China’s Insurers Should Care About Global Climate Change: Part 2

Why China’s insurers must confront global climate-change risk

August 2022Climate change has become a global challenge, and the insurance industry should play an important role in mitigating it and building a greener future. Specifically, insurance products can support sustainable development across industries and exploration of energy-saving technological innovation. Also, insurance funds represent high-volume, long-term investments, which can strongly support green innovation and development, and the transformation of the economy.

As concern about climate change’s impact has spread, companies face stricter guidelines for information disclosure. To meet the new regulatory requirements, the insurance industry can use powerful analysis and decision-making tools for climate-change-risk-related asset and liability management as well as stress testing.

This article is the second of two on the topic of global climate change. Part 1 summarized global climate-change risk issues and some international practices. This article explores ideas and methods that China’s insurance industry can use in carrying out climate-change risk stress testing, so as to help the green and sustainable development of China’s insurance industry.

Principles for climate-change risk stress testing

For the insurance industry, stress testing of climate-change risk includes analysis of the transmission of climate-change impact and identification of possible risk scenarios.

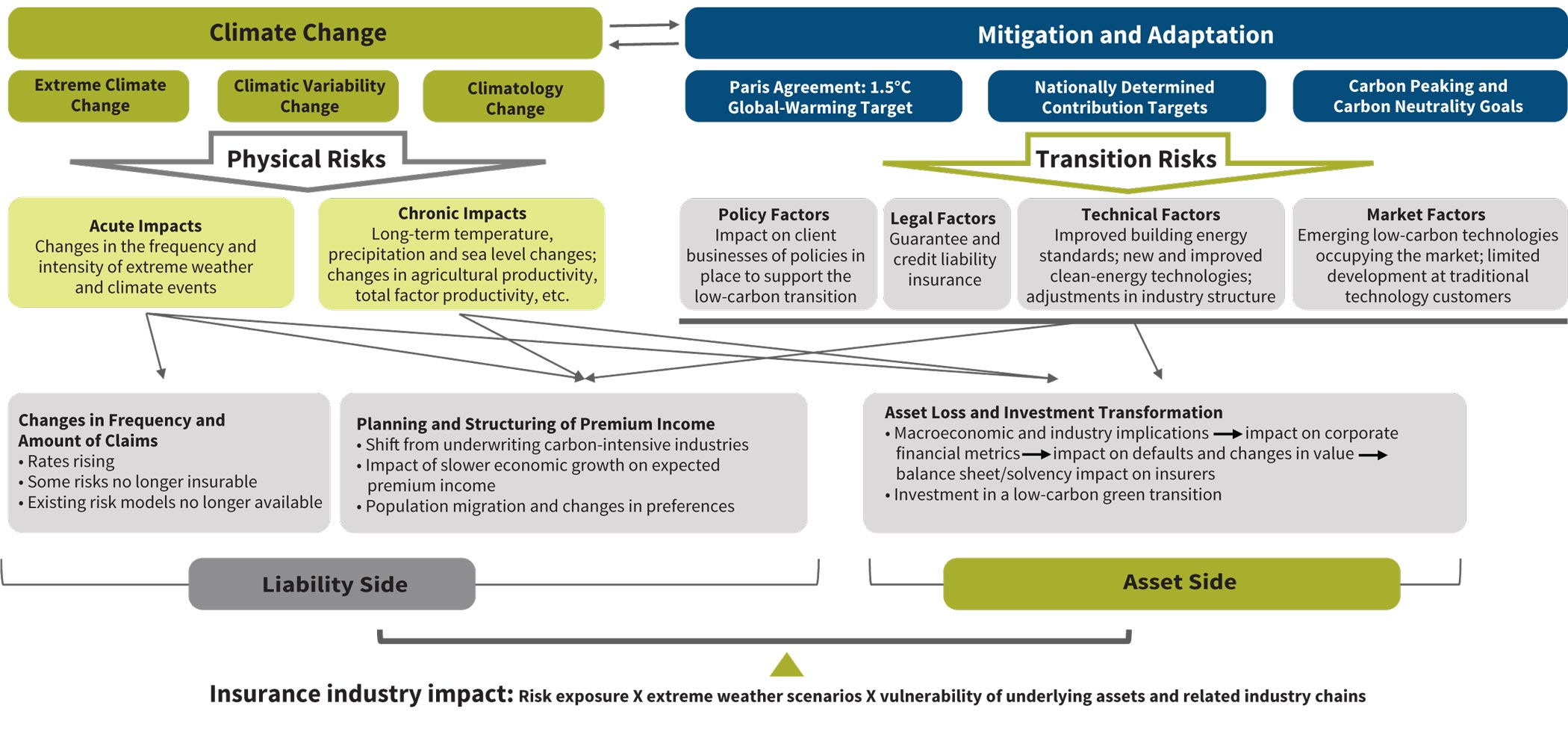

Analysis of the Transmission Path

The impact of climate-change risks on the insurance industry has been discussed around the globe. The main pathways of its impact are divided into “physical” and “transition” risk (see Figure 1). Physical risks involve the impact of climate change on physical assets, including acute risks and chronic risks. Transition risks involve the costs of mitigating and adapting to climate change and are classified according to the areas of the economy and society involved—mainly policies, legislation, technologies and markets.

Figure 1: Conduction Analysis of the Impact of Climate-Change Risks on the Insurance Industry

Physical risks and transition risks will be transmitted to both the asset and liability sides of insurance companies’ balance sheets. Based on the practical experiences of the insurance industry, we find that physical risks are generally of greater concern, followed by transition risks.

Scenario-Setting Framework and Principles

As discussed in part 1 of this series, early efforts at stress-testing climate-change risk in the financial services sector have included guidance on scenario setting by various organizations and use of scenarios by Chinese banks. Building on the international work to develop climate-change risk stress tests, we believe that the scenario setting in China’s insurance industry should focus on the following principles:

