Weather Perils and Carbon Policies

Actuarial insights from climate scenario analysis

November 2023Photo: Shutterstock.com/Piyaset

With risk being a core part of actuarial work, we strive to predict the unknown and minimize unforeseen losses. Despite our hopes for a better “new normal” after COVID-19, the global economy has faced several volatile and complex risk events. These events include bank failures, geopolitical confrontations, energy crises and frequent natural disaster occurrences. The role of insurance in providing financial security has never been more important.

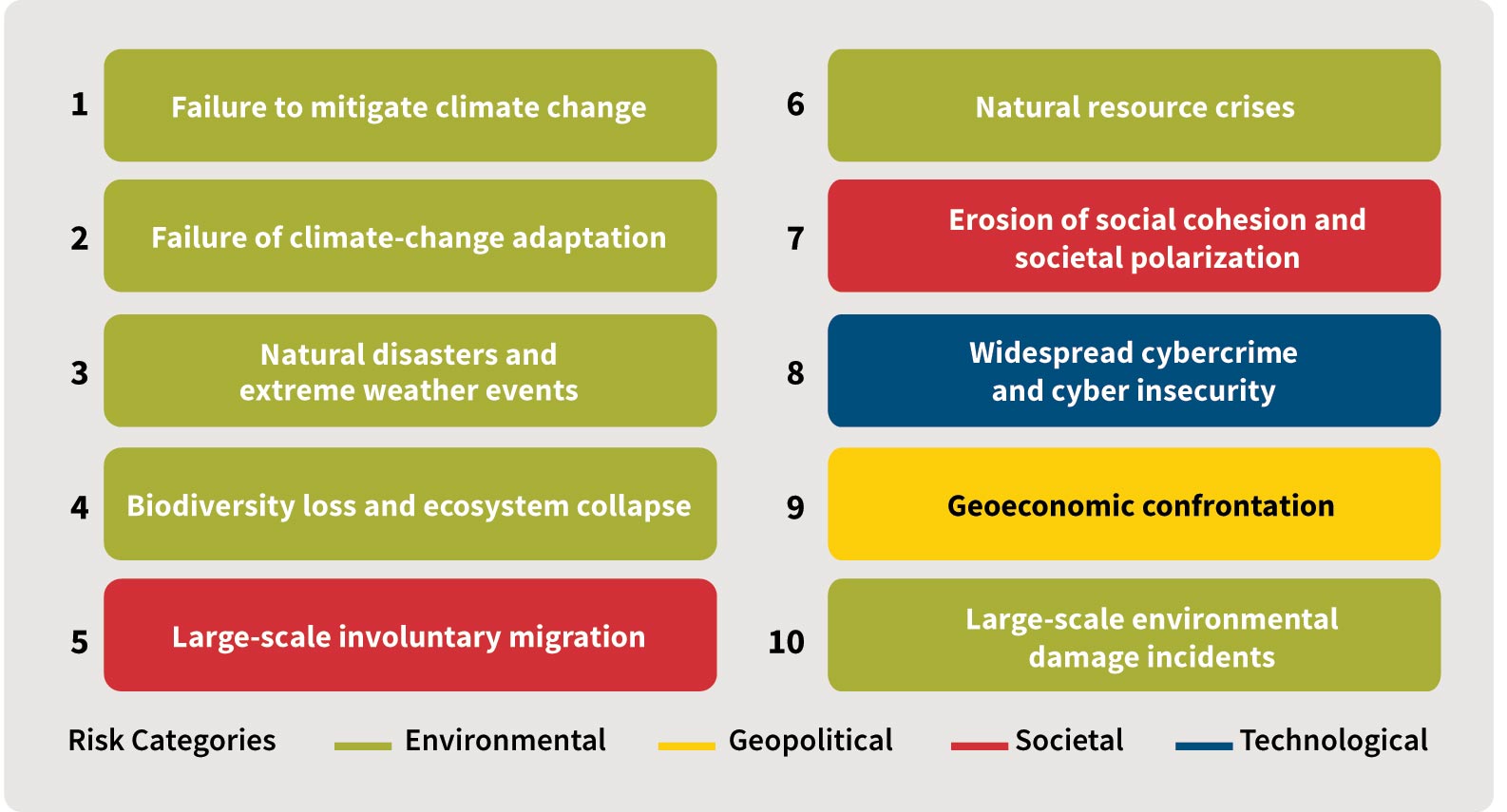

According to a recent survey by the World Economic Forum, global experts anticipate that among all risks, climate-related risks are expected to be most severe in the next decade, as shown in Figure 1.

Affecting the global population, climate change brings about dire impacts such as an increasing number of extreme weather events, food and water shortages, coastal inundation and species loss. The way climate impacts manifest in the insurance sector can vary depending on the area of practice and location. Some examples include the following:

- Deaths and destruction caused by natural catastrophes like typhoons, floods, wildfires and extreme heat or cold

- Long-term health impacts resulting from weather and habitat changes such as air pollution and pandemics

- Rise of sustainable and green investment instruments

- Divestment and losses stemming from investments in high carbon-intensive industries

- Losses from climate-related litigation in relation to directors and officers (D&O) insurance policies

- Financial disclosure on climate risk management

This list is not exhaustive, and we can expect more unforeseeable types of climate impact in the near future accompanied by complex chain reactions and second-order effects. Predicting the evolution of the climate conversation in the coming years is difficult, as it is heavily dependent on governments, companies and citizens advocating for new green policies, technological advancement and zero-carbon commitments.

Explore a Range of Possible Climate Scenarios

With the uncertainty surrounding the timing and severity of climate effects, it is necessary to consider a range of possible scenarios that can challenge current assumptions and inform business decisions. According to the latest survey the Global Association of Risk Professionals (GARP) conducted, more than 80% of global financial firms are now undertaking climate scenario analysis.

There are three commonly referenced climate families published by international public institutions—the Network of Central Banks and Supervisors for Greening the Financial System (NGFS), Intergovernmental Panel on Climate Change (IPCC) and International Energy Agency (IEA)—as shown in Figure 2.

Figure 2: Introduction of Climate Scenarios: NGFS, IPCC and IEA

| Network of Central Banks and Supervisors for Greening the Financial System (NGFS) | Intergovernmental Panel on Climate Change (IPCC) AR6 | International Energy Agency (IEA) | |

| Philosophy and approach | A group of central banks and supervisors, in collaboration with an academic consortium, established NGFS in 2017 to describe scenarios to inform risk management in the financial and private sector. The membership now spans more than 120 banks and supervisors from all continents. | Included in the 6th assessment report from IPCC, the scenarios are constructed from scientific and academic perspectives to inform policymakers with summaries across all scientific assessments on climate change, implications and future risks, and potential adaptation and mitigation options. | Scenarios built from an energy industry perspective to describe future energy trends and corresponding emissions reduction. They define a set of starting conditions (e.g., policies and targets) and describe where they lead based on energy models with market and technology dynamics. |

| Published scenarios

(temperature increase by 2100) |

|

|

|

In the banking and insurance sector, regulators worldwide most commonly reference NGFS scenarios in regulatory climate stress tests, including those in the European Union, United Kingdom, Canada, Hong Kong and Singapore.1 Most climate variables, with breakdowns for more than 180 countries, are readily available and accessible at no cost. With this open-source platform, many companies and regulators build bespoke climate scenarios that incorporate their internal perspectives based on NGFS.

Among the six distinct scenarios in NGFS, three are frequently adopted and provide a broad range of climate outcomes:

- Hot house world scenario based on current policies

- Delayed transition scenario

- Net-zero scenario

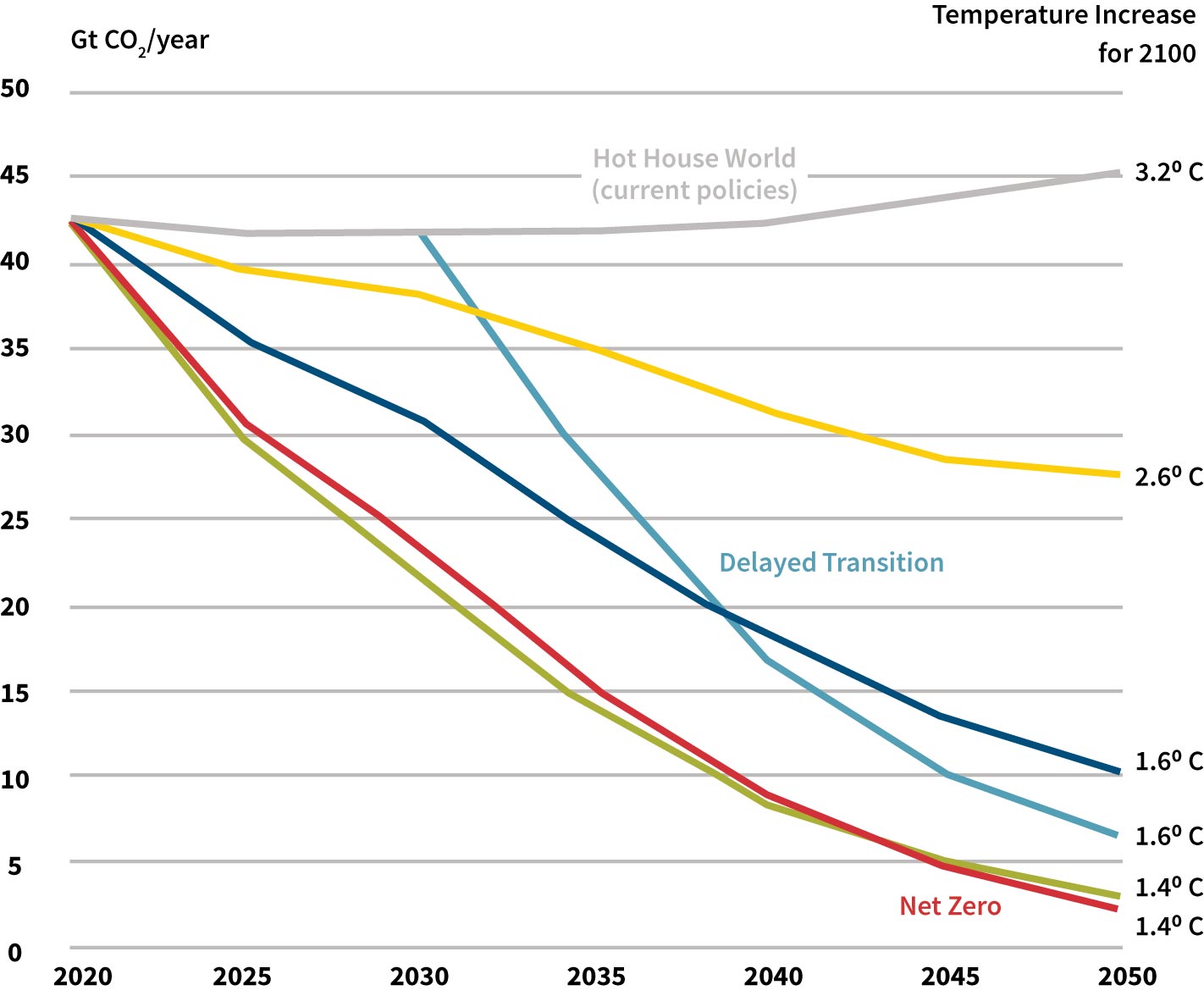

The narratives surrounding these popular scenarios are shown in Figures 3 and 4.

Figure 3: CO2 Emissions by Scenario

Figure 4: Carbon Emission Pathways and Narratives of NGFS Scenarios

| Scenario | Narratives |

| Hot House World

Current policies (3.2°C) |

Only currently implemented policies are preserved, with slow technological changes and minimal carbon price. Global efforts are insufficient to halt global warming and sea level rise. |

| Delayed Transition

(1.6°C) |

Annual emissions do not decrease until 2030, when stringent and disruptive climate policies like carbon taxes and restrictions on high-emission industries are introduced. |

| Net Zero

(1.4°C) |

Progressive and gradual climate policies are introduced early with innovation in carbon capture and removal. Global net zero is reached by 2050. |

Under each scenario, the manifestation of climate impacts will vary:

- Under scenarios characterized by higher temperature increases and limited policy intervention (e.g., hot house world scenario), there is a higher physical risk. This risk relates to potential damage to assets and loss of lives resulting from more frequent and severe weather events.

- Under scenarios characterized by lower temperature increase and stringent policy intervention (e.g., net-zero scenario), there is a higher transition risk. This risk relates to potential loss incurred due to carbon pricing and policy changes implemented in response to climate change.

Model Physical Risk Under Extreme Weather Events

No matter which scenario we use in the analysis, there will be distinct trajectories for various weather parameters such as rainfall, temperature and sea level. To evaluate the effects of physical risks, we need to translate these trajectories into parameters that represent the changes in frequency and severity of extreme weather perils, called peril parameters.

This enters the realm of natural catastrophe modeling, which relies on global and regional climate models. These models simulate weather patterns over time by solving equations that represent the processes and interactions governing Earth’s climate. Regional models, being more accurate and precise than global models, allow us to focus on common perils in specific parts of the world. For example, regions in Asia are more prone to tropical cyclones, while the United States is more prone to forest fires and hurricanes.

After inputting the weather parameters into the models, we can forecast how climate change increases the frequency of extreme weather perils:

- Increase in rainfall and sea level will lead to more floods

- Increase in air temperature and humidity will lead to more wildfires

- Increase in sea temperature will lead to more tropical cyclones

To complete the analysis, we also need to assess how these events will affect the insured assets and estimate the severity of losses. Take the property sector, for example. The impact will manifest in direct property damage and business interruption. The projection can be made by examining the property archetype, determining respective restoration costs and referencing historical data on the duration of business interruption during similar extreme weather events.

Different buildings—such as houses, apartments and commercial skyscrapers—exhibit varying levels of resilience to flooding and extreme winds. Location also matters, as coastal areas are more susceptible to coastal floods and cyclones. Considering these characteristics when conducting climate stress tests for a diverse portfolio is crucial.

Model Transition Risk Under Carbon Pricing and Policies

With the introduction of the carbon tax and government interventions aimed at achieving carbon neutrality, insurers likely will face investment losses in high carbon-intensive industries such as oil and gas, power generation, metals and mining, and others. The U.K. regulatory climate stress test results in 2021 indicate that insurers’ asset value could decline by up to 15% by 2050. This decrease is due to the devaluation of equity holdings and credit downgrades and defaults in corporate bond portfolios.

Given the varying pace of transition across companies, industries and markets, a bottom-up approach can be used to model transition risk within an insurer’s investment portfolio. This involves examining each counterparty and projecting its future profit and loss by considering the following factors:

- Company financials and carbon emissions data

- Carbon price and sector price elasticity (how easy it is to pass on carbon costs to customers)

- Company transition plans and carbon targets

- Sector-specific considerations (e.g., product type, fuel mix and price, technology level, etc.)

Since transition affects each sector differently, it is better to employ customized calculation models for each carbon-intensive sector. For instance, models for the oil and gas and power generation sectors would focus primarily on fossil fuel reserves and renewable energy uptake as key drivers. On the other hand, the automotive sector model would consider battery technology and electric vehicle adoption as key drivers.

Once we have projected the profit and loss for the counterparties, the stress test calculations can proceed as usual. This entails projecting defaults for corporate bonds and evaluating potential declines in the value of equity holdings.

Case Studies From Insurers

Following the widely recognized climate disclosure framework, Task Force on Climate-Related Financial Disclosures (TCFD), insurers from various jurisdictions have been actively disclosing their efforts in regulatory and in-house climate scenario analysis in annual sustainability reports. Here are some recent examples of developments and commitments made by insurers:

Allianz

Disclosed in its latest sustainability report, Allianz has performed climate scenario analysis with time horizons extending up to 2050 that encompass a range of scenarios from 1.5°C to 4°C of average warming by the end of the century. The report highlights key results, including impact on its investment portfolio with projected market value losses of around 9.0% by 2025. Allianz also discloses property and casualty (P&C) losses of up to EUR 100 million and life and health (L&H) losses of up to EUR 60 million under the most extreme physical risk scenario. Allianz will continue decarbonizing its investment and insurance portfolios, reaching net-zero greenhouse gas (GHG) emissions by 2050.

AXA

Disclosed in its latest climate report and another on climate and biodiversity, AXA participated in regulatory climate stress tests, including those from the Prudential Regulation Authority (PRA) in the United Kingdom and the Autorité de contrôle prudentiel et de résolution (ACPR) in France. The company has utilized three scenarios with different climate pathways with varying levels of physical and transition risks. Internally, AXA forecasted a maximum potential loss of 9.5% in the market value of its investment portfolio under the scenario with high transition risk within a 15-year time frame.

Looking ahead, the company has committed not to make new direct investments in listed equities and corporate bonds of oil and gas companies in developed markets. AXA aims to expand its insurance business in the field of renewable energies. The company also has incorporated considerations of physical risk impact into its pricing and capital modeling work.

The Way Forward

The practice of climate scenario analysis is gaining momentum rapidly in the insurance industry. Regulatory climate stress tests are becoming more common, with the European Union now preparing for its first climate stress test, which includes the insurance sector. TCFD is mandatory in jurisdictions like the United Kingdom, New Zealand and Singapore. Climate risk also is expected to be incorporated into own risk and solvency assessment (ORSA) frameworks.

The topic of climate risk transcends boundaries and is on the mind of not just investors but also employees, governments and consumers. It resonates strongly with younger generations who understand the urgent need for action. Collectively, we can pave the way toward a cleaner and more sustainable world by harnessing our expertise and embracing sustainability.

Jan Hou Chong, FSA, served as contributing editor for this article.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

References:

Copyright © 2023 by the Society of Actuaries, Chicago, Illinois.