Striking the Right Note

The past failures, present successes and future possibilities of the classic longevity instrument, the longevity bond

August/September 2017Systematic longevity risk is a key risk factor in many life insurance and pension products. For example, annuity providers are exposed to the risk that the mortality rates of pensioners will fall at a faster rate than anticipated in their pricing and reserving calculations. Yet annuities are commoditized products. They sell mainly on the basis of price (although factors such as service and credit rating are also considerations), and profit margins need to be kept low in order to gain and then protect market share. If the mortality assumptions built into the prices of annuities turn out to be gross overestimates, this cuts straight into the profit margin of annuity providers.

In principle, systematic longevity risk can be hedged with an appropriate hedging instrument. The classic hedging instrument is a longevity bond, an annuity bond paying coupons linked to a mortality index, such as the realized mortality experience of the national population of 65-year-olds on the issue date (with no return of principal), so that the payouts on the bond correlate highly with the payments an annuity provider needs to make on its annuity book.

In this article, we take a historical sweep over the market for longevity bonds, looking at past failures, current successes and what lessons can be learned for the future of this type of instrument.

The Past: The Classic Longevity Bond—A Disappointing Failure

One of the earliest attempts at creating a capital market in longevity-related instruments was the proposal to issue long-dated longevity bonds (or survivor bonds) made more than 15 years ago.1,2 As a reference population cohort dies out, the coupon amounts decline but continue in payment for a fixed term (in the case of longevity bonds) or until the entire cohort dies (in the case of survivor bonds). To illustrate, if after one year, 0.8 percent of the reference population has died out, the second year’s coupon payment will be 99.2 percent of the first year’s payment, and so on.

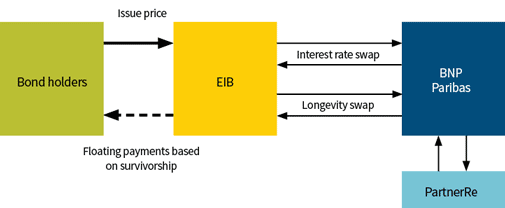

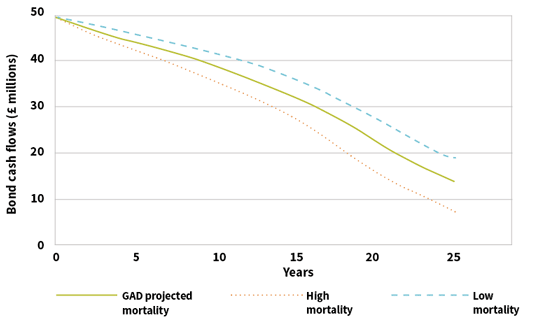

The first attempt to issue a longevity bond was in November 2004, when the European Investment Bank (EIB) attempted to launch a 25-year £540 million longevity bond with an initial coupon of £50 million. The reference mortality index was based on 65-year-old males from the national population of England and Wales, as produced by the U.K. Government Actuary’s Department (GAD). The structurer/manager was BNP Paribas, which assumed the longevity risk but reinsured it through Bermuda-based PartnerRe (see Figure 1). The target group of investors was U.K. pension funds. Figure 2 shows how the coupons might change on the bond: If mortality is lower than projected by the GAD, the coupons on the bond will decline by less than anticipated, and vice versa. The bond holder—for example, a pension fund paying pensions to retired workers—is therefore protected from the systematic longevity risk it faces.

Figure 1: The Structure of the European Investment Bank Longevity Bond

Source: Adapted from Blake, David, Andrew Cairns, and Kevin Dowd. “Living with Mortality: Longevity Bonds and Other Mortality-Linked Securities.” British Actuarial Journal 12, no. 1 (2006): 153–197.

Figure 2: Coupons on the European Investment Bank Longevity Bond

Source: U.K. Government Actuary’s Department

Problems

After a year of marketing, the EIB longevity bond had not generated sufficient demand to be launched and was withdrawn. There are a number of reasons for this, including the following.

Design Issues

The EIB bond had a number of design weaknesses that made the bond an imperfect hedge for longevity risk. The basis risk in the bond was considered to be too great. The bond’s mortality index was a single cohort of 65-year-old males from the national population of England and Wales. While this might provide a reasonable hedge for male pension plan members in their 60s, pension plans also have male members in their 70s and 80s, as well as female members.

Pricing Issues

The longevity risk premium built into the initial price of the EIB bond was set at 20 basis points.3 Given that this was the first ever bond brought to market, investors had no real feeling as to how fair this figure was. There was concern that the upfront capital was too large compared with the risks being hedged by the bond, leaving no capital for other risks to be hedged. In addition to hedging interest rate risk, this bond also hedged longevity risk, but the bond’s payments were in nominal terms and hence did not hedge inflation risk.

Institutional Issues

There was a range of institutional issues that the bond’s designers failed to confront. To start, the issue size was too small to create a liquid market. Market makers did not welcome the bond, because they believed it would be closely held and they would not make money from it being traded.

