Putting a Price Tag on Health

Value in health care is more than finding cost reductions

December 2018/January 2019Statements of fact and opinions expressed herein are those of the individual author(s) and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

For health actuaries, questions about the costs and financing of health care are a daily concern. Much of the pressure to understand cost drivers and control costs has fallen upon the health insurance industry, which in turn places much of the burden squarely on the shoulders of health actuaries. As we work to respond to this situation, it’s important to remember that the cost for any good or service, health care included, is only one part of the equation. The other critical component is what you get for your money.

Roles and Responsibilities

What do we hope to attain when we spend money on health care? The answer may seem obvious, but it is worth reflecting on. Health, as defined by the World Health Organization, is “a state of complete physical, mental and social well-being and not merely the absence of disease or infirmity.”1 Health promotion, then, is not merely about healing wounds, eradicating

disease or extending life spans, but is instead concerned with improving overall well-being. Patients are well within their rights to expect that the health care goods and services they purchase promote their health.

Patients have their own individual goals and definitions of health, but helping patients achieve those goals is the ultimate purpose of the health care industry, a purpose that unites all stakeholders in the system. At the end of the day, “health service organizations are social enterprises with an economic dimension rather than an economic enterprise with a social dimension.”2

While the purpose of the health care industry is to produce health, the purpose of the insurance industry is to produce financial security (a significant contributor to overall well-being). This gives insurance a unique role in this system, but one that should ultimately serve the same end. The distinctions between the roles of the insurance industry and the health care industry are blurring by the day as providers increasingly take on some of the financial risks of health care delivery, and as insurers continue to be involved in determining what will and will not be paid for through benefit design, network design, utilization review, medical necessity criteria and other processes and criteria.

Defining Value

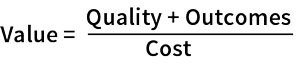

Value has become somewhat of a buzzword in health care as of late, though its emergence as a prominent consideration is not without merit. One popular definition posits that value is the measure of “health outcomes achieved per dollar spent,” and this definition is frequently expanded to encompass quality of care as well.3,4 In this framework, the quality of care and health outcomes are the numerator, and cost the denominator. We can think of achieving value in health care not necessarily as a cost reduction exercise, but as an optimization problem, where neither cost nor outcomes should be considered in isolation. In this sense, the real conundrum is not just how much we’re spending, but what we get for what we’re spending.

Indeed, if infant mortality, cancer and heart disease were eradicated, perhaps many of us would be willing to pay much more for such fine results. And yet, as spending on health care in the United States has pulled away from other Organisation for Economic Co-operation and Development (OECD) countries since the 1980s, its outcomes have not. The United States spends a higher proportion of its gross domestic product (GDP) on health care than any other country, but our life expectancy ranks 27 out of 35 countries in the OECD. Compared to other OECD countries, we also have the fourth-highest infant mortality rate and the ninth-highest likelihood of premature death from a variety of causes, such as heart disease and cancer.5

Cost and Quality: Not a Zero Sum Game

In a value-based framework, what criteria should be used to evaluate new health care interventions? In the actuarial world (as in other domains with an economic dimension), a common measuring stick is return on investment (ROI). If a particular intervention is expected to result in cost avoidances that exceed the costs of implementation, spending on that intervention may be justified on the expectation of positive financial outcomes. On the other hand, health care providers often focus more on quality, safety and effectiveness. If a particular intervention can be proven to be necessary, safe and effective, provision of that intervention may be justified on the expectation of improved quality of care and positive health outcomes. Health economists commonly use cost-effectiveness analyses, which measure the cost of an intervention per quality-adjusted life-year (QALY), as a way to relate outcomes to costs, but this method has not gained widespread adoption in actuarial circles (with some exceptions). When an intervention is evaluated only for cost impacts or only for health outcomes, it’s possible to wind up investing scarce resources in interventions that have low overall value.

Additionally, focusing on costs alone can result in systematic underinvestment in improvements to delivery systems and public health interventions that are often complex, difficult to evaluate and have longer time horizons for their intended effects.6 One study found the majority of cost impact analyses that are published relate to new technologies or drugs, and only 10 percent of such studies evaluated delivery improvements or public health interventions, with many of the studies in that 10 percent focusing on clinical prevention7 (see Figure 1). These types of interventions do not lend themselves well to experimental study designs, have externalities that are difficult to measure and often co-occur with other interventions, making it difficult to directly measure effects and attribute them to particular interventions. The relatively low volume of evidence for ROI for these types of investments may speak more to the overall complexity of measuring them than to their actual value.

Figure 1: Types of Interventions in Published Health Care Cost Impact Studies

If one were to consider cost and health outcomes as bookends of a financial-clinical continuum, one would quickly dismiss this as a nonviable framework. A health care system could focus exclusively on the cost of care at the expense of clinical outcomes (after all, isn’t the cheapest care no care at all?) or it could focus exclusively on clinical care with no regard to costs (using all the latest technologies in every circumstance). It is doubtful that many believe we should operate at either extreme, but there are many situations where we might not think to explicitly consider both sides and may inadvertently promote interventions that are not well-balanced to provide value.

Finding Balance

One approach to evaluating health care interventions that could serve to unify interests in both cost and health outcomes is the STEEPE criteria, an analytical framework outlined in 2001 by the Institute of Medicine (now called the Health and Medicine Division) and widely adopted by health care providers since then. The STEEPE criteria suggest that health care should be:8

- Safe. Avoid injuries to patients from the care that is intended to help them.

- Timely. Reduce waits and sometimes harmful delays for both those who receive and those who give care.

- Effective. Provide services based on scientific knowledge to all who could benefit and refrain from providing services to those not likely to benefit.

- Efficient. Avoid waste, including waste of equipment, supplies, ideas and energy.

