Releasing Inspiration

A story of collaboration, innovation and saying good-bye to the fax machine!

October/November 2017I have a lot of love for the insurance world, having worked in a variety of roles in insurance for the past two decades. Though I love our industry, it has been notoriously slow to respond to technological innovations that improve the way things have always been done. The insurance industry is complex and intricate, fraught with poor user experiences, low literacy, lack of transparency and heated political challenges. It is also nearly 7 percent of the entire gross domestic product (GDP) in the United States.

Unfortunately, while the world rapidly adopts ever-changing technology and the use of automation for daily activities, the employee benefits industry is operating as it did 20 years ago in most places. The tools commonly used by insurance professionals remain unchanged—Microsoft Excel, paper applications, wet signatures and even fax machines! Recently, however, the sun has begun to rise on the insurance industry, and there are positive signs of change. These innovations are most obvious at the front end of health care, where health payment solutions, data analytics tools, telehealth, wearable devices, and other products and services are addressing the needs of businesses and consumers.

But equally important and powerful is what’s happening behind the scenes, in the health care system’s back-end infrastructure. This “unsexy plumbing,” as it has been called, makes the front-end advances possible. For technology innovators, this plumbing also presents myriad opportunities to reduce costs, streamline processes and shape the future of this industry that affects all Americans.

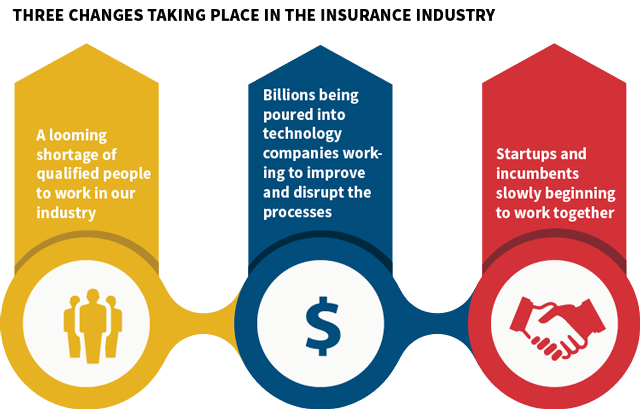

There are three sweeping changes taking place in the insurance industry:

- A looming shortage of qualified people to work in our industry

- Billions being poured into technology companies working to improve and disrupt the processes

- Startups and incumbents slowly beginning to work together

A Looming Shortage of Qualified Workers in Employee Benefits

Seasoned insurance agents are rapidly exiting the industry. According to McKinsey & Company research, one in four agents will retire by 2018, and the agency market is expected to have a serious shortage of agents.1

- The average age of a U.S. insurance agent is 60.

- Twenty-five percent of the industry’s workforce is expected to retire by 2018, with 35 percent projected to retire by 2020.

- Agencies need to hire three young producers for every producer currently employed.

This means we have a massive shortage of brokers—both e-brokers and traditional. Are you ready for this industry turnover? How will you scale to attract and retain the next generation of insurance professionals entering the workforce? How do we attract qualified talent and inspire a new generation to build their careers in this industry?

Now is the time for insurance businesses, brokers and carriers to find ways to attract and recruit new talent and, in the process, modernize their business workflow and integrate technology platforms and standards.

Money is Pouring Into the Insurance Sector

InsurTech investments between 2014 and 2016 alone generated more than $10 billion for startups. This does not include the additional investments made by mature and established insurance companies that updated or revamped their technologies. KPMG notes that it expects investment interest in InsurTech to remain “hot” throughout all areas of the world in 2017.2 InsurTech companies are working to solve the pain points within the industry, offering new data sources, providing new possibilities for underwriting, increasing customer focus and attempting to reduce costs substantially. These companies have the ability to transform the operational practices of the insurance industry, which benefits everyone.

More than 60 percent of all InsurTech deals have involved companies that specialize in some type of insurance automation. For example, one startup, CynoClaim by Outshared, is enabling 60 percent of claims to be managed automatically through digitization and automation, allowing processes and functions to become cheaper and more efficient.3

Oscar Health Insurance recently partnered with an established insurer, Humana, to blend its technology with an established distribution network. In addition, Oscar pulled in startup and wearable-device company Misfit to reward healthy customers by automatically linking their biometric information to their health insurance. The advantages of embracing InsurTech are clear—it is essential that employee benefits players modernize, collaborate and change.

Startups and Incumbents Working Together

As I mentioned, I have worked in this industry for almost 20 years. We started Limelight Health after years of frustration working as insurance agents in employee benefits and experiencing firsthand the inefficiencies and redundancies in our everyday work. Taking just one area of the workflow—quoting and enrollment, for example—we saw that far too much time was spent on these manual administrative tasks.

So we started with a few simple questions:

- Why is it so hard to simply get a quote from a carrier?

- Why is underwriting so antiquated and “secret?”

- Why is it not easier to explain the products to a customer?

- Why don’t we have a standard to enroll employees?

How do we solve these problems? How do we provide an enjoyable user experience and make these processes efficient? As we began the journey, we quickly found there are very few standards. Due to legacy technology and a lack of access to underwriting and rating logic, building a good user experience and connecting systems is a daunting task.

