Financially Literate?

A look at the public’s understanding of financial products and tools

December 2019/January 2020A key way to maintain a healthy mind is to never stop learning. When it comes to financial education, this same mantra is also the key to financial stability.

In order to achieve financial stability, new knowledge must be acquired to make sound financial decisions. Priorities, income and expenses change throughout life, and different knowledge is required to wisely make financial decisions at various stages.

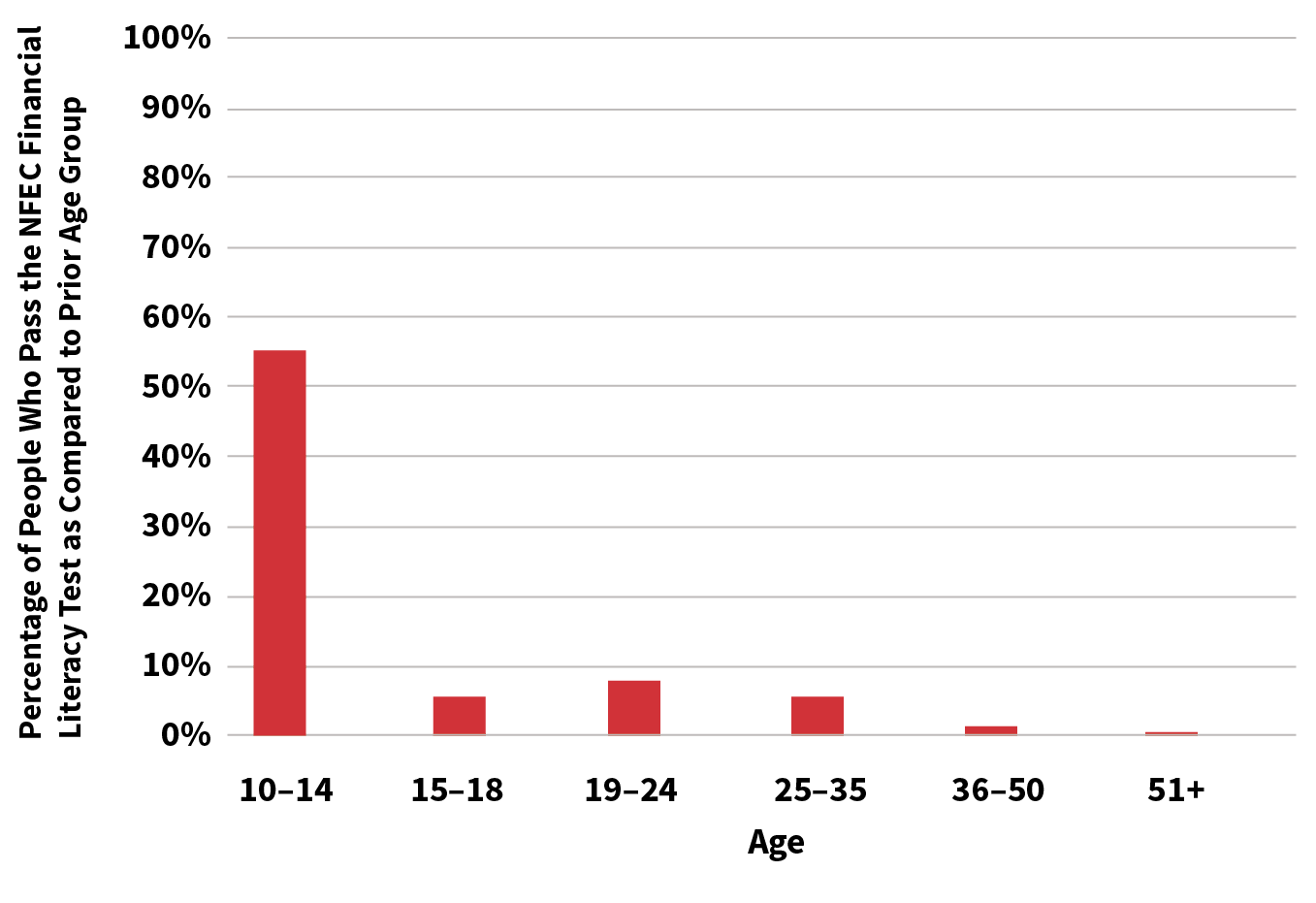

However, research shows that in reality, less financial knowledge is acquired with age (see Figure 1). After the ages of 25 to 35, people learn very few new financial insights. Yet the financial instruments used by those over age 35 dramatically differ from the financial tools commonly used up to that point in life. Additionally, the tools used by those older than 35 are significantly more complex in features and more costly in penalties. Technology also has enabled an increased array of choices in recent generations.