- Patient-centered. Provide care that is respectful of and responsive to individual patient preferences, needs and values, and ensure that patient values guide all clinical decisions.

- Equitable. Provide care that does not vary in quality because of personal characteristics such as gender, ethnicity, geographic location and socioeconomic status.

In this framework, efficiency clearly makes room for consideration of the cost of care, and the other five aims are helpful guideposts as we make determinations about how to allocate scarce health care resources. Interventions that don’t fit into this framework may prove to be of low value, even if they produce cost savings, while interventions that achieve these aims may prove to be of high value even if they do not produce cost savings.

In more recent years, the Institute for Healthcare Improvement developed and popularized the notion of the Triple Aim—the idea that health system performance can be optimized by focusing on interventions that improve the patient experience of care, improve the health of populations and reduce the per capita cost of health care.9 This framework places a greater emphasis on population-level outcomes while still connecting the importance of balancing cost management with the importance of health care quality and outcomes.

Preventive care provides a good case study for considering this balance. It’s widely believed that preventive care pays for itself—that by preventing the occurrence of new problems, or by preventing the worsening of current problems, we avoid unnecessary emergency room visits, hospitalizations and long-term complications (and thus, costs). However, a major study by the Robert Wood Johnson Foundation published in 2009 looked at more than 500 studies of preventive care published in peer-reviewed journals and found this conventional wisdom to be false. The researchers found that outcomes for preventive care were good at reducing prevalence of disease and increasing longevity, but few studies showed strong evidence of cost savings.10 The researchers note that many preventive care interventions are cost-effective, even if not cost-saving. To quote Aaron Carroll, M.D., a prominent health researcher, medical professor and columnist for The New York Times: “But money doesn’t have to be saved to make something worthwhile. Prevention improves outcomes. It makes people healthier. It improves quality of life. It often does so for a very reasonable price. … Sometimes good things cost money.”11

Doing Our Part

Health care providers have been focused on providing quality care for their patients. However, in an environment with limited resources and the need to efficiently allocate health care dollars, providers have increasingly needed to consider costs. The Institute for Healthcare Improvement’s Triple Aim framework, which highlights the need to simultaneously improve the patient experience, the health of populations and reduce the per capita cost of health care, has become highly influential.12 The transition from fee-for-service payment models to value-based payment models is well underway, including accountable care organizations (ACOs) that are taking on financial responsibility for the outcomes they produce for Medicare beneficiaries.13 Initiatives such as the Choosing Wisely campaign, a joint effort of leading medical societies spearheaded by the American Board of Internal Medicine, have developed widely respected guidelines for avoiding unnecessary health care services and procedures.14 Leading health research organizations such as The Dartmouth Institute are studying unwarranted variation in how health care resources are used.15

Perhaps as expectations grow for health care providers to consider the costs of care, it would be wise for actuaries and other leaders in the health insurance industry to join them by giving greater consideration to improving health outcomes. All parties make unique contributions that keep the entire health care apparatus humming along. But as the lines between roles continue to become less clear, we would do well to ensure we’re all working on the same equation to achieve value for patients.

Special thanks to Jordan Paulus, Steve Melek and Susan Philip for their helpful input and peer review of this content.

References:

- 1. World Health Organization. Constitution of WHO: Principles. World Health Organization, (accessed August 29, 2018). ↩

- 2. Darr, Kurt. 2004. Ethics in Health Services Management. 4th ed. Baltimore: Health Professions Press. ↩

- 3. Porter, Michael. 2010. What Is Value in Health Care? The New England Journal of Medicine 363, no. 26:2477–2481. ↩

- 4. Wehrwein, Peter. 2015. Value = (Quality + Outcomes) / Cost. Managed Care Magazine, August 16. ↩

- 5. Meisler, Laurie. Americans Die Younger Despite Spending the Most on Health Care. Bloomberg, August 2, 2017. ↩

- 6. Kaplan, Robert, and Michael Porter. 2011. The Big Idea: How to Solve the Cost Crisis in Health Care. Harvard Business Review, September. ↩

- 7. Brousselle, Astrid, Tarik Benmarhnia, and Lynda Benhadj. 2016. What Are the Benefits and Risks of Using Return on Investment to Defend Public Health Programs? Preventive Medicine Reports, 3:135–138. ↩

- 8. Committee on Quality Health Care in America, Institute of Medicine. 2001. Crossing the Quality Chasm: A New Health System for the 21st Century. Washington, D.C.: National Academy Press. ↩

- 9. Institute for Healthcare Improvement. IHI Triple Aim Initiative: Better Care for Individuals, Better Health for Populations and Lower per Capita Costs. Institute for Healthcare Improvement, (accessed August 29, 2018). ↩

- 10. Goodell, Sarah, Josh Cohen, and Peter Neumann. Cost Savings and Cost-effectiveness of Clinical Preventive Care. Robert Wood Johnson Foundation: The Synthesis Project, September 1, 2009, (accessed August 29, 2018). ↩

- 11. Carroll, Aaron. Preventive Care Saves Money? Sorry, It’s Too Good to Be True. The New York Times, January 29, 2018. ↩

- 12. Supra note 9. ↩

- 13. Gruessner, Vera. Private Payers Follow CMS Lead, Adopt Value-based Care Payment. HealthPayer Intelligence, October 17, 2016, (accessed August 29, 2018). ↩

- 14. The American Board of Internal Medicine Foundation. Choosing Wisely: A Special Report on the First Five Years. Choosing Wisely Initiative, October 26, 2017, (accessed August 29, 2018). ↩

- 15. The Dartmouth Institute. Variation in Health Care Delivery. The Dartmouth Institute, (accessed August 29, 2018). ↩

Copyright © 2018 by the Society of Actuaries, Chicago, Illinois.