Accelerated Underwriting Analysis

Examining today’s accelerated underwriting and its future potential

January 2024Photo: iStock.com/peshkov

As mentioned in the Society of Actuaries (SOA) 2022 Accelerated Underwriting Practices Survey Report, “accelerated underwriting (AU) programs give life insurers new ways of assessing medical and financial risks for some applicants more quickly than traditional underwriting programs.” New analysis of Reinsurance Group of America, Inc. (RGA) data on the state of AU for individual life insurance paints a clear picture of where AU is today and highlights a path forward for successful AU.

The SOA Research Institute’s 2022 Accelerated Underwriting Practices Survey Report compared the results of two surveys—not only to determine how practices have changed but also how they have changed from 2020 to 2022 because of COVID-19. The study identified these top five changes to AU programs from 2020 to 2022 (see pages 4-5 of the report for more details).

- Face amount limits: Seventeen of 22 respondents indicated changing face amount. Eight respondents made the change because of COVID-19, and 12 indicated the change was less restrictive, that is, an increase in face amount levels.

- Algorithm: Nine respondents changed their AU algorithm, with six respondents making a modification to the algorithm and four indicating the change was less restrictive.

- Data sources: Nine respondents changed their data sources, with seven of these respondents indicating the change was a new data source. Responses were split between whether the change was more or less restrictive.

- Issue age limits: Seven respondents changed their issue age limits.

- Random holdouts: Seven respondents changed their random holdout practice.

Gathered from RGA data and confidential industry sources, the analysis looked at acceleration rates, mortality slippage based on gender and risk class, and the type of evidence and tools the industry currently uses for AU programs. It also addresses concerns from the AU community about escalating policy face values and issue ages. (The SOA Research Institute published a report in November 2023. See the sidebar for more details and key takeaways.)

Where Are We Now?

AU programs have matured and strengthened since 2014, which generally is considered the year the practice started to develop. RGA’s analysis of the U.S. individual life insurance AU market demonstrates that maturity and may offer guidance on enhancing existing AU programs and improving their outcomes.

Acceleration Rate

Across the AU programs RGA reinsures, acceleration rates vary from 10%-70%, with an average acceleration rate of 40%-50%.

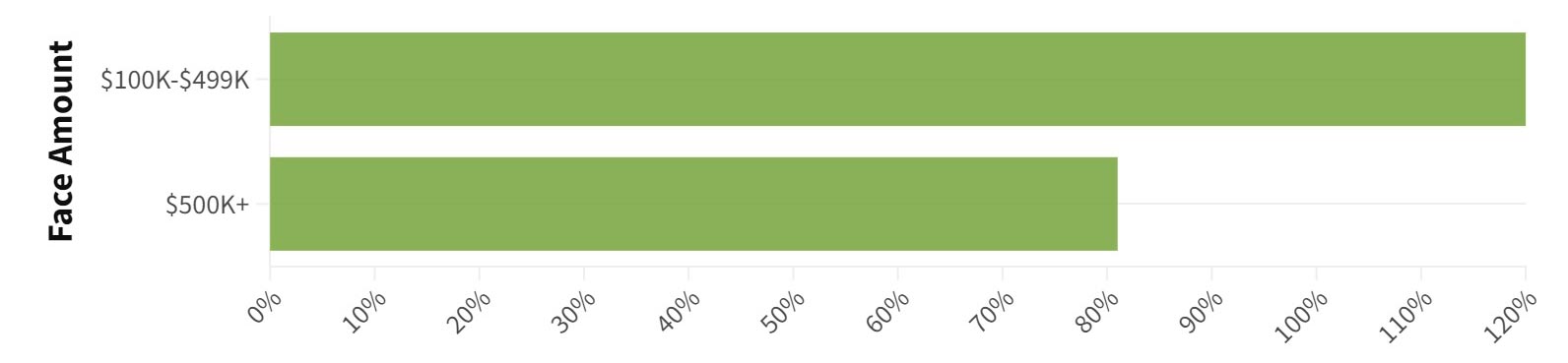

Mortality slippage—the estimated mortality increase for policies issued through AU relative to policies issued through traditional underwriting—also may change as face amounts increase. Recent analysis of AU random holdout data reveals lower mortality slippage for face amounts $500,000 and higher when compared to smaller face amounts, as shown in Figure 1.