Figure 1: Growth in Financial Knowledge

Financial capability defines the level of knowledge needed to make financial decisions that are best suited to one’s situation and progress toward achieving financial stability. Different financial products are available and appropriate depending on the situation, as well as the past behavior and available assets of the individual. Financial capability can be considered within the context of a maturity model with stages that include basic, intermediate, capable, well-equipped and highly knowledgeable levels of understanding. Each level progresses in terms of the complexity of financial instruments understood, but additional tools also enable a higher ability to build and maintain assets that can withstand hardship events and shocks.

Basic Knowledge of Financial Instruments

The first stage of financial capability, basic knowledge, includes the ability to create and follow a budget, balance a checking account and understand the importance of savings. This stage of knowledge is typically sufficient to manage monetary assets up to age 18. While the tools may be basic in application, they are not always applied in practice. According to the FINRA Foundation National Financial Capability Study, 19 percent of individuals in the United States report they spent more than their income in the past year. 1

Effective use of banking products is a major hurdle in achieving basic financial capability. As previously stated, almost one-fifth of people in the United States are unable to keep their spending within their income. To fund the difference, almost one-fifth of checking account holders are heavy overdrafters who pay more than three fees a year. Most of these heavy overdrafters are younger than age 35, and the fees assessed comprise almost a full week of annual income.2

A Gen Z Approach to Financial Literacy

We started our company, Zogo, when we were only 18 years old in an attempt to solve our own personal finance problems. Growing up, no one taught me or my peers anything about financial literacy. At home, our parents didn’t really talk to us about 401(k) accounts or credit scores. Sure, our team members all took some form of financial literacy classes in high school, but the classes felt like lectures and were too boring to be effective.

When we learned that a lot of big corporations, especially banks and credit unions, spent millions of marketing dollars sponsoring financial literacy classes, we were shocked. These corporations were trying to put their brands in front of Gen Z, but in reality, these classes weren’t teaching financial literacy or spreading their brand.

So, we got to work trying to teach our generation financial literacy. We developed Zogo to make financial literacy learning fun, and also to help our corporate partners better reach Gen Z.

After a lot of testing, we built a financial literacy app that pays kids to learn. We break down complicated financial concepts into more than 300 bite-sized modules that meet young people where they are—on their phones. These modules start with easy concepts like budgeting, but they grow more complex as teenagers advance and make their way through the app.

Users start each module by learning five concepts before taking a five-question quiz. Kids earn points in the form of pineapples as they complete modules. They can redeem these points for rewards such as gift cards.

Our mission is to improve youth financial literacy nationwide, and we’re doing it together with financial institutions.

Mastery of a checking account must be accompanied by discipline in maintaining a savings account. In the United States, 46 percent of individuals lack a rainy day fund.3According to a 2017 GOBankingRates survey, more than half of Americans (57 percent) have less than $1,000 in their savings accounts.4 Withstanding and recovering from economic shocks are consequently difficult, and worry about such events also increases stress levels.5 The 2017 Global Benefits Attitudes Survey reported 59 percent of people worry about their financial futures, and 34 percent cite financial concerns as negatively affecting their lives—lack of a savings net can mean homelessness with one unexpected hardship.

Intermediate Financial Capability

Quite often, a solution used to address an inability to follow a budget or to fund unexpected expenses is to access credit. The entry-level product many people select is unsecured credit—a credit card. Responsible usage of a credit card requires an intermediate level of financial knowledge—specifically, the ability to understand interest rates and credit terms.

Just over half (51.64 percent) of the respondents to a survey from the National Financial Educators Council correctly answered that loan payments are based on interest rate and term. Use of credit card, student loan and other credit products without this level of knowledge has far-reaching and long-term effects for the future financial stability of an individual. The negative impact of inconsistent payments or nonpayments on a credit bureau report and credit score can reduce credit options for seven or more years, and can be a very costly lesson in terms of future interest rates for credit extensions. Not understanding payment options can have ramifications for 20+ years for student loan holders.