- Maintain consistency with the global climate-change and emissions-reduction policy scenarios. The Intergovernmental Panel on Climate Change (IPCC) has developed detailed scenarios for climate-change progression and shared socioeconomic pathways (see Figure 2).1 These five scenarios combine the pace at which greenhouse gas emissions are reduced and various socioeconomic measures such as population and education. Use of the IPCC’s unified overarching framework would be consistent with the general laws of changes in the earth’s climate system. This also would promote the comparison between China’s analytical findings and the results of international studies, contributing to the fruits of global research study.

- Couple the global climate-change scenarios with the climate conditions and energy transition paths specific to China. Climate-change scenarios are closely related to the physical geography, population and economic growth patterns of each region, and climate-change impacts can be reduced with climate-change mitigation and adaptation. The framework of IPCC’s Sixth Assessment Report couples the concentration pathways representing climate change and the shared socioeconomic pathways (SSPs) representing population and socioeconomic growth (column 1 of Figure 2) to establish its global scenarios. In recent years, scholars have carried out the development and application of SSPs in China, focusing on climate factor changes, population and socioeconomic systems, and have estimated future impacts and risks. So far, most of this work has not assessed the cascading impacts of climate-change risks on different sectors of industry, and it is unable to reveal regional and urban-rural differences in impacts. Therefore, the relevant scenarios for China must be set up in a coordinated and unified manner.

- Capture the key risk factors in the Chinese market. In terms of physical risks faced by China, the greatest direct economic losses of meteorological disasters related to climate change from 2004 to 2018 have been those caused by torrential rains and floods (38% of all direct economic losses due to disasters), followed by droughts (24%) and typhoons (20%).2 In terms of transition risks, the energy transformation path designed in combination with China’s latest “double carbon” goal will affect the future performance of high-carbon industries and related industries in the upstream and downstream of the green industry chain, and this will affect the insurance industry’s asset and liability sides as previously detailed in Figure 1.

| Scenario | Near Term

2021–2040 |

Mid-term

2041–2060 |

Long Term

2081–2100 |

|||

| Best estimate (C) | Very likely range (C) | Best estimate (C) | Very likely range (C) | Best estimate (C) | Very likely range (C) | |

| SSP1-1.9: Sustainable practices; high investment in education and health | 1.5 | 1.2–1.7 | 1.6 | 1.2–2.0 | 1.4 | 1.0–1.8 |

| SSP1-2.6: Some cuts to emissions; high investment in education and health | 1.5 | 1.2–1.8 | 1.7 | 1.3–2.2 | 1.8 | 1.3–2.4 |

| SSP2-4.5: Middle-of-the-road scenario | 1.5 | 1.2–1.8 | 2.0 | 1.6–2.5 | 2.7 | 2.1–3.5 |

| SSP3-7.0: Steady increase in emissions; competition among nations | 1.5 | 1.2–1.8 | 2.1 | 1.7–2.6 | 3.6 | 2.8–4.6 |

| SSP5-8.5: Accelerating increase in emissions; high spending on fossil fuel uses | 1.6 | 1.3–1.9 | 2.4 | 1.9–3.0 | 4.4 | 3.3–5.7 |

Sources: IPCC Sixth Assessment Report (Working Group I).

