The Science of Project Management

Collaborating with project managers to achieve transformation goals

December 2020Photograph: iStock.com/juststock

Actuaries are living through an unprecedented time of change. Besides the megatrends in technology and market landscape, regulatory and accounting changes—such as principle-based reserving (PBR), U.S. Generally Accepted Accounting Principles (GAAP) long-duration target improvement (LDTI) and International Financial Reporting Standards (IFRS)—have been the catalysts for actuarial and financial transformations in recent years. For the past decade, U.S. insurance regulators have worked toward a more principle-based approach, and today, both PBR and LDTI are moving away from formulaic and/or locked-in valuation to model-based approaches.

The impact of these changes on insurance companies goes beyond compliance:

- External stakeholders, such as regulators, analysts and shareholders, will rely on the new standards to measure companies’ risks and performance. A new level of disclosure and analysis is required to show not only “the how” but also “the why” of companies’ financial results.

- The regulatory changes are forcing insurance companies to adjust how they measure and manage their own risks and business performance, from product pricing to risk management and even compensation programs. They also need to reassess their short-term and long-term business strategy through the lens of the new reporting regime.

- Management teams need the data and tools to gain actionable insights to effectively execute their business strategy and communicate financial results.

Many insurance companies have embarked on end-to-end actuarial and finance transformation initiatives to develop a comprehensive data infrastructure, integrated reporting processes and robust analytic capabilities to satisfy reporting and management needs. Actuaries going through the transformation programs often work side by side with data, system and finance teams. Increasingly, project managers also are pivotal collaborators for actuaries throughout planning, launching and executing transformation programs. However, many actuaries are still learning to collaborate with project managers, as the two professions provide different skill sets and attributes. This article highlights the value of project management and explores effective collaborations between actuaries and project managers.

Why Projects Fail

Not having effective project management is one of the primary reasons why projects fail. A 2020 Project Management Institute (PMI) survey suggests that “organizations that undervalue project management as a strategic competency for driving change report an average of 67 percent more of their projects failing outright.”1 Additional data points on how projects underperform or fail from PMI’s 2018 Pulse of the Profession report include:2

- 31 percent of projects do not meet their goals.

- 43 percent of projects go over their initial budget.

- 48 percent of programs are not delivered on time.

- 50 percent of senior executives believe corporate effectiveness is constrained by a lack of delivery effectiveness in transformation programs.

Many senior executives recognize the need for highly skilled project managers. According to PMI’s 2018 Pulse of the Profession report, more than two-thirds of project professionals say their senior leadership highly values project management, and nearly half of organizations prioritize developing a culture that values project management.3

But project management is easier said than done. Many actuaries feel overwhelmed because often they are asked to do it on top of their normal activities—and without proper project management training.

