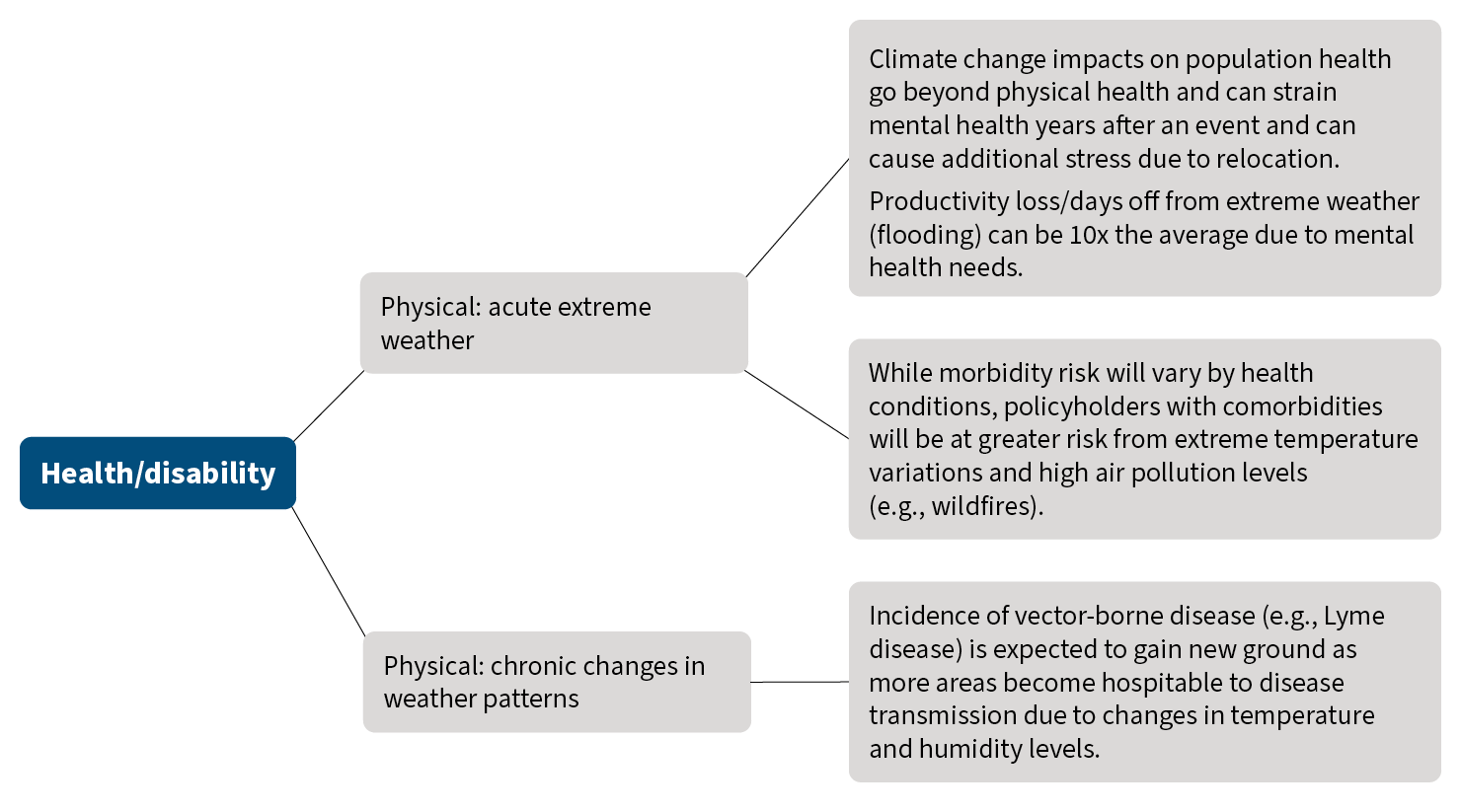

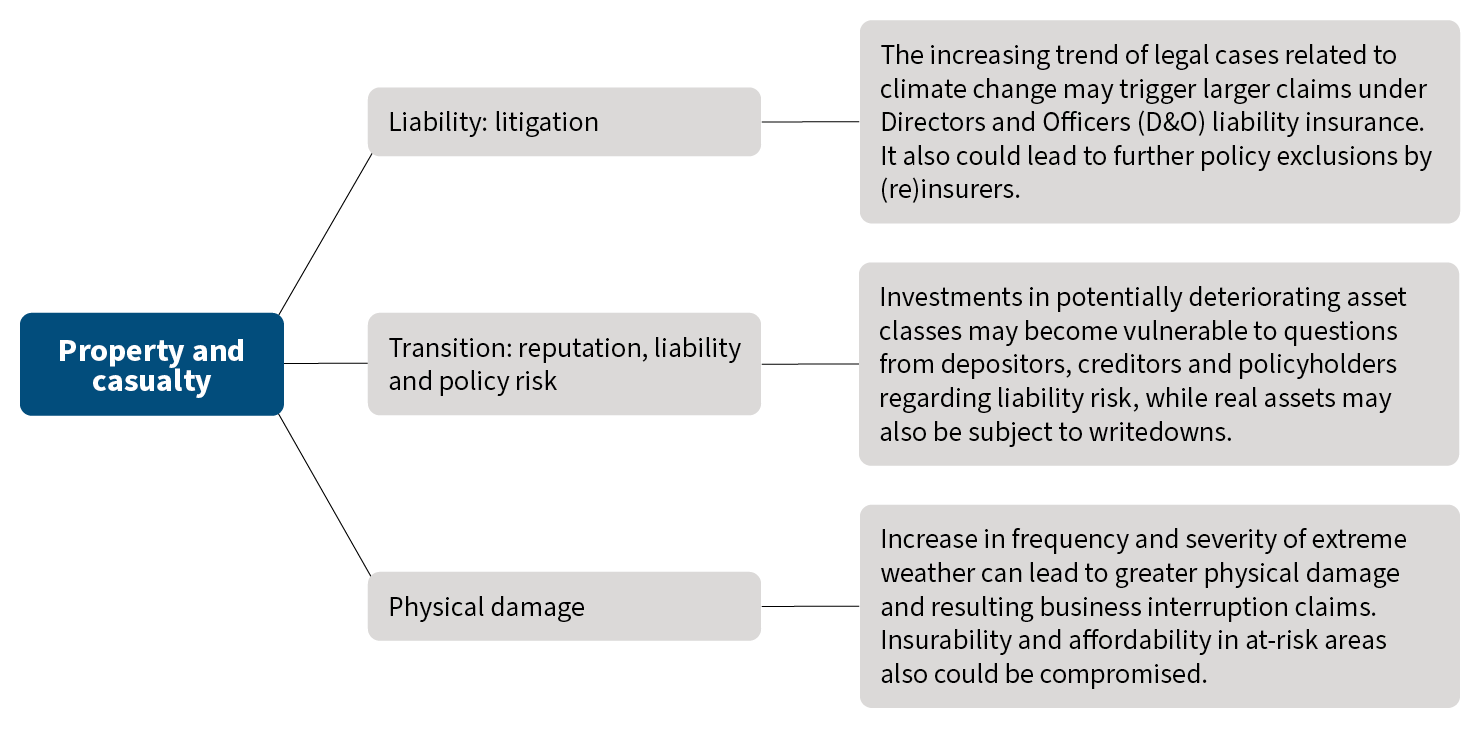

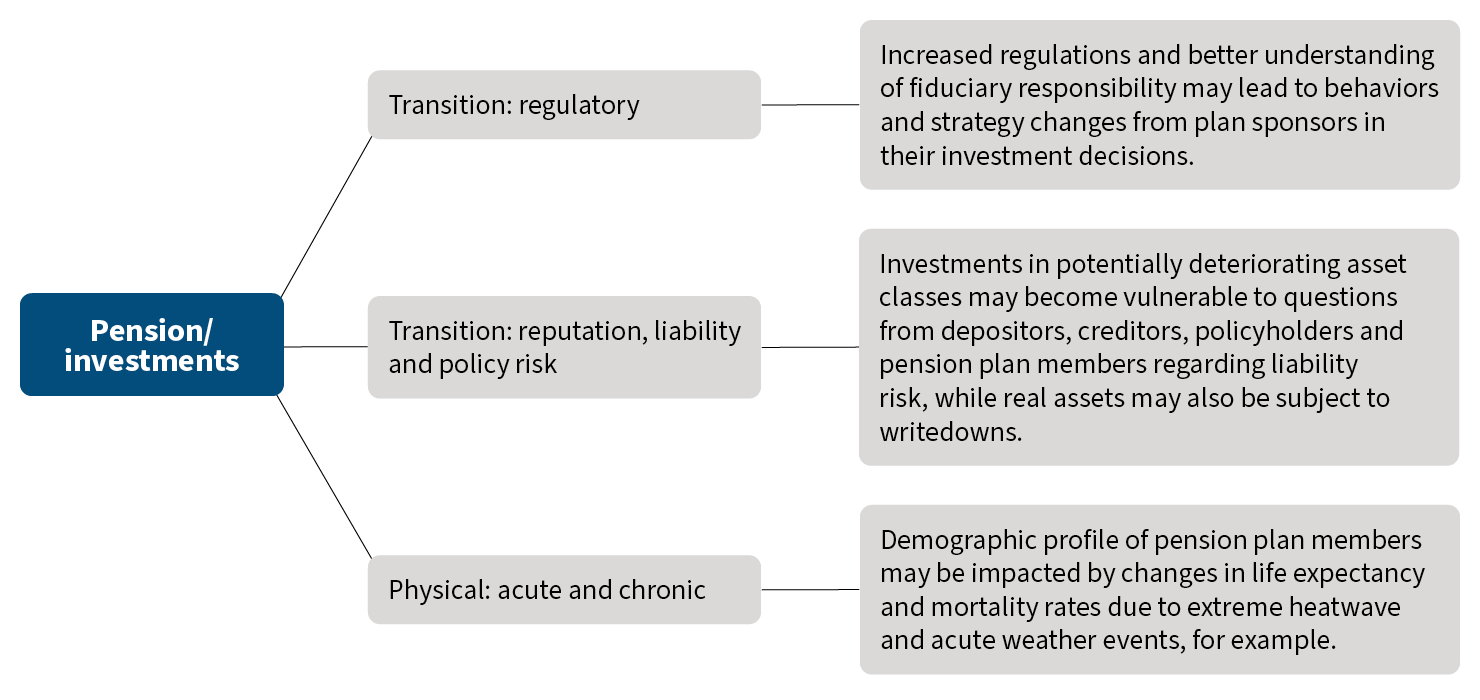

With an increasing awareness of the interdependencies of climate risks, their systemic nature creates impacts far beyond physical damage and business interruption that should not be overlooked to mitigate long-term insurability and affordability of insurance offerings. Figures 1, 2, 3 and 4 illustrate how life, health, P&C (re)insurance and pension plans are exposed to the physical, transition and liability risks presented in the TCFD, and how they can play a role in building resilience through their insurance and investment activities.

Figure 1: Risk Exposures for Life

Sources: Swiss Re Institute. Special Feature: It’s Existential—Climate Change and Life & Health. Swiss Re, May 22, 2019.

Booth, Claire, Neil Cantle, Dana-Marie Dick, Ian Penfold, Natasha Singhal, and Vidyut Vardhan. Risk Metrics for Climate Change. Milliman, May 2020.

Figure 2: Risk Exposures for Health and Disability

Sources: Decent, Dana, and Blair Feltmate. After the Flood: The Impact of Climate Change on Mental Health and Lost Time from Work. Intact Centre on Climate Adaptation, June 2018.