Andrea Januta. “Explainer: The U.N. Climate Report’s Five Futures—Decoded.” Reuters, August 9, 2021.

Analytical methods and tools

The methods and analytical tools used to assess the impact of climate-change risks and related economic impacts on insurance companies can address both the asset and liability sides of the business.

Methods and Tools for the Liability Side

For property and casualty insurance companies, physical risk has a greater impact on their liabilities than transition risk. Property and casualty insurers need to assess whether climate change has been taken into account in pricing, risk management and claims analysis. Stress test models of physical risk often are based on catastrophe models, incorporating some climate-change scenarios. However, in the view of climate-change risks, China’s insurance industry needs to assess the vulnerability of various regions in China subject to the long-term physical risks of ongoing climate change and short-term physical risks caused by severe weather events in different geographical locations.

Changes in the frequency and intensity of extreme weather and climate events caused by physical risks, combined with mitigation measures taken by insured subjects in transition risk scenarios, will affect the frequency and extent of insurance claims. What has been considered a 100-year event may become a 50-year event in the 2050s. Correspondingly, actuarial fair premiums will no longer be “fair.” The catastrophe risk model that the insurance industry relies on needs to be adjusted. It will be difficult for a model that relies solely on statistical patterns of historical events to capture the potential impacts of climate change. In addition, lower macroeconomic growth due to climate change is likely to drive down expectations for premium income growth.

Property and casualty insurance companies generally assess catastrophe risk in terms of frequency of occurrence and degree of damage. Climate change not only affects these two dimensions but also introduces a new dimension: time. Slow and smooth climate change will buy human society more time to adapt to change and take measures, thereby increasing the resilience of the whole system to climate-change risks. The climate physical risk model based on the catastrophe model can be divided into four modules:

- Hazard module. The hazard module simulates possible event scenes, based on realistic parameters and historical data. The parameters may include the specific intensity or size of an event, the location or path, and the probability of occurrence. In different regions, the probability of occurrence of hazard events will be different.

- Vulnerability module. The vulnerability module quantifies the expected losses caused by the risk exposure of the insured target in the risk event.

- Risk exposure module. The risk exposure module needs to consider the composite distribution of urbanization, economic development and demographic structure.

- Financial module. The financial module combines the results of the vulnerability module and the risk exposure module to conduct risk assessment. This provides an important basis upon which enterprises decide what measures to take to reduce the relevant risks.

For life insurance, the impact of physical risk on the liability side is less significant than it is for property insurance companies. In the short term, the impact of physical risk on life insurance companies is small. But in the long run, rising temperatures may be accompanied by increasing incidence of some diseases, such as cardiovascular and respiratory diseases. For insurers, this type of risk is particularly significant for fixed-rate stock health insurance business policies. Insurers that conduct stress testing to set up temperature rise scenarios and project future payments can investigate solutions early.

Methods and Tools for the Asset Side

For the investment business, insurers should analyze the impact of forecast changes in the socioeconomic system on the assets. These changes involve quantitative indicators (such as energy prices, energy demand, carbon prices and land use) as the output of the underlying model. At present, the common underlying models in the financial industry are industry-specific models, macroeconomic models and integrated assessment models (IAMs). Insurers can use existing underlying models directly when constructing transition risk models, and then use the socioeconomic variables output from these models to further assess the impact on key drivers of corporate finances (such as revenue, cost and capital expenditure) in various industries, especially high-carbon industries.

Insurers may refer to international literature such as Case Studies of Environmental Risk Analysis Methodologies, published by the Network for Greening the Financial System (NGFS), to identify quantitative methods to use in analyzing the impacts of transition risk on asset allocation and large-scale assets. Companies can establish related investment research and asset allocation systems based on the company’s climate-change risk. They also can incorporate the relevant indicators of climate-change risk stress tests into their investment decision-making standards and large-scale asset allocation models. Such efforts will reduce the risk exposure of high-carbon emissions and emission reduction. In addition, insurers will be able to select targets with more capacity for becoming low carbon, as well as encourage targets with high emissions to develop their capacity for reducing emissions through due-diligence management, which eventually can minimize the carbon risk of the portfolio without affecting portfolio returns.

How Climate-change risk stress testing helps China’s insurance industry

Climate-change risk stress testing helps China’s insurance industry develop sustainable practices on the liability and asset sides of the business.