Further, the issuer did not consult widely enough with potential investors or their advisers before the bond was announced. Advisers were reluctant to recommend it to pension plan trustees. They said they welcomed the introduction of a longevity hedge but did not like the idea of the hedge being attached to a bond. Indeed, they were somewhat suspicious of capital market hedging solutions per se, preferring instead insurance indemnification solutions, such as a buy-out (an insurance company buys the pension plan liabilities and relieves the plan sponsor of all risks—investment, inflation, interest rate, as well as longevity risk—associated with running a pension plan) or a buy-in (an insurance company sells a bulk annuity policy to a pension plan, which is used to pay the pensions when due, and hence hedges only the longevity—and possibly also the inflation—risk). In other words, advisers and trustees were used to dealing with risk by means of insurance contracts that fully removed the risk concerned and were not yet comfortable with capital market hedges that left some residual basis risk. Fund managers at the time did not have a mandate to manage longevity risk, and similarly saw no reason to hold the bond.

The reinsurer, PartnerRe, was not perceived as being a natural holder of U.K. longevity risk. This turned out to be a rather significant point, since it was discovered that no U.K.-based or EU-based reinsurer was willing to provide cover for the bond, and PartnerRe itself was not prepared to offer cover above an issue size of £540 million.

Educational Issues

The longevity bond was a new concept that was completely unfamiliar to most players in the market. For it to be successful, a major educational effort would have been needed on all the issues already discussed, especially structure, basis risk, hedge effectiveness and liquidity. This education process needed to be broad enough to cover the entire industry and involve defined benefit (DB) plan sponsors, fiduciaries, investment consultants, plan actuaries and insurers.

Lessons Learned

The EIB bond was a very innovative idea, and it is disappointing that it was not a success. Nevertheless, important lessons have been learned from its failure. Two of the most important lessons relate to mortality indices and mortality forecasting.

Mortality Indices

The EIB bond’s actual cash flows would have been linked to the mortality of 65-year-old males from England and Wales. This single mortality benchmark was considered inadequate to create an effective hedge. It soon became apparent that what was needed was a set of mortality indices against which capital market instruments could trade. The most prominent attempt to do this was the LifeMetrics Indices launched in March 2007 by J. P. Morgan in conjunction with the Pensions Institute and Towers Watson.4 The indices comprise publicly available mortality data for national populations, broken down by age and gender. Both current and historical data are available, and the indices are updated to coincide with official releases of data. The indices cover the key countries—the United Kingdom, the United States, Holland and Germany—where longevity risk is perceived to constitute a significant economic problem. In launching LifeMetrics, J.P. Morgan recognized the critical importance of education and provided educational materials, including documentation, software, data and presentations, to the industry at no cost.

Mortality Forecasting Models

The EIB bond’s projected cash flows depended on projections of the future mortality of 65-year-old males from England and Wales. The U.K. GAD prepared these projections, but the model used to make these predictions was not published and the projections themselves were adjusted in response to expert opinion in a way that has not been made transparent. What was needed to complement transparent mortality indices were more transparent stochastic mortality forecasting models. This deficiency was addressed in subsequent years by a number of mainly academic researchers who developed and published different forecasting models.5

The Present: The Kortis Bond—A Modest Success

In December 2010, with the lessons learned from the EIB bond, Swiss Re launched an eight-year longevity-based bond valued at $50 million. To do this, it used a special purpose vehicle, Kortis Capital, based in the Cayman Islands. The bond was designed to hedge Swiss Re’s own exposure to longevity risk.

The bond holders are exposed to the risk of an increase in the spread between the annualized mortality improvement in English and Welsh males ages 75 to 85 and the corresponding improvement in U.S. males ages 55 to 65.6 The mortality improvements will be measured over eight years from Jan. 1, 2009, to Dec. 31, 2016. The bonds matured on Jan. 15, 2017,7 although there is an option to extend the maturity to July 15, 2019. The principal will be at risk if a Longevity Divergence Index Value (LDIV) exceeds the attachment point or trigger level of 3.4 percent over the risk period. The exhaustion point, at or above which there is no return of principal, is 3.9 percent. The principal will be reduced by a principal reduction factor (PRF) if the LDIV lies between 3.4 and 3.9 percent. See the sidebar for how to derive the LDIV.

If there is a larger-than-expected increase in the spread between the mortality improvements of 75- to 85-year-old English and Welsh males and those of 55- to 65-year-old U.S. males, the principal of the bond will be reduced. The exposure Swiss Re is hedging comes from different sources. For example, Swiss Re is the counterparty in a £750 million longevity swap with the Royal County of Berkshire Pension Fund that was executed in 2009, and consequently is exposed to high-age English and Welsh males living longer than anticipated. It also has reinsured a lot of U.S. life insurance policies and is exposed to middle-aged U.S. males dying sooner than expected. The longevity note provides a partial hedge for both exposures and will help Swiss Re reduce its regulatory capital. In exchange for putting their capital at risk, investors receive quarterly coupons equal to three-month London Interbank Offered Rate (LIBOR) plus a margin.