Booth, Claire, Neil Cantle, Dana-Marie Dick, Ian Penfold, Natasha Singhal, and Vidyut Vardhan. Risk Metrics for Climate Change. Milliman, May 2020.

Where to Start?

Building value, creating positive impact and fostering growth in a world that is sometimes referred to as a VUCA world (volatile, uncertain, complex and ambiguous) can be facilitated by data collection, risk metrics, and ongoing climate change assessment and monitoring. The disclosure framework the TCFD proposes represents an excellent starting point for insurers and pension plans to become more comfortable with climate change risks and their potential impact on long-term financial performance. It is also compatible with many existing actuarial processes like the ORSA and can contribute to the development of meaningful risk metrics over and above those used in the Actuaries Climate Index (ACI).

In addition, on governance structures, policies and practices, actuaries are well-positioned to assume a senior climate officer’s role within the risk area of insurers; particularly, those with strong risk backgrounds and climate risk knowledge should be considered for these positions. Or, looking at Barbara Zvan’s7 prior experience in Canada’s Expert Panel on Sustainable Finance, actuaries also might be well-suited for leadership roles in sustainable finance.

TCFD adoption, which is currently voluntary in most jurisdictions, continues to grow among all industries, including insurance. One area that lags in terms of disclosures is assessing the resilience of strategy to climate change risks, which is likely to receive increased attention as organizations become familiar with the full internal benefits of this disclosure exercise.

There is no magic formula, but starting somewhere and starting now with existing processes and disclosure frameworks may be a good place to start. The exact impact on severity, frequency and timing of climate-related risks continues to be unknown—at least beyond what can be reliably estimated using historical data. But what we know about these difficult-to-assess risks is their nonlinearity, complexity and compounded nature. While the lack of comparable and granular data may still be an ongoing issue, uncertainty about the future should not foster a culture of complacency. Instead, exploratory risk analysis using scenario analysis may become a valuable exercise for organizations. The largest benefit may likely accrue to those who internalize the process—through integration with strategy and overall risk management—rather than those who engage in this exercise for the sole purpose of external reporting.

Acknowledgments to the team of collaborators who made valuable contributions to the text. All are members of the Climate Change and Sustainability Committee at the Canadian Institute of Actuaries:

Gaetano Geretto, FSA, CERA, FCIA

Anna Marie Beaton, ASA, FCAS, FCIA, MAAA

Frances Fu, FSA, FCIA

Tulio Walles, FSA, FCIA

André Choquet, FSA, FCIA

Frédéric Matte, FCAS, FCIA

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

References:

- 1. Task Force on Climate-related Financial Disclosures. Recommendations of the Task Force on Climate-related Financial Disclosures. Financial Stability Board, June 2017. ↩

- 2. Gutterman, Sam, Joe Kennedy, Rob Montgomery, Priya Rohatgi, and Max J. Rudolph. The Task Force on Climate-related Financial Disclosures (TCFD)—What Actuaries Need to Know. Society of Actuaries, August 2020. ↩

- 3. The IPCC and the IEA produced global emission scenarios tied to specific temperature increase targets. These models are updated regularly to provide the latest scientific evidence of climate change impacts and future risks, and options for climate adaptation and mitigation. ↩

- 4. A “disorderly” transition could result from several factors, including sudden and unexpected changes in the costs of low-carbon solutions, level of carbon tax and/or global energy prices. This, in turn, would expose carbon-intensive assets to a significant risk of stranding. ↩

- 5. Surminski, Swenja, Laurens M. Bouwer, and Joanna Linnerooth-Bayer. 2016. How Insurance Can Support Climate Resilience. Nature Climate Change 6, 333–334. ↩

- 6. United Nations Office for Disaster Risk Reduction. Cadre d’Action de Sendai Pour la Réduction des Risques de Catastrophe 2015–2030. United Nations, 2015. ↩

- 7. Barbara Zvan is now CEO of the Universities Pension Plan in Ontario. ↩

Copyright © 2021 by the Society of Actuaries, Chicago, Illinois.