Protecting Bradley

Life insurers can do a better job of making life insurance more relevant to millennials

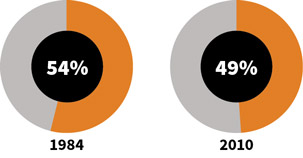

December 2015/January 2016Demand for mortality protection is closely tied to life cycle. At the early stages of adult life, the need for income protection rises as people finish their education, start a job, get married, buy a house and have children. In a few coming years, the millennials—those born between 1981 and the late 1990s—will be the segment with the largest need for mortality protection. Swiss Re’s research shows that in 2010, both the protection needs and the protection gap were the largest for families headed by 35- to 44-year-olds—the age group that will consist of the millennials over the next decade. Millennials today are still underserved, however, contributing $4.9 trillion of the $20 trillion protection gap as of 2010.1

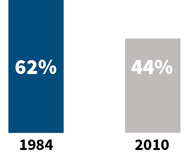

The mortality protection gap spans across both employer-provided (group) and individual coverage sources. Ownership of life insurance has declined at an alarming rate and currently stands at a 50-year low, according to a LIMRA study.

With a population of 85 million, millennials are the largest age cohort of the U.S. population with the highest share (35 percent) in the working age population (see Figure 1). Compared to earlier generations, millennials are better educated—especially women—and are more ethnically diverse. For example, approximately 61 percent of adult millennials have attended college, whereas only 46 percent of baby boomers did so.

Figure 1: Age Group Share of Working Age Population, 2013

They’re most open to change and are more connected. They are also “digital natives,” as technology has always been present in their lives. Thus, they’re the most avid users of the Internet and mobile devices, and most active on social media networks. Nearly a quarter of millennials say that their generation’s unique and distinctive identity is tied to their use of technology.4 As shown in Figure 2, millennials spent over 400 billion minutes on the Internet in 2014 alone, compared to Gen Xers, who recorded a little over 200 billion minutes of Internet usage.

Figure 2: Minutes on Internet (In Billions)

The economic characteristics of the millennial generation are also different, as they still carry the scars of the latest recession. The oldest millennials were in their late 20s during the economic recession, when unemployment levels kept rising with decreasing levels of income. Succeeding years of millennials faced a difficult employment market just as they were graduating from college. The average earnings of persons under age 35 relative to all families fell from 61 percent in 2007 to 56 percent in 2013, as they started their careers in a weak labor market with flat or lower average starting salaries, got modest raises and had higher rates of underemployment.5 This experience has greatly molded their financial and economic decision-making process.

Moreover, millennials are entering adulthood with record levels of student debt.6 For example, there was an approximate 70 percent increase in student loan borrowers from 2004 to 2012, and about 52 percent of millennials claim that student loans are their biggest financial concern (see Figure 3). In the event of the death of a millennial with student debt, the responsibility for that student’s loan transferring over can be unmanageable or financially devastating for the student’s co-signer.

Figure 3: Biggest Financial Concern for Millennials

A life insurance policy might be a good option to provide some peace of mind. Additionally, a good proportion of millennials are currently out of school and in the workforce, and hence liable for these debts.

Despite their personal debt, millennials are surprising long-term optimists, which explains their willingness to keep their money in tracking Exchange Traded Funds (ETFs).7; More than 8 in 10 say they either currently have enough money to lead the lives they want (32 percent) or expect to in the future (53 percent).8 This might be an avenue for life insurers to educate and market to millennials not only on the need for protection, but also for financial planning.

Reaching the millennials to help them address their protection needs is a huge opportunity for insurers. Life insurers need to understand the characteristics and expectations of this generation in order to successfully engage with them. The fact is that millennials have the most to gain—they’re most likely healthy and will qualify for lower premium rates for life insurance coverage when they apply early in life. As it stands today, millennials aren’t being reached in the right way—they’re digital natives, yet most life insurers are still using traditional broker and agent channels to reach their consumers.

Life insurers can do a better job of making life insurance relevant for millennials. This generation typically identifies with products that fit their lifestyles, and as the current industry stands, it’s difficult for them to understand the importance of life insurance protection. Technological developments, the spread of the Internet, and social media have strongly influenced consumer preferences and buying behavior, especially of millennials. They’ve grown to expect easy and quick access to information in their commercial interactions, transparency about cost and value, and high-services. They’re savvy in their buying practices, invest time to research and compare options online, and seek the fastest and easiest ways to make the most cost-effective purchases.9

Selling and buying life insurance is challenging for many reasons. In the current economic environment, many families still face budget constraints that limit demand due to stagnant or declining real income. Familiarity with life insurance and perceptions of need are also a hurdle. Unlike other types of insurance such as home and auto, the purchase of life insurance is discretionary, and as such doesn’t stack up high in the hierarchy of perceived needs.

According to LIMRA’s 2015 Insurance Barometer Study, many millennials place more importance on purchasing technology, eating out and shopping over buying life insurance. Millennials aren’t familiar with the insurance industry10 and don’t understand why life coverage is relevant in their lives. Only 5 percent say they’re very familiar with the concept of insurance (see Figure 4). Also important are powerful psychological and behavioral biases, which tend to hinder “rational” decision-making when it comes to making complex decisions such as the purchase of life insurance.11

Figure 4: Millennial Familiarity With The Insurance Industry

The life insurance industry has fallen behind many other industries in meeting customer expectations in the digital age. Much needs to be done to improve the customer experience and to make the buying of life insurance simple, convenient, non-invasive and pleasant. Life insurers need to simplify products where possible and streamline underwriting and selling procedures, making use of big data and predictive analytics tools to complement the protective value of the traditional underwriting process. Utilizing predictive modeling techniques to develop an analytics-based approach to underwriting can result in better, faster and more efficient business decision-making. It is clear that other industries—such as property and casualty and banking, among others—have taken the lead in incorporating predictive analytics as part of their core business processes to improve their decision-making.

