Extra Coverage Necessário

A regulatory impact assessment on Brazilian individual health plans

October/November 2016The Brazilian Constitution states, “Health is a right of all and the duty of the State.” Thus, in order to meet the demands of the more than 200 million people in the country, the Brazilian government established a program called Sistema Único de Saúde (SUS) more than 25 years ago.

To operate this program, the State has set up a network of public, philanthropic, and private hospitals and clinics. In this system, the pay grade table SUS offers to its partners has a gap of up to 1,300 percent1 when compared to the pay grade table of the market. Not only does this pay gap weaken the established partnerships among hospitals and clinics, but it also discourages new entrants into the system, which has led to a shortage of medical staff and patient beds.

For these reasons, the SUS has been unable to satisfy the tremendous demand for medical procedures, resulting in 25 percent2 of the Brazilian population acquiring some kind of supplementary health plan, i.e., a plan that is a substitute for public health. Components of this system include the regulatory agency Agência Nacional de Saúde Suplementar (ANS), companies that sell supplementary health products (health insurance and health plan companies), and members and providers (physicians, hospitals, laboratories, etc.).

Supplementary health products have existed in Brazil since the 1960s. However, delays in the formation of operational regulations caused the majority of health plans selling these products to operate without any consumer guarantee until 1998, when the first regulations came about. Since then, ANS has published more than 500 new rules, with the goal of making the market more professional and safer for the consumer.

Due to the new legislation, Brazilian supplementary health products no longer were permitted to establish limits of any kind—quantitative or financial—and ANS monitored all of the companies selling these supplemental products very closely to ensure cooperation. In addition, these companies were required to begin setting up certain reserves.

Forcing all of the companies that sell supplementary health products to conform to these rules caused severe decapitalization of the sector. Strong measures to compensate this decapitalization were taken. In the case of individual products, these regulations caused a massive extinction; although these products were never the priority of these companies, they have dropped to the lowest market share since September 2005, at just 20 percent. Companies selling supplementary health plans are finding many difficulties in this line of business, which unlike the group health plans, is strongly regulated and monitored by ANS.

With respect to individual plans specifically, many legislative points must be assessed as factors that discourage their continuity in the market. Consider the following examples:

- The prohibition of the insurer’s ability to terminate the contracts, which makes the products valid for an indefinite period (i.e., lifelong).

- The regulation of the annual rate increases is based on group plan experience.

- The prohibition of risk selection or underwriting on the basis of age or preexisting conditions at the time of enrollment.

- Frequent updates in the list of mandatory medical procedures that must be covered, which extends to all contracts established since 1999 that do not have a counterpart to the price reevaluation.

Moreover, these practices work poorly for the market because they do not always employ the basics of good actuarial practice. These plans often are considered to be a true market destabilizer, similar to what happened to the Brazilian individual life insurance market in the past, in which a similar model damaged many insurance companies financially.

ACRONYMS LIST

| Acronym | Definition |

| AcANS | Accumulated ANS rates |

| AcIPCA | Accumulated IPCA rates |

| AcVCMH | Accumulated VCMH rates |

| ANS | Regulatory Health Agency |

| IBGE | Brazilian Institute of Geography and Statistics |

| IESS | Supplementary Health Research Institute |

| IPCA | Brazilian Inflation |

| PDR | Premium Deficiency Reserve |

| SUS | Brazilian Government health program |

| VCMH | Brazilian Medical Trend |

For all of these reasons, the analysis of ANS data for individual plans indicates that the loss ratio of these products has increased steeply over the years. From here forward, we will examine some of the legal issues that affect the loss ratio for these supplemental products.

Variation of Medical and/or Hospital Costs (Variação de Custos Médicos e Hospitalares)

The ANS has imposed rate increase restrictions on the individual market. For several years, the rate increase regulations—although higher than the Consumer Price Index (called IPCA or Brazilian Inflation)—did not increase fast enough to keep up with the Variação de Custos Médicos e Hospitalares (VCMH or Brazilian Medical Trend).

Figure 1 is a comparison chart showing the percentage rates of VCMH, IPCA and ANS adjustment, as well as their accumulation (AcVCMH, AcIPCA and AcANS) over the years.