The Need for Project Management

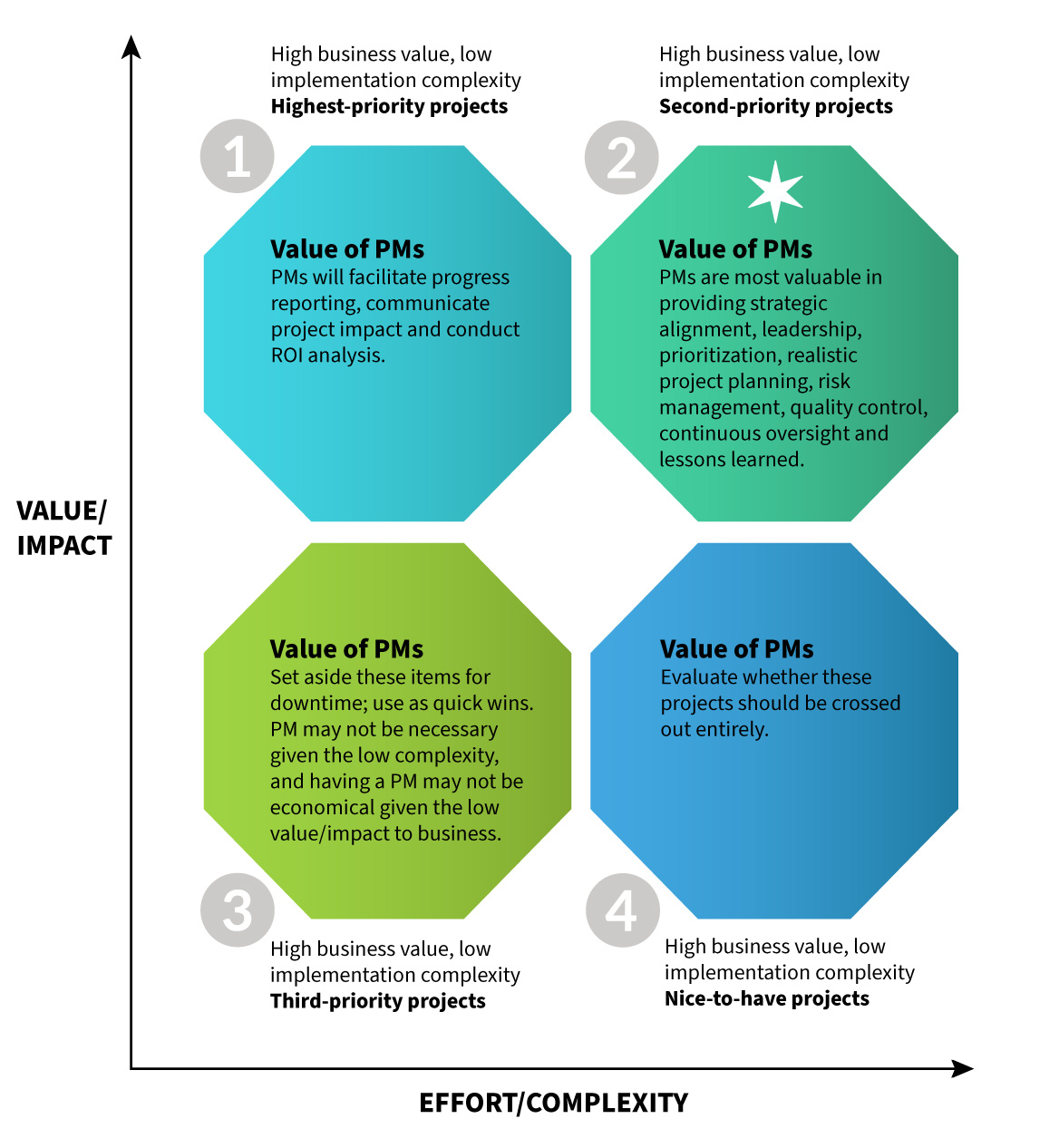

A “value vs. complexity” model frequently is used to prioritize initiatives and categorize projects into four types. This model highlights the value of a project manager and their contribution to the various scenarios. See Figure 1.

Figure 1: Value of Project Managers

For low-complexity or low-impact projects like scenarios 1, 3 and 4 in Figure 1, project manager support is still valuable—although the level of support can be scaled back to match the size and the budget of the project. Projects like scenario 2 (upper right corner of Figure 1) are the most complex, have the highest impact and span multiple business units and functional areas. Project manager support is most beneficial and critical for these types of projects.

A full suite of project manager capabilities is applicable in scenario 2—from strategic alignment, leadership, oversight and risk management at the top, to project execution, dependency management and quality control at the bottom. The project manager role is like a conductor of the orchestra. Despite each member being highly talented individually, a conductor is necessary so the music is played in harmony and all instruments complement one another throughout the musical movement.

Program vs. Project

A program is a group of related projects managed in a coordinated way, while a project is a single, temporary endeavor that ends when the work is completed and delivered. A large program typically consists of many projects. For example, a company may form an LDTI program to address accounting change requirements. Within the program, there could be actuarial modeling projects, data quality enhancement projects, reporting optimization projects and so forth.