Figure 1: Average Mortality Slippage by Policy Face Amount, Relative to Total, for AU Life Policies

Source: RGA, based on random holdout data 2020–Q1 2023

Maximum Face Amount

The most common maximum face amount is $1 million, with more than 40% of AU programs setting that as the maximum. Another 40% of AU programs maintain a maximum face amount of $2 million to $3 million. Almost half the programs offering $2 million or more in coverage use tiered age limits to ensure the highest face amounts are restricted to younger issue ages, such as age 40 or 50. Less than 5% of AU programs offer maximum face amounts of more than $3 million.

In general, acceleration rates for policies up to $1 million are higher than acceleration rates for policies greater than $1 million.

Issue Age

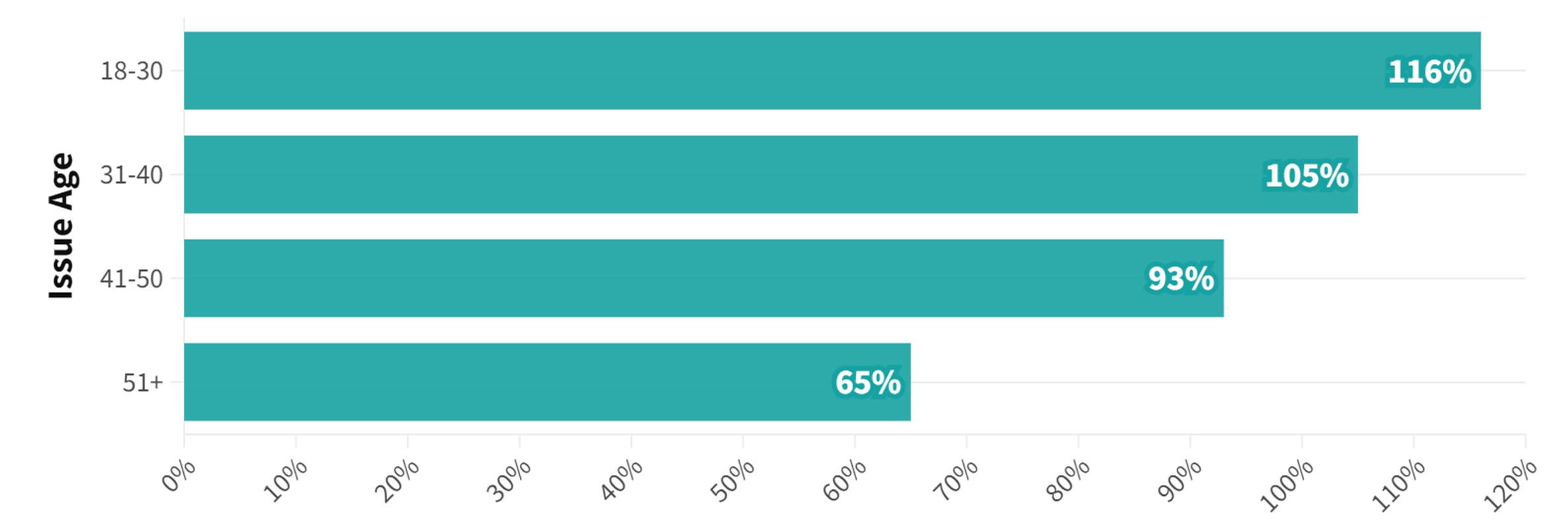

Currently, the most common maximum issue age is 60. Only a few AU programs push their maximum issue age to 65 years. Medical impairments are more common at higher ages, which may correlate to lower acceleration rates and higher mortality slippage for policies issued to older applicants. As shown in Figure 2, older applicants are less likely to be approved by accelerated means than younger applicants.