Liability-Side Benefits

Climate-change risk stress testing supports insurers in strengthening climate-change risk management and product innovation on the liability side. Based on the analysis process and results of climate-change risk stress testing, insurance companies can strengthen the management measures on the liability side to cope with many changes in climate-change risk and explore opportunities for innovative products.

Here are some of the ways insurers can pursue these benefits:

- Assess the exposure of various types of businesses to climate-change risks, especially those related to agricultural, property and environmental-protection obligations.

- Formulate corresponding business management rules based on geographic climate-change scenarios.

- Optimize reinsurance solutions.

- Appropriately adjust insurance rates and optimize pricing for businesses at risk of climate-change impact.

- Adjust policy renewal rules for subjects with greater climate-change risk.

- Add climate-change risk considerations when underwriting new business, diversifying the regions where underwriting targets are located in combination with the company’s development strategy.

Asset-Side Benefits

Climate-change risk stress testing supports asset allocation. Insurance companies can set climate scenario parameters and corresponding macro scenario parameters through climate-change risk stress testing. They also can identify climate-change risks on the asset side of their balance sheets and organically integrate the climate model results into existing asset allocation and asset liability management models.

Specifically, insurance companies need to analyze the return and risk characteristics of various types of assets, consider regulatory policy constraints and asset constraints, and determine the expected rate of return and risk of assets during the holding period or planned range. Based on the analysis of the impact of climate-change risks on large-scale assets, companies can consider adding the impact of climate-change risk pressures to the expected return rate and risk parameters of large-scale assets. After estimating the rate of return and risk and using optimization techniques to identify the portfolio that offers the highest rate of return at each risk level, the insurer can select the investment alternative according to the target return.

At the portfolio level, the carbon footprint provides an assessment of greenhouse gas emissions associated with a given portfolio, helping to indicate how investments are affected by future climate-change risks. Insurance companies, as investors assessing the risk of the assets they hold, can pay attention to the performance of their assets’ weighted average carbon intensity (WACI). This indicator supports timely adjustment of asset allocation, risk reduction and investment in industries with low WACI, such as new energy and low-carbon industries. Companies also can optimize portfolio carbon risk by adding portfolio-level WACI constraints to existing models.

Recommendations for the Insurance Industry in China

Climate-change risk is the most important systemic risk faced by the insurance industry in the mid and long term; it may profoundly affect the sustainable development of insurance companies on the asset and liability sides. Therefore, those who oversee the industry at the highest levels must promote standards for climate-change risk management. We recommend that regulators or industry organizations promote the formulation of rules for climate-change risk stress testing to enable the sustainable development of China’s insurance industry.

More specifically, China’s insurance regulatory agencies, industry organizations and other institutions should learn from the experience of the international insurance industry and the domestic banking industry in carrying out climate-change risk stress tests. They also should organize the industry and relevant experts to study and select climate-change risk stress test methods and rules for China’s insurance industry. Specific initiatives should include but not be limited to:

- Further sorting out the transmission path of climate-change risks affecting China’s insurance industry, identifying key risks and establishing an analytical framework.

- Setting climate-risk stress scenarios that address China’s climate and economic and social characteristics.

- Developing quantitative model tools for climate-risk stress testing in China’s insurance industry, and then formulating relevant data standards.

- Encouraging the insurance industry to gradually implement information disclosure based on climate-change risk stress testing, asset and liability optimization transformation strategies, and other key measures of progress on sustainability.

The insurance industry has begun pursuing research into climate change and environmental risk scenario analysis and stress testing. Such efforts should continue and include optimization of relevant risk-modeling methods and improvement of data quality. As a result, stress testing will be able to provide substantive guidance for the long-term sustainable development of insurance companies on both the asset and liability sides of the business.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

Notes:

1. Shared socioeconomic pathways (SSPs) are a powerful tool launched by IPCC in 2010 to describe global socioeconomic development scenarios, which are combined with measures of climate-change adaptation and mitigation to assess the challenges facing society in the future. There are currently five typical paths: SSP1 (Sustainability, a sustainable path), SSP2 (Middle of the Road, a middle path), SSP3 (Regional Rivalry, a regional-competition path), SSP4 (Inequality, an unbalanced path) and SSP5 (Fossil-Fueled Development, a path in which development is based on fossil fuels).

2. Calculated with reference to China Meteorological Disaster Yearbook.

Copyright © 2022 by the Society of Actuaries, Chicago, Illinois.