PREDICTIVE ANALYTICS IN THE LIFE INSURANCE PROCESS

Predictive analytics is basically the analysis of large data sets (big data) to make inferences or identify meaningful relationships, and the use of these relationships to better predict future events. Predictive modeling tools have the potential to enable insurers to address some of the concerns resulting in the low penetration of life insurance among millennials—complex and invasive underwriting process, costly and time-consuming process from time of application to when a policy is issued, etc…

The gains from utilizing predictive analytics tools clearly include shortening turnaround times of the buying process; reducing the cost of underwriting and, ultimately, insurance premiums; and reducing the current invasiveness of underwriting. These are improvements from which both the insurer and every prospective policyholder will ultimately benefit, but even more so the millennial generation that has particularly identified these concerns as the pain points of its insurance buying experience.

Digital technology provides huge potential to transform the life industry and make it more consumer-centric. Technology now allows for end-to-end contact between insurers and customers on mobile platforms, especially for the relatively simple and standardized products that younger adults need the most. The spread of wearable devices has opened opportunities to engage consumers and build long-term relationships by motivating and rewarding healthy behaviors. Data collected in real time will become increasingly relevant in risk measurement and assessment, and may radically transform underwriting. Advances in big data and cognitive computing promise to lead to the development of new tools for digital advice and personalized product and coverage recommendations.

Distribution Capabilities

Distribution channels have been evolving over time with new technology and the Internet. Companies must adapt their distribution strategies quickly and take advantage of new technologies that allow for speedy and interactive ways to engage consumers online and via mobile, communicate more effectively and foster long-term relationships with their customers.

A good example is MetLife expanding into traditional brick-and-mortar stores (Wal-Mart) to sell life insurance from a kiosk. Even large technology and retail companies like Google and Amazon are partnering with insurers as retailers. Distribution has become a source of competitive advantage for life insurers. This process will create value for consumers of all ages, but it is especially vital for reaching the younger generations for whom the traditional methods of risk assessment, underwriting and selling life insurance products are an enigma.

Although innovation is already underway, it is still in an emerging stage. For example, John Hancock and the Vitality Group partnered recently to create an interactive wellness program whereby wearing a Fitbit and sending information seamlessly to their insurer, participants can earn rewards throughout the year by reaching their wellness goals. They’ve made healthy living a part of life insurance. This model of wellness and life insurance has been in place in other markets, particularly in South Africa where the Vitality Group has a partnership with Discovery Insurance to provide rewards and incentives to its policyholders.

Mass Mutual established Haven Life, an insurance agency that enables customers to apply for and receive term life insurance entirely online. Oscar Life, a health insurer, has created an app that compiles a comprehensive history of an individual’s health, including doctor’s visits and prescriptions, as well as providing fitness trackers for its patrons. These are all examples of how investing in technology is key to reaching younger consumers. The opportunities to build long-lasting relationships from early adulthood are huge for companies that successfully adapt their business models to engage them.

Conclusion

Market trends show that life insurance coverage continued to decline from 2010 to 2013. Over the next 10 years, the millennials will be 35- to 44-year-olds—spanning the time in adult life during which mortality protection needs are the highest and the protection gap has historically been largest.

The preferences and expectations of this large demographic group will define the future of the industry. Their behaviors have been shaped by use of technology from a very early age, and in order to reach and engage with them, life insurers need to radically transform traditional practices and carry out efforts to make life insurance more relevant. Technology will inevitably play a key role, and early adopters will have a significant competitive advantage.

The advent of more advanced technology—cognitive computing, big data and predictive analytics—is transforming the insurance industry. Life insurers need to embrace the use of predictive analytics in their business decision-making process, given that it has the ability to help shorten turnaround times, reduce the cost of underwriting and reduce the current invasiveness of underwriting.

References:

- 1. Swiss Re, sigma, The mortality protection gap, August 2012. ↩

- 2.LIMRA, Household trends in U.S. Life insurance ownership, 2010. ↩

- 3. LIMRA, 2015 Insurance Barometer study. ↩

- 4. Pew Research Center, How millennials today compare with their grandparents 50 years ago, pewrsr.ch/1x4rsjT. ↩

- 5. Swiss Re Economic Research and Consulting, The U.S. mortality protection gap—an update. ↩

- 6. Two-thirds of recent bachelor’s degree recipients have outstanding student loans, with an average debt of about $27,000. See How much do students really pay for college? Urban Institute, Dec. 5, 2013. ↩

- 7. Pew Research Center, Millennials in Adulthood ↩

- 8. The Stunning Evolution of Millennials: They’ve become the Ben Franklin Generation, huff.to/1Fa6eEx. ↩

- 9. Nielsen, Mobile Millennials: Over 85% of Generation Y owns smartphones, 2014, bit.ly/1pyhyfG; and Urban Land Institute Foundation, Generation Y: Shopping and entertainment in the digital age, 2013. ↩

- 10. The Griffith Insurance Education Foundation and The Institutes, Millennial generation attitudes toward work and the insurance industry, 2012. ↩

- 11. Swiss Re, sigma, Life insurance: focusing on the consumer, June 2013, offers a detailed discussion on why consumers don’t buy life insurance. ↩