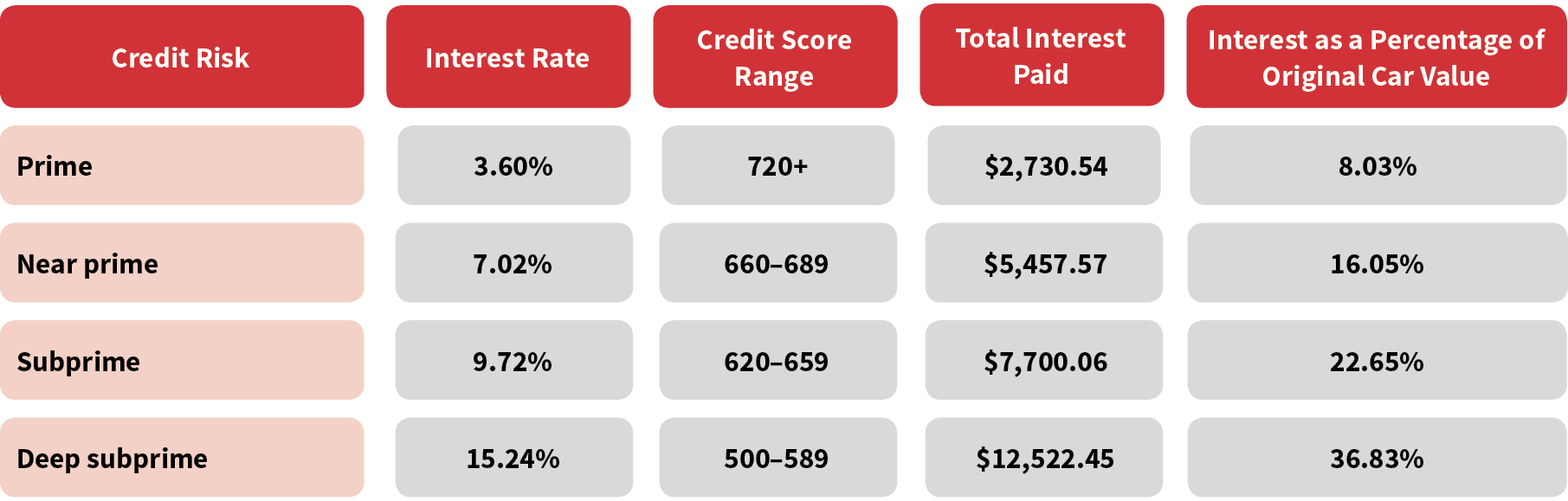

Individuals with low credit scores, indicative of late payments or defaults, are considered higher credit risks and receive higher interest rates for credit solutions. Those with credit scores above 760 are considered prime borrowers with low credit risk, and therefore they receive the best interest rates. A careless or inconsistent approach to managing credit commitments will result in decreases in credit scores and can be very costly. For example, the difference in interest between a deep subprime rate and prime rate on a car loan can be five times more over a 60-month term for an average priced car (see Figure 2).

Figure 2: Interest Paid Over the Full Term of Car Loan by Credit Rating

Source of interest rate: Wamala, Yowana. Average Auto Loan Interest Rates: 2019 Facts & Figures. Value Penguin, September 3, 2019 (accessed September 16, 2019).

Capable Knowledge of Financial Instruments

A capable level of knowledge in consumer finance translates into an ability to amortize interest and understand compounding interest. These concepts are critical to understanding mortgages, CDs and bonds, and are important in life stages when building assets is the focus—usually during the prime earning years of ages 25 to 50. A common product used to build assets in this life stage is a mortgage—the credit product used to finance the largest purchase typically made throughout life. Small differences in rates for such a large purchase with an extended life of repayment can be significant. The difference in credit score between a prime and deep subprime mortgage can yield a 2.5 percent differential in interest rate, which can double the interest expense over the life of the mortgage.

There is a clear lack of understanding of financial products that simultaneously exists with a high level of usage.