As one author said: “Program managers are part of the organization’s senior management team focused on the strategic delivery of value. Project managers manage technicians and subcontractors. Program managers manage project managers and collaborate with other senior managers.”4

Program Management and Its Core Capabilities

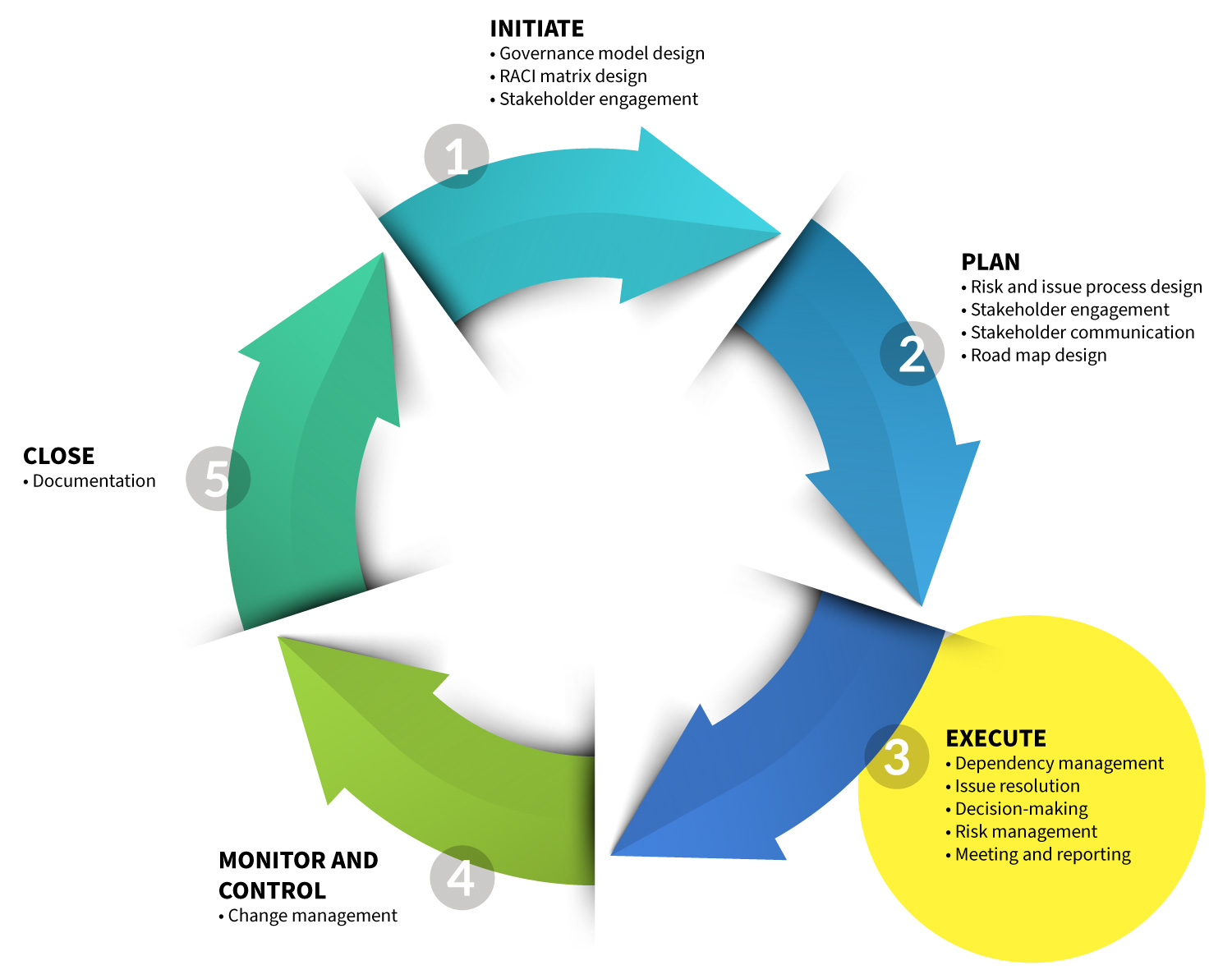

A typical project cycle goes from Initiate → Plan → Execute → Monitor and Control → Close.5 Figure 2 categorizes some key project manager capabilities/activities under each phase of the project cycle.