Figure 1: Rates of Brazilian Supplementary Health Index (VCMH, IPCA and ANS)

Source: Based on data from VCMH, IPCA and ANS readjustment data history

It should be noted that during a period of only nine years, if the VCMH is compared to the mandatory rate by the ANS, individual plans lost 50 percent of their value, which had a direct impact on the increased loss ratio.

Demographic Aging

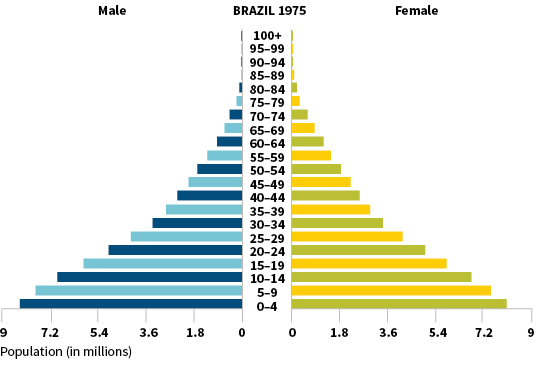

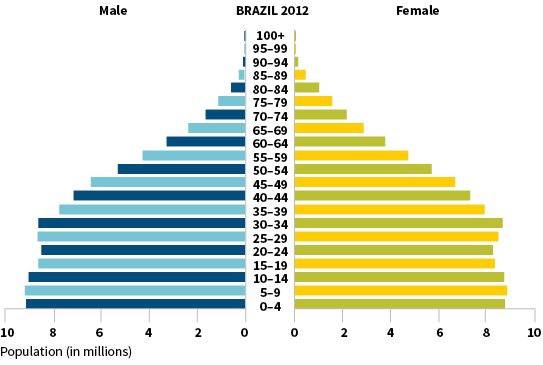

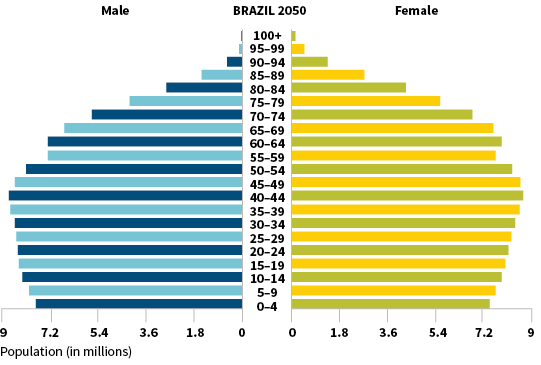

In the last 30 years, Brazil has experienced a strong demographic transformation. Data from the Brazilian Institute of Geography and Statistics (IBGE) indicates that in a maximum of 40 years, the Brazilian age pyramid will be older (similar to that of France at present). In other words, we expect a quick shift in the ages of our population, as can be seen in Figure 2.

Figure 2: Age Pyramid of the Brazilian Population Through the Years

Source: Brazilian Institute of Geography and Statistics

Aging, by itself, could be considered a big problem Brazilian health plan companies will need to face. However, the application of existing Brazilian rules will only exacerbate the issue.

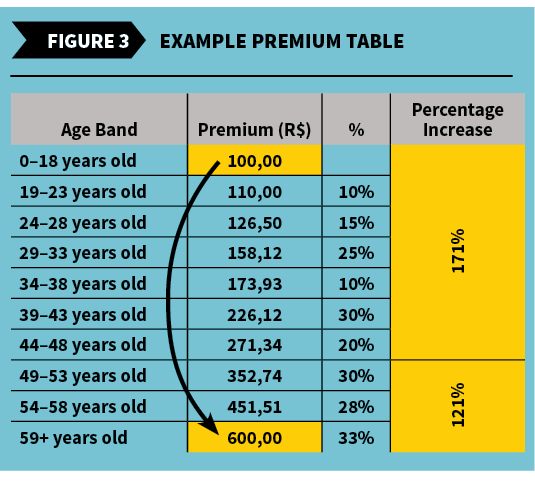

According to the ANS regulations, health plans have limitations on how much the premiums are allowed to vary or increase by age within the 10 required age bands. Specifically, those companies must make sure the oldest age band’s premium level does not exceed six times the first age band’s premium, and that the percentage increase between the premiums of the seventh and the 10th age bands does not exceed the percentage increase between the first and the seventh age bands’ premiums.