Figure 2: Average Acceleration Rate by Issue Age, Relative to Total, for AU Life Policies

Source: RGA data for policies issued 2020–Q1 2023

As one might expect, AU random holdout data reveals the highest mortality slippage for ages 40 and older. Interestingly, however, we see higher mortality slippage for ages 18-30 than the 31-40 age group. One theory is that people under 30 may visit their doctors less frequently than their older counterparts, and less detailed digital medical footprints may allow higher-risk, younger applicants who otherwise would have been disqualified from the accelerated process to be approved.

Gender

AU random holdout data reveals a material gender gap for estimated mortality slippage on AU policies. On average, the mortality slippage of females is 40% lower than the overall average for an AU program; the rate for males is 40% higher.

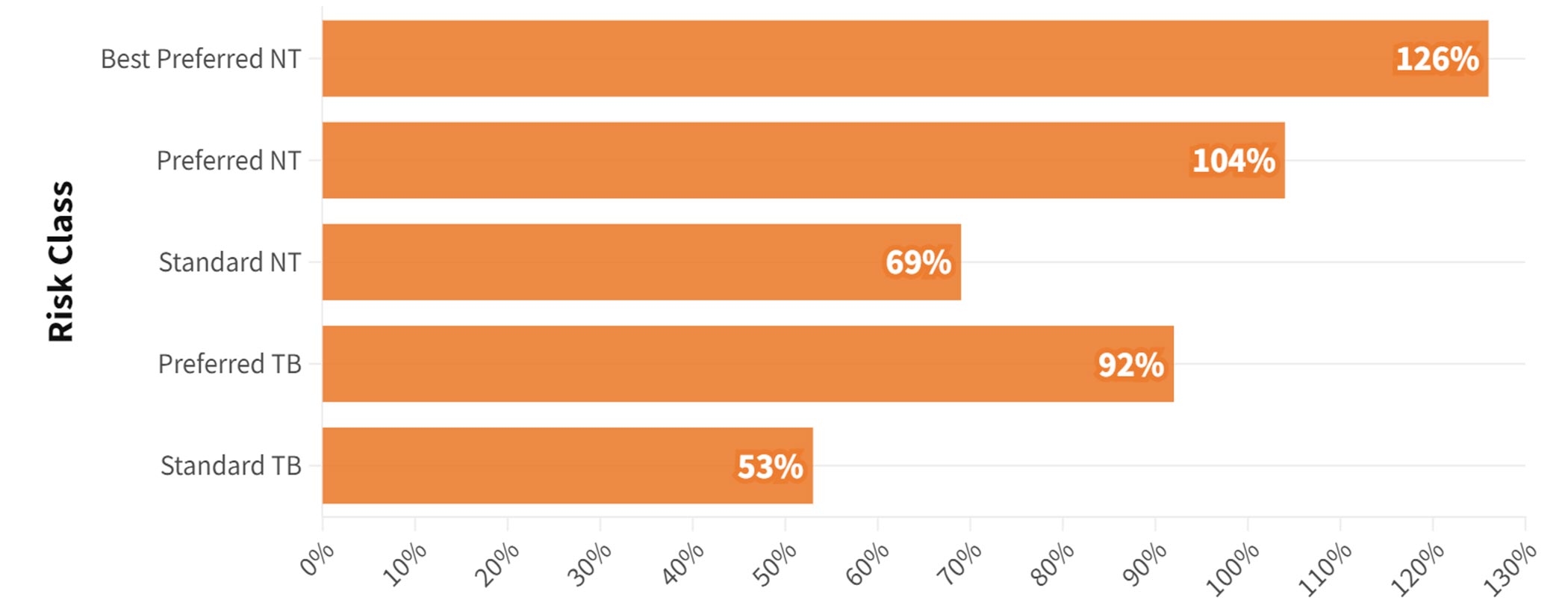

Risk Classes

Early AU programs restricted offerings to preferred nontobacco user classes. But as the industry learned from its early iterations, AU programs have expanded to standard and better classes, both tobacco and nontobacco. Some programs are adding substandard classes to the mix, but they typically structure them as grouped substandard classes. In an accelerated environment where full details about the applicant’s health profile may not be available, it can be difficult to determine a precise table rating.