Figure 2: Five Phases of the Project Cycle

Let’s dive into four core project management capabilities during the project execution phase.

1. Dependency Management

Large, complex projects typically involve numerous project teams, multiple functional areas and several external vendors. Among possibly thousands of activities, certain ones are more critical to the success of the program. The critical path method (CPM) is a popular project management technique to identify these high-value, critical activities. These activities not only impact the individual project team’s delivery timeline, but they also have a day-to-day impact on the overall program’s timeline. When a potential delay of such activities is identified, project managers can manage these activities effectively and communicate the downstream impact to project teams.

Agile project management has gained popularity in the last decade. Most organizations nowadays adopt a hybrid project management approach that combines the agile method along with the traditional waterfall method. Under this approach, critical path activities may change from time to time. Project managers can provide guidance to each project team on the changing priorities, communicate program-level decisions and adjust project plans—while the project team stays focused on executing daily activities.

Here’s a simple example: An insurance company is conducting a model conversion project to produce PBR results. Supposedly, the assumptions are set by project team A and then will be implemented by project team B. Without the assumptions provided by project team A, project team B either cannot start or will be severely limited in starting its modeling activities. In this example, assumption setting is identified as a critical path activity. The delay from project team A has a downstream impact to prevent project team B from commencing its work, subsequently delaying the whole program. An effective project manager would highlight and prioritize the assumption-setting activity for project team A among all of its project-related activities.

2. Issue Resolution

Large, complex projects require a systematic approach to manage issue escalation and resolution, particularly on issues that impact critical-path activities. In a large transformation program, resources (e.g., labor, tools, budget) are allocated at the program level.

Project teams may run into issues they cannot solve due to lack of resources or authority. These issues might be resolved by pulling the levers available at the program level, such as adding full-time employees to address capacity constraints or using more advanced software and hardware. Project managers can escalate issues from each project team to the program level, where these issues are analyzed and prioritized according to their importance to the program. Program-level resources then can be deployed to accelerate issue resolution.

3. Decision-making

Decision-making is an integral part of project management. “The first rule for making good decisions is to involve the right people at the right level of the organization.”6 When there is no obvious decision-maker to provide guidance, project managers can escalate the issue to the program-level leadership.

For example, a new product was priced using system A. However, during the development phase, the project team identified numerous constraints of system A and found that system B was more suitable as the valuation tool. The project team lead does not have the authority to make the decision to switch the product from system A to system B due to cost implications as well as company policy considerations. The best course of action in this case is to escalate the issue to the program level and allow multiple business stakeholders to make a joint decision.

On the other hand, there may be situations where there are too many cooks in the kitchen, so to speak. Large programs usually consist of many stakeholders across various business units and functional areas. There is no surprise that each stakeholder may have different views that lead to a different decision on the same matter. Multiple stakeholders making conflicting decisions would cause confusion for project teams. In such cases, project managers can facilitate committee decisions at the program level so all stakeholders’ perspectives are considered and the final decision is made to benefit the entire program.

4. Risk Management

Risk needs to be managed at both the project team level as well as the program level to confirm that projects:

- Stay on time.

- Stay on budget.

- Are delivered with quality.

Underestimating risks could have severe consequences.

- Project timeline. Regulatory changes that have mandatory effective dates drive many actuarial transformation programs. Failure to comply with new requirements on time will not only damage the firm’s reputation but also result in costly fines. Project managers can manage project teams to complete tasks on time or communicate early warning signs when they see the program at risk.

- Budget management. Programs for developing innovative solutions may not always have a defined scope upfront. As more information becomes available, program leadership needs to make trade-offs to keep projects under budget. Project managers can communicate program-level changes and align the focus areas of individual project teams.