Purchasing a medical, dental, vision, life, disability or cancer product is one of the most important decisions that directly affects our nation’s workforce. Employee benefits are a major factor for 60 percent of people when considering whether to accept a job offer.4 It seems that health insurance, being so personal and so relevant to most of the general population, would warrant a mutually beneficial, seamless process for which to procure, compare, choose and enroll—with the right data and tools within easy reach of the user.

This brings us back to the initial question: How do we do a better job getting major established players in the insurance industry to embrace and work with early-stage startups? The typical sales cycle can be 18–24 months, and this time can spell death to a startup working on an 18-month cash runway. Often, for example, large carriers need to make decisions with a committee of 20 people. Even when there is an innovation team or a strategy officer, these people are not empowered with the budget and decision-making authority to do a paid pilot or proof of concept. One suggestion is to create an innovation center with its own budget and provide it with a leader who takes lean startup concepts of “failing fast,” and invest in startups with solid proofs of concept that show potential to become full deployments.

The second glaring need is for a common set of standards. It’s been much more difficult than we expected to scale our company because of the lack of nationwide standards for group rate and benefit data. In other sectors, including telecom, banking and FinTech that preceded the current InsurTech transformation, there was an emphasis on creating similar technical standards across the board. As a result, many companies can innovate and provide financial services and solutions with the click of an app because you can connect to every financial institution’s set. It’s impossible to build a technology platform that works for everyone unless there are the infrastructure and standards to support it.

There has been some progress in a few areas with regard to InsurTech. For example, at the public level, health information exchanges, such as the California Integrated Data Exchange (Cal INDEX) and the Statewide Health Information Network of New York (SHIN-NY), are working to gather and share health data with the goal of reducing costs, increasing efficiency and, ultimately, improving the quality of care.

The Meaningful Use standards established by the Centers for Medicare & Medicaid Services (CMS) are another example of the government’s role in promoting data integration. By offering payment incentives to health care providers and organizations, CMS encourages the implementation and “meaningful use” of health care information exchanges and qualified electronic health records (EHRs), among other objectives. While it’s too soon to gauge the program’s full impact, the incentives ultimately should lead to an expanded use of interoperable data, which in turn will support improved care and outcomes. That being said, this pertains to medical records, which is just one aspect of data standards. To my knowledge, there has been little work done when it comes to rating, underwriting and plan availability standards.

Under the Affordable Care Act, which currently is being dismantled slowly, we have public use files for small group medical products when filed by insurance companies. This includes some products like medical, dental and vision. But even this data is not consistent with final sold plans and rates.

Why it Matters

Fifty percent of all bankruptcies happen because someone doesn’t have the ability to pay for medical expenses.5 This is directly related to health insurance coverage. Most people have no clear understanding of how important medical, dental, vision and disability coverage is, and the impact it can have on their lives.

For example, “While about three out of four Americans aged 22–64 believe they know how to use health insurance, only about one in five could correctly calculate how much they owed for a routine doctor visit, according to findings from a national survey by AIR designed to measure health insurance literacy.”6 In addition, we often talk about bringing down the costs of coverage, yet a staggering $400 billion is lost every year to waste and inefficiency, simply as a result of the use of paper records!7

Often, we travel along the path of life with no clear understanding of what coverage we have and what coverage we lack. We typically don’t pay attention until something terrible happens (e.g., an accident, illness or a death of a loved one). A secure health care benefits strategy would help provide some stability while going through hard times with one less thing to worry about. If we don’t work to get standards and provide a better user experience that is data driven, there is no way we will be able to address some of these crucial, often life-changing problems in our industry.

We live in a moment of opportunity. If we, as players in the insurance community, can take a deep breath, dive into the murky waters and work together to find new solutions to these issues, we will be of great benefit to all people as we move toward a tomorrow that promises greater longevity, more automation and a better-informed society.

References:

- 1. “Building a Talent Magnet: How the Property and Casualty Industry Can Solve its People Needs.” McKinsey & Company White Paper. 2010. ↩

- 2. “The Pulse of FinTech Q4 2016: Global Analysis of Investment in FinTech.” KPMG. February 21, 2017. ↩

- 3. De Feniks, Reggy, and Roger Peverelli. “Top 10 InsurTech Trends for 2017.” Insurance ThoughtLeadership.com. January 3, 2017. ↩

- 4. Jones, Kerry. “The Most Desirable Employee Benefits.” Harvard Business Review. February 15, 2017. ↩

- 5. Himmelstein, David U., Deborah Thorne, Elizabeth Warren, and Steffie Woolhandler. “Medical Bankruptcy in the United States, 2007: Results of a National Study.” The American Journal of Medicine, 122 no. 8 (2009): 741–746. ↩

- 6. “How Much Do People Really Know About Their Health Insurance?” American Institutes for Research. October 22, 2014. ↩

- 7. “$375 Billion Wasted on Billing and Health Insurance-Related Paperwork Annually: Study.” Physicians for a National Health Program. January 12, 2015. ↩