DERIVING THE LONGEVITY DIVERGENCE INDEX VALUE (LDIV)

The LDIV is the spread between the annualized mortality improvement in English and Welsh males ages 75 to 85 and the corresponding improvement in U.S. males ages 55 to 65. It is derived as follows.1

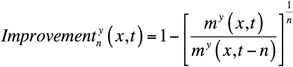

Let my (x,t) be the male death rate at age x and year t in country y. This is defined as the ratio of deaths to population size for the relevant age and year. Annualized mortality improvements over n years are defined as:

The annualized mortality improvement index for each age group is found by averaging the annualized mortality improvements across ages x1 to x2 in the group:

![]()

The LDIV is defined as:![]() where y2 is the England and Wales population aged 75 to 85, and y1 is the U.S. population aged 55 to 65.

where y2 is the England and Wales population aged 75 to 85, and y1 is the U.S. population aged 55 to 65.

The principal reduction factor (PRF) is calculated as:

![]()

1 Hunt, Andrew, and David Blake. “Modelling Longevity Bonds: Analysing the Swiss Re Kortis Bond.” Insurance: Mathematics and Economics 63 (2015): 12–29.

The Future: A Crunch Point Coming?

The Kortis bond was a success—but only one such bond has been issued to date, so the success at $50 million can only be described as modest. By contrast, there have been $200 billion of buy-outs and buy-ins globally between 2006 and 2016.8

Governments could consider helping to both encourage and facilitate the development of the longevity risk transfer market. In particular, they could play a pump-priming role, as argued some years ago by the U.K. Pensions Commission.9 For example, they could consider issuing longevity bonds to establish the riskless term structure for the longevity risk premium, as they do in the inflation-linked bond market in respect to the inflation risk premium. Similarly, the regular issuance of longevity bonds—even in a small size—would provide pricing points to catalyze the development of the market, in addition to providing value as a hedging instrument.

Of particular concern is extreme longevity risk associated with individuals older than 90—a risk that the private sector is unwilling to hedge. The government could consider helping by selling deferred annuities to this group. This would be a form of risk sharing between the state and the private sector. The state’s contribution would be to issue these instruments, leaving the private sector (life companies and the capital markets) to design better annuity products and trade longevity risk up to age 90. The main benefit from a capital market perspective of a government-issued longevity instrument would be to offer a standardized liquid benchmark that would help to establish the risk-free price of longevity risk at different terms to maturity.

So far, however, there has been little sign of progress on any of these fronts. This is unfortunate since it will lead to a crunch point in the near future. There are growing signs of a capacity constraint in the insurance and reinsurance markets for both buy-outs and buy-ins. The only way for this constraint to be relieved and for capital to be released in the (re)insurance industry so it can continue offering buy-outs and buy-ins is for longevity risk to be transferred to capital markets investors, such as sovereign wealth funds, insurance-linked securities investors, hedge funds and so on. Currently, this group of investors has shown only limited interest in longevity risk as an asset class—and the reasons for this and potential solutions have been explained in this article.

References:

- 1. Blake, David, and William Burrows. “Survivor Bonds: Helping to Hedge Mortality Risk.” Journal of Risk and Insurance 68, no. 2 (2001): 339–348. ↩

- 2. Blake, David, Andrew Cairns, Kevin Dowd, and Richard MacMinn. “Longevity Bonds: Financial Engineering, Valuation and Hedging.” Journal of Risk and Insurance 73, no. 4 (2006): 647–672. ↩

- 3. Cairns, Andrew, David Blake, Paul Dawson and Kevin Dowd. “Pricing Risk on Longevity Bonds.” Life and Pensions 1, no. 2 (2005): 41–44. ↩

- 4. http://www.llma.org ↩

- 5. Cairns, Andrew, David Blake, Kevin Dowd, Guy Coughlan, David Epstein, Alen Ong, and Igor Balevich. “A Quantitative Comparison of Stochastic Mortality Models Using Data from England & Wales and the United States.” North American Actuarial Journal 13, no. 1 (2009): 1–35. ↩

- 6. It is important to recognize that the Kortis longevity bond was not a true longevity bond in the sense we have described, because it involved transferring the risk associated with the spread (or difference) between the longevity trends for two different population groups rather than the trends themselves. ↩

- 7. The payoff of the bond depends on population mortality data for 2016 for England and Wales and the United States, neither of which is currently available (U.K. data are expected in July or August 2017; the United States is a lot slower at releasing data). ↩

- 8. Ben-Ami, Daniel. “Interview: Amy Kessler, Prudential Retirement.” Pensions & Investments Europe, December 2016. ↩

- 9. A New Pensions Settlement for the Twenty-First Century. Pensions Commission. The Stationery Office. (2005): Norwich, England. ↩