- Quality and controls. Regulatory or accounting changes require rigorous change control and documentation along the way. Actuaries excel at complicated coding and model calculations—while sometimes lacking in producing documentation. Project managers can provide administrative support on control and documentation requirements. Moreover, project managers can help enforce a standardized process and drive consistency across all project teams.

Collaboration With Project Managers

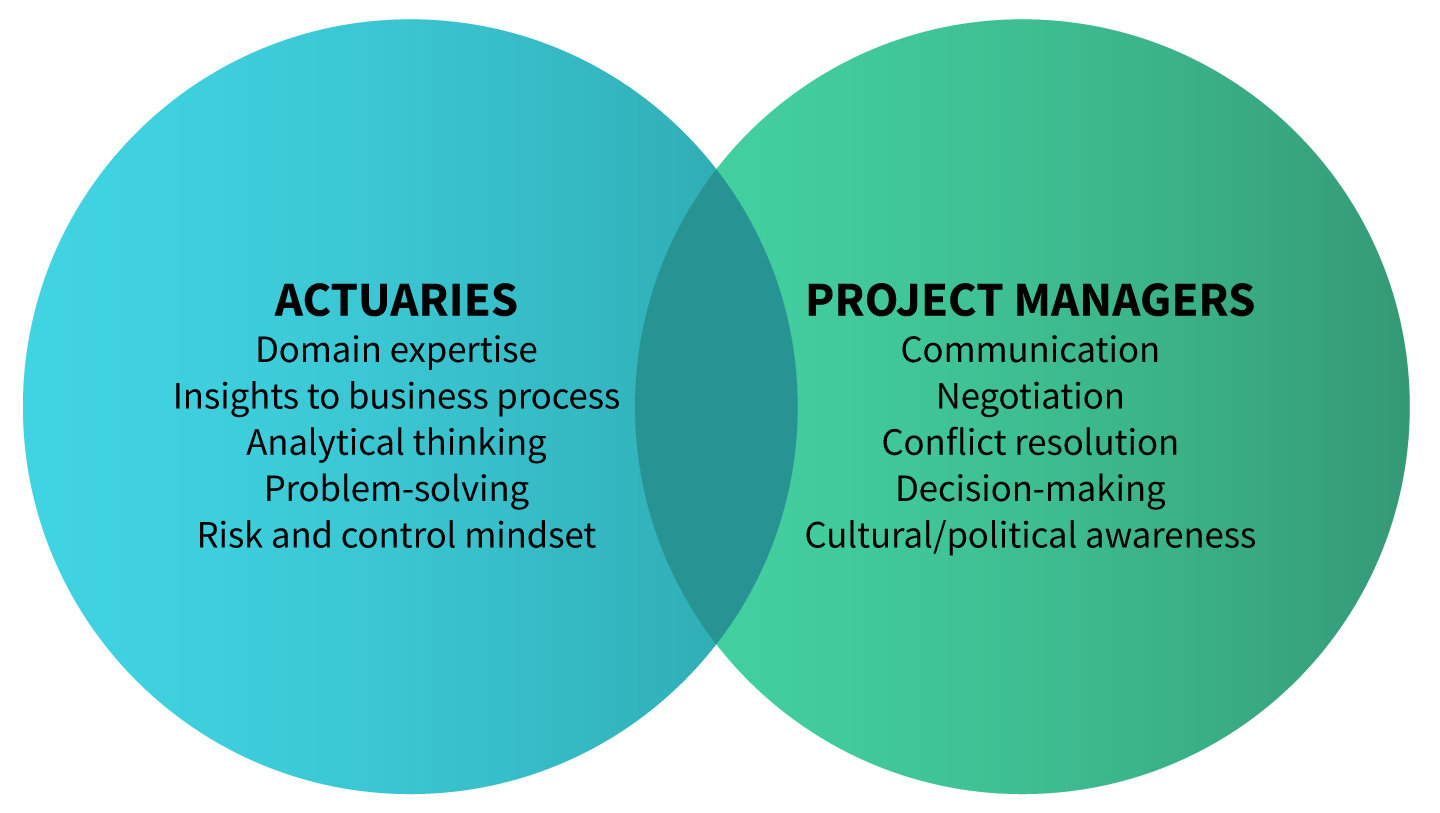

Recognition and appreciation for the value of project management is the first step for a successful collaboration between actuaries and project managers. Good project managers possess many skills that are complementary to actuaries. While actuaries bring domain expertise, technical insights and an analytical mindset, project managers leverage their skill set to bridge communication gaps, resolve conflicts, facilitate decision-making and manage program progress.

Figure 3: Complementary Skill Sets

Actuaries who play different roles in a transformation program could benefit from project management in different ways. Project managers work side by side with actuaries to assist or complement their activities.

Program Sponsors

Successful transformation programs require a clear vision and strategy. As program sponsors, actuaries at the executive level are asked to set the direction for the transformation programs based on the understanding of an organization’s business capabilities, operating model and workforce needs. At the top, project managers can facilitate decisions in defining the program strategy, creating a road map and building the business case to implement new capabilities (see Figure 4).

Figure 4: Project Responsibilities: Program Sponsors vs. Project Managers

| Program Sponsors | Project Managers |

|

|

Program Leaders

Establishing an effective governance model is pivotal for a successful program launch. A measurable and actionable reporting framework, with a view into short- and long-term success, will help drive adoption and attain program goals. Project managers can bring playbooks, resourcing models and analytics to help program leaders design and establish effective governance structures (see Figure 5).

Figure 5: Project Responsibilities: Program Leaders vs. Project Managers

| Program Leaders | Project Managers |

|

|

Project Teams