Consider Figure 3 for an example of these limitations:

If we take a careful look at Milliman’s Brazil Health Cost Guidelines, we can verify the difference in cost between the first and the last age band is much more than six times, which is inconsistent with the ANS guidelines. To fill this gap, health plan companies had to charge more to their younger enrollees in order to reach greater values in the higher ranges.

List of Procedures

In order to follow the technological developments in medicine, every two years the ANS determines a new list of appointments, exams and treatments with mandatory coverage in health plans. Since 1998, this list has represented the minimum coverage required for consumers according to the coverage of the signed contract (out-patient, inpatient or both).

It would be most actuarially appropriate if companies that sell supplementary health products could pass the extra cost to consumers. However, as seen earlier, the allowable increases are regulated by the ANS and have never been set high enough to cover costs of the new procedures.

Technical Reserves Deficiency

ANS requires that these health plan companies set up only the incurred but not reported reserve, the unearned premium reserve, and the due and unpaid reserve; however, individual plans require more reserves than just these in order to stabilize the loss ratio over time. These include the contract reserve, the active life reserve and the premium deficiency reserve (PDR).

The contract reserve is established when some portion of the premium collected in a contract’s early stages is intentionally designated to help pay for anticipated higher claims costs in later stages, like in Brazil contracts.

The active life reserve is the combination of contract reserves and unearned premium reserves; the latter already is mandatory in Brazil and represents premiums that have been collected and entered in the ledger, but actually are allocated to a period of time after the valuation date.

The PDR is set up when it is determined that future premiums are not sufficient to cover future claims payments and expenses. The distinction between the PDR and the contract reserve lies in the initial pricing intent. Contract reserves are established when the product is priced initially, with the knowledge that the incidence of premiums and claims will not match. A PDR is required when a gross premium valuation determines there is a contractual obligation to fund future losses, but the liability cannot be recognized by an experience adjustment to contract reserve entries because it has already been sold, leaving you in a bind.

Joining all of the rules together, we can create a simulation for an individual plan and its evolution through the years. We will assume an expected initial loss ratio of 70 percent for a 30-year-old, a claim cost increase of 1.5 percent for each additional year of age (e.g., a 31-year-old costs 1.5 percent more than a 30-year-old), and a readjustment gap of 4 percent per year (taking into account the list of new procedures every two years). The readjustment gap is essentially the difference between the real increase in costs (e.g., 10 percent), and what ANS will allow these premiums to increase by (e.g., 6 percent), which results in a gap between the real cost and the premium level (e.g., a readjustment gap of 4 percent).

Observing Figure 4, it is clear the detachment of the premium curve and the events curve begins at age 62, but the loss ratio already has reached alarming levels by age 38.

Figure 4: Sample Individual Plan Evolution By Age

Source: Author’s own elaboration

To meet the financial needs wrought by these regulations, the health plan companies set the premium payment of the products so new entrants partially subsidize the older ones, which changes the underlying premium model to use cross-subsidization and premiums that do not align with costs.

Undercapitalized and discouraged, as well as lacking the needed reserves, the insurance companies in this market gradually are moving toward a more practical solution: stop selling individual plans in order to limit the damage generated by this portfolio. Because of this approach, many of the individual plan portfolios of health insurance companies are in decline.

In addition to these adverse conditions, which have been in place since 2005, the situation is getting worse today as Brazil experiences serious economic problems. With the collapse of the economy, unemployment rates consistently have set new records every month. Because these people have no backup plan, the government tries to remediate part of the problem by mandating that all employers keep their dismissed and retired employees in the portfolio for some time, since the employees help pay for the cost. However, this practice is tied directly to the increase in post-employment liabilities (International Accounting Standards), which causes dissatisfaction with the employers, in turn producing a negative impact on the group health plans.

We conclude that for the market to regain interest in individual plans and to wholly rebalance itself, it would require radical changes in legislation, including the requirement of the aforementioned reserves.