The best risk class has the highest acceleration rate and the highest mortality slippage. On average, this class’s acceleration rate is between 1.5 and 2 times that of the residual standard class, as shown in Figure 3. Based on AU random holdout data, the best risk class has more than 1.5 times the overall mortality slippage, on average. This is partly due to the absence of key metrics in traditional preferred criteria, such as measured cholesterol, blood pressure and body composition. Additionally, while other risk classes may benefit from “favorable misclassifications” in some programs, this isn’t possible for the best class because there are no better classes “upstream.”

Figure 3: Average Acceleration Rate by Risk Class, Relative to Total, for AU Life Policies

NT = Nontobacco

TB = Tobacco

Source: RGA data for policies issued 2020–Q1 2023

Evidence and Tools

Without the traditional paramedical exam and fluids collection that takes place under full underwriting, AU frequently necessitates additional evidence to evaluate applicants. Figure 4 breaks down the types of evidence and tools AU programs use most frequently, as well as tools that underwriters are exploring for expanded use in the future.

Figure 4: Use of Evidence and Tools in AU

| Nearly Universal | Common, Not Universal | In Progress or Upcoming |

| Prescription history | Credit data (most common) | Electronic health records |

| Motor vehicle record (MVR) | Clinical labs | Medical record summarization |

| Medical Information Bureau (MIB) | Medical claims | |

| ID verification | Combination scores (created by combining two or more data sources, i.e., medical data and credit data) |

Source: RGA, 2023

Many insurers have zeroed in on the “big three” evidence types to enhance their AU programs:

- Clinical labs: With a strong “hit rate” (the rate that an inquiry returns information on an applicant) of 60%-70%, clinical labs provide deep information on specific test results. However, they provide little context about why a physician ordered a lab or the applicant’s overall health picture.

- Medical claims: The reverse is true for medical claims, which provide a broader look at an applicant’s health, potential impairments and past diagnoses—but will not include test results. Hit rates vary by vendor but can top 80%, providing a solid opportunity to gather health data on an applicant.

- Electronic health records: While they offer the weakest hit rate at 30%-40%, electronic health records can paint the clearest picture of an applicant’s medical history, including treatment plans, lab results and doctors’ notes. Yet the unstructured nature of this data makes it challenging to automate.

Choosing between evidence tools requires more than a one-size-fits-all approach. It is important for insurers to seek the best type of evidence to make a decision on a specific case. What is right for one case may not work for another. But each of these “big three” evidence types carries the strong advantage of being significantly less expensive and time-consuming than a paramedical exam or insurance lab panel.

Next Steps

What can this new analysis tell us about how to potentially improve AU programs?

- Take a breath—insurers are achieving equilibrium on face values and issue age. Industry chatter about escalating face values and issue ages had many insurers worried about keeping pace. Recent data shows that few insurers are pushing past $3 million or offering coverage to applicants over 60.

- The AU gender gap is real but manageable. The +/-40% mortality slippage variation between women and men relative to an overall program is significant and could create challenges for insurers that have not factored those differences into their pricing. If not priced appropriately, insurers could lose money on male cohorts, particularly for products with thinner margins. As with any life insurance product, insurers can mitigate the effect of the gender gap with careful pricing and an understanding of any gender distribution risk on accelerated policies.

- Build a feedback loop, and act on the findings. Insurers are pressured to increase their acceleration rates, which tends to result in higher mortality slippage. In our view, one of the best ways to break that correlation is to analyze misclassified AU cases and determine which of the “big three” evidence types could have revealed the information needed to address problematic cases. We believe this type of forensic auditing may help insurers better align applicants and evidence and ultimately make better AU decisions. It also may pave the way for alternative pathways if a case does not immediately qualify for AU. With the right information about similar cases, insurers can request clinical labs or medical claims, providing an AU pathway that avoids fluid collection or needle sticks.

Conclusion

The future is bright for AU programs, and this new analysis highlights opportunities for program improvements, whether through a closer investigation of mortality slippage by gender, expanded use of evidence or a stronger emphasis on monitoring. We believe insurers could expand AU offerings and improve overall outcomes by focusing on these factors.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

Copyright © 2023 by the Society of Actuaries, Chicago, Illinois.