Project teams are the ultimate executors who deliver and achieve program goals. They need project management support to align project timelines with key milestone dates, balance resource availability and financial constraints, and react to change management needs (see Figure 6).

Figure 6: Project Responsibilities: Project Teams vs. Project Managers

| Project Teams | Project Managers |

|

|

Conclusion

Diligent program management ultimately can determine the realization of project goals. Most actuaries are not equipped with the skills to perform project management duties in addition to their project execution responsibilities. Project managers have become an integral part of the transformation teams.

Recognition and appreciation for the value of project management will help actuaries collaborate with project managers more effectively. Actuaries should embrace the different skill set and perspectives project managers bring to the project and be proactive in teaming up with and cross-training project managers. Doing so will not only help the success of ongoing projects, it also will help actuaries grow into the business leaders needed during this time of challenge, transformation and innovation for the insurance industry.

The views reflected in this article are those of the authors and do not necessarily reflect the views of Ernst & Young LLP or other members of the global EY organization. The material has been prepared for general information purposes only and is not intended to be relied upon as accounting, tax or other professional advice. Please refer to your advisers for specific advice.

References:

- 1. Project Management Institute. Ahead of the Curve: Forging a Future-Focused Culture. In Pulse of the Profession, February 11, 2020. ↩

- 2. Project Management Institute. $1 Million Wasted Every 20 Seconds by Organizations Around the World. Project Management Institute, February 15, 2018. ↩

- 3. Supra note 1. ↩

- 4. Weaver, P. 2010. Understanding Programs and Projects—Oh, There’s a Difference! Paper presented at PMI Global Congress 2010—Asia Pacific, Melbourne, Victoria, Australia. Newtown Square, Pennsylvania: Project Management Institute. ↩

- 5. Alie, S. 2015. Project Governance: #1 Critical Success Factor. Paper presented at PMI Global Congress 2015—North America, Orlando, FL. Newtown Square, Pennsylvania: Project Management Institute. ↩

- 6. Rogers, Paul, and Marcia W. Blenko. Who Has the D?: How Clear Decision Roles Enhance Organizational Performance. Harvard Business Review, January 2006. ↩

Copyright © 2020 by the Society of Actuaries, Chicago, Illinois.