There is a clear lack of understanding of financial products that simultaneously exists with a high level of usage.While 63.8 percent of properties in the United States are owner-occupied housing, according to the U.S. Census Bureau,6 a survey by TheKnowledgeAcademy with YouGov cites that only 36 percent of people were confident they understood amortization.7 This again highlights how people use financial products without a true understanding of their complexity and how exactly they work. Furthermore, these financial tools are used during the life stages at which new financial knowledge ceases to be acquired (after ages 25 to 35).

Very different and more complex products are appropriate and beneficial past age 35—specifically, different types and uses of life insurance, health insurance vehicles and retirement accounts. According to a health insurance literacy study, only 4 percent of Americans could correctly define co-pay, deductible, coinsurance and out-of-pocket maximum.8 About one-third of Americans do not understand life insurance products,9,10 and only 4 percent of respondents answered seven or more questions out of 10 correctly regarding disability insurance.11 Long-term care and disability insurance can be a supplement to Social Security disability benefits, and it is often necessary to sustain costs of living due to a health crisis—a common hardship faced by many.

Well-equipped in Financial Knowledge

“Saving for retirement” is a common phrase. In reality, savings vehicles are not adequate to grow the capital necessary to achieve sufficient funds to enable retirement. The terminology itself is deceiving, because investing and the accompanying risks associated with a higher return are necessary to accumulate the larger sums needed to support retirement. The terminology is a reflection of the need for consumers to connect with a simpler idea than risk-based returns. Timing of the acquisition of this knowledge greatly affects financial stability and the building of generational wealth. Assuming an 8 percent annual return, an investment with a constant contribution of $400 starting at age 25 until age 60 would return $923,000, vs. $382,000 if the individual started contributing at age 35 instead of 25.

A report by the Stanford Center on Longevity12 found that nearly one-third of baby boomers had no money saved in retirement plans in 2014. Nonetheless, the possession of a retirement account does not translate into financial capability, as demonstrated with other financial instruments. Common investments for retirement accounts include stocks, mutual funds and index funds. Yet, according to one survey, only 39 percent were confident they understood mutual funds,13 and 17 percent do not understand the difference between a mutual fund and an exchange-traded fund (ETF).14 While there is usage of these financial tools, there is not a clear understanding of what the tools are.

An additional consideration for long-term financial stability is tax consequences for different investment tools, which can vary greatly and have a large impact on overall wealth due to compounding and time. An understanding of tax consequences, contribution limits and limitations on access to funds is critical to making wise investment decisions, particularly for instruments intended to enable retirement.

Other factors requiring the continued acquisition of financial knowledge are:

- The increased complexity of products used during ages 36 to 50

- Technology

- The changing tax code

The last significant tax reform in the United States was more than three decades ago, and views on investing must adjust with changes in tax laws. The tax code had been relatively slow changing, and consumers adjusted their knowledge and strategy to what they perceived to be a stable factor. But we are currently in a period of substantial change in tax laws.

Additionally, technological changes are enabling previously sophisticated and esoteric financial products to be widely available and sold as mass market retail products. Over a span of 26 years, the development of equities derivatives—combined with electronic trading—brought a once esoteric product to small investors. The daily volume of derivatives contracts overseen by the Options Clearing Corporation, the clearinghouse for all exchange-related options, went from 500,000 on average in the entire year of 1982 to 30,006,663 in a single day in 2008. This was a result of changes in regulations and the rise of online brokers. More recently, the VIX index was created to reflect market volatility. Now, anyone can “invest” funds in volatility. How do you explain buying volatility through futures contracts?

Highly Knowledgeable

Lastly, the focus in later stages of life is on the protection of assets, income in retirement and financial stability of future generations. An understanding of the business cycle and its effects on investments is instrumental in the timing of withdrawals of funds for liquidity needs without greatly reducing total assets. Furthermore, a well-grounded understanding of futures, geographic and sector risk, and yield curves can help in optimizing asset allocations to maximize return in all phases of the business cycle. It is at this stage in life when new options for financial instruments such as reverse mortgages, annuities and trusts become relevant. Custodial accounts and other tools enabling the transfer of wealth to coming generations are also helpful in achieving goals of sustainable wealth at this stage.

There is a clear lack of understanding of financial products that simultaneously exists with a high level of usage. Only 40 percent of respondents to the Advanced Financial Education Test answered questions correctly to achieve a passing score of 70 percent on basic financial knowledge, but more than 93 percent of Americans have a bank account. Financial capability is important at a personal level, as lack of financial knowledge can cause monetary hardships, be the reason for rejection for a job or promotion due to a background check, cause a deterioration in health as a result of stress, and determine whether the concrete ceiling of poverty can be broken.

Collectively as a society, lack of financial knowledge increases the extremity of credit crises, disenfranchises populations of citizens, increases health care costs, contributes to volatility and instability in markets, and raises amounts of government support.

Financial capability is not only important on the individual level, but also as a societal asset. The answer to whether an individual is financially capable should not be a “yes” or “no,” but rather a range relevant to their economic situation and stage in life. Continuing to learn in later life stages is critical to financial stability and building wealth.

The ideal situation would be for all consumers to understand the products available for their purchase and how best to leverage them for their financial goals. However, this is an immense body of knowledge to acquire.

One solution to a lack of financial knowledge would be to simplify products to enable consumers to more easily grasp product features and purpose. However, financial products have evolved and will continue to evolve to serve a number of purposes from financing large-scale public works to protecting nest eggs from taxes. With a large market of small investors available to provide funding and active litigation when every contingency is not addressed in contracts, complexity with widespread availability is the result. Furthermore, the needs of both counterparties in a financial transaction must be satisfied. While it is simpler to pay the same amount each pay period, the cost of funds and missed opportunity costs change each pay period. This mismatch in needs between borrower and lender alone will spur innovation and complexity. Simplified products are not sufficient to serve all financial needs or legally protect all parties. We need something more.

Increasing complexity can also be attributed to complex tax laws, periods of high volatility in markets and an effort to differentiate products amidst increasing levels of competition. Having a financial mentor; a knowledgeable and trusted adviser; or engaging a financial services professional to transfer knowledge, guide decisions and assist in increasing financial knowledge is necessary for financial security.

References:

- 1. Lin, Judy T., Christopher Bumcrot, Tippy Ulicny, Gary Mottola, Gerri Walsh, Robert Ganem, Christine Kieffer, and Annamaria Lusardi. The State of U.S. Financial Capability: The 2018 National Financial Capability Study. FINRA Investor Education Foundation, June 2019 (accessed September 16, 2019). ↩

- 2. Hackenbracht, Joy, Thaddeus King, Andrew Scott, Rachel Siegel, and Susan Weinstock. Heavy Overdrafters: A Financial Profile. The Pew Charitable Trusts, April 2016 (accessed September 16, 2019). ↩

- 3. Supra note 1. ↩

- 4. Huddleston, Cameron. More Than Half of Americans Have Less Than $1,000 in Savings in 2017. GoBankingRates, September 12, 2017. ↩

- 5. Supra note 1. ↩

- 6. U.S. Census Bureau. Population Estimates, July 1, 2018 (V2018). U.S. Department of Commerce (accessed September 16, 2019). ↩

- 7. Emmatty, Amy. Americans Are Confident About Their Understanding of Financial Terms. YouGov, February 27, 2018 (accessed September 16, 2019). ↩

- 8. Policygenius. 4 Basic Health Insurance Terms 96% of Americans Don’t Understand. Policygenius, January 24, 2018 (accessed September 16, 2019). ↩

- 9. Lynch, Cristy. Survey: Why Most American Don’t Have Individual Life Insurance Coverage. helloBestow, February 16, 2018 (accessed September 16, 2019). ↩

- 10. Brown, Mike. 54% of Americans Own a Life Insurance Policy, But One-third Not Exactly Sure How It Works. LendEdu, August 28, 2018 (accessed September 16, 2019). ↩

- 11. Babbel, David F. Financial Security for Working Americans: An Economic Analysis of Insurance Products in Workplace Benefits Programs. Charles River Associates, July 2011 (accessed September 16, 2019). ↩

- 12. Streeter, Jialu, and Amal Harrati. Disentangling Differences in Retirement Preparedness Between Baby Boomers and Silent Generation. Stanford University, October 2018 (accessed September 16, 2019). ↩

- 13. Supra note 7. ↩

- 14. O’Brien, Sarah. Many Investors Don’t Know the Difference Between MutualFunds and ETFs—Here’s Why It Matters. CNBC, October 5, 2018 (accessed September 16, 2019). ↩

Copyright © 2019 by the Society of Actuaries, Chicago, Illinois.