Bridging the Gap

Financial literacy across generations in Canada

November 2025Photo credit: Shutterstock/Thinkhubstudio

November marks Financial Literacy Month in Canada—a timely reminder that, despite unprecedented access to financial information, many Canadians still struggle to make informed decisions, and the gaps vary sharply by age. And while financial decisions are a constant across one’s lifetime, the knowledge needed to navigate them is anything but uniform. From the 25-year-old entering the workforce to the 65-year-old planning how to withdraw retirement savings, Canadians face vastly different financial landscapes shaped by generational circumstances, digital fluency and evolving economic pressures.

Recognizing diverse needs and methods of communication and tailoring financial literacy initiatives to each generation can help Canadians achieve long-term financial security in ways that are most relevant to their circumstances.

Understanding the generational divide

While there is no one-size-fits-all approach to financial education, generational cohorts tend to share common economic pressures and knowledge gaps. Recognizing these differences is essential to developing effective, targeted financial literacy strategies.

Gen Z (born 1997–2012): Digital, with debt tendencies

This generation is tech-savvy, socially connected and intent on learning from the previous generations’ lessons. Many are entering adulthood and the workforce, taking on numerous financial firsts, like purchasing groceries or paying rent at an all-time high cost of living, according to data from Statistics Canada. Social media is a key source of financial information and advice, and the rise of influencers presents both risk and opportunity.

Millennials (born 1981–1996): Stretched and searching

Millennials are navigating high housing costs, student debt and childcare expenses while trying to save for retirement. Many are unsure how to balance paying down debt with investing, having taken on the largest amount of debt in comparison to other generations. 1

Gen X (born 1965–1980): The financial sandwich

This group is often juggling the cost of supporting both children and aging parents, all while falling behind on their own retirement savings. Despite higher income levels, wealth accumulation lags behind that of other generations and financial confidence is low.2

Boomers (born 1946–1964): Decumulation decisions

Many boomers have accumulated wealth but are unsure how to decumulate (turn retirement savings into income after you stop working) it efficiently. The complexities of retirement income streams, withdrawals of retirement savings, annuity options, as well as Canada/Quebec Pension Plan (C/QPP) and Old Age Security (OAS) deferrals, can be overwhelming. This generation is also, as reports show, disproportionately vulnerable to financial fraud, especially online, due to gaps in digital literacy.

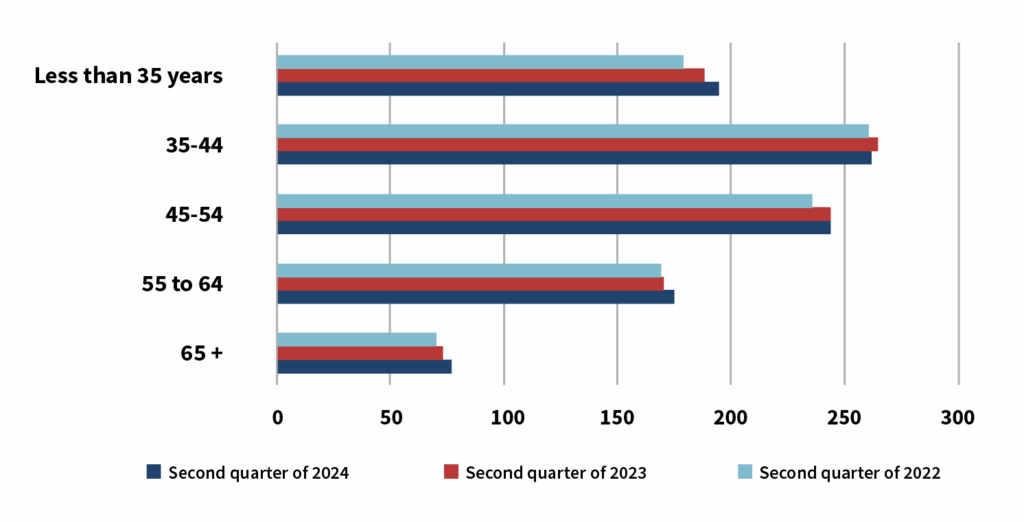

Affordability across generations

Many of the above trends can be seen in the differing debt-to-income ratios of the various age groups.

Figure 1: Debt-to-income ratio by age group

Source: Statistics Canada

The debt-to-income ratio increases with each generation, with millennials’ ratio about four times that of baby boomers. This is largely attributable to the increase in the cost of home ownership compared to salaries over the years. 3

Gen Zers are the anomaly to this pattern. Although debt-prone, many have been priced out of the current housing market and instead are turning to investing. In fact, as reports show, Gen Zers invest consistently each year, more than any other age group, and contribute greater amounts toward retirement than their millennial counterparts.

Millennials are often the most impacted by affordability challenges. Many millennials entered the workforce facing the dual challenges of large student debt and limited wage growth related to the 2008 financial crisis. As housing prices surged in the 2010s and early 2020s, those without an early foothold in real estate found themselves needing larger down payments just to enter the market, leaving many to rent longer, only to see housing prices continue to increase.

Stagnating wage growth during the financial crisis also impacted Gen Xers at a time when they were in their 30s and 40s, entering managerial roles and would generally have anticipated a sharp increase in earnings. This is often the age when individuals can turn their financial attention to investing. When the baby boomers were in their 30s, in the 1980s, global stock markets quadrupled. Millennials, now in their 30s, have seen a strong market over the last few years. Gen Xers, however, saw a dip in equity markets in the early 2000s after the dotcom bubble burst, followed by the financial crisis later that decade. These factors have contributed to Gen Xers lagging in wealth accumulation.4

Baby boomers, on the other hand, face unique affordability challenges in retirement, despite generally having more wealth than younger generations. While many benefited from favorable housing markets and lower costs of living in their younger years, they now face rising healthcare costs and the potential need for long-term care while navigating how to draw down retirement assets. Boomers need to manage the risk of outliving their assets while also ensuring they have the ability to access funds as needs arise, in order to address long-term care and other costs.

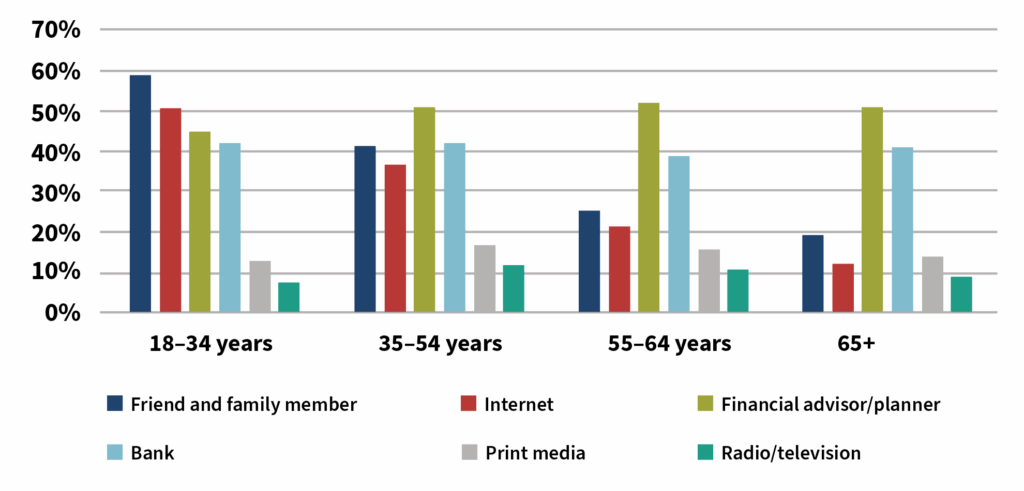

Tailored financial literacy strategies

Maximizing financial education effectiveness means meeting Canadians where they are, communicating in a way that resonates with each cohort, and creating age-specific tools and resources.

Figure 2: Canadians’ preferred source of financial advice, by age group

Source: Government of Canada

Younger Canadians between the ages of 18 and 34 are more likely to seek financial advice from friends or family members, or by relying on the internet, social media and influencers for financial advice, giving rise to the term “finfluencers” (financial influencers). Finfluencers often break down complex investment jargon into easier, more digestible concepts, making things less overwhelming. However, finfluencer content can often lack any disclosure and include high levels of promotion, so finding a credible source is important.5

Podcasts are another popular method among Gen Zers and millennials (as well as this Gen Xer). A podcast released earlier this year by a seasoned financial advisor boomer and his Gen Z daughter, “Am I Rich Yet?” is described as “a weekly podcast for millennials and Gen Zers where we teach you how to save, spend, and grow your money smarter.” In preparing the topics for the podcast, questions were gathered from a survey of about 100 Gen Zers. Each episode is approximately 15 minutes long and covers topics like goals and budgeting, debt and savings, investing, credit cards, housing, real estate decisions, taxes and lifestyle choices. The tag-team approach aims to ensure messages and advice are clear and relatable to the target audience.

Gen Xers and baby boomers predominantly seek advice from financial advisors or their bank. The Each One, Teach One (EOTO) program, which is managed by the Canadian Credit Union Association, trains employees of Canadian credit unions to deliver financial education workshops in their communities. Workshops are delivered in plain language without any ties to products or services, with the sole goal of empowering Canadians to take control of their financial decisions and plans. Workshops include Introduction to Basic Budgeting, Introduction to Registered Education Savings Plans (RESPs), Home Readiness and Financial Wellness for Seniors.

Cross-generational financial well-being

While each generation faces unique financial turning points, several key themes are common across all age groups when it comes to financial wellbeing: Having a clear understanding of financial well-being is essential—being able to meet current and future financial obligations, feel secure about one’s financial future and make choices that allow enjoyment of life.

Studies show a strong link between financial well-being and personal well-being: Financially prepared individuals tend to feel more resilient and optimistic about the future. For younger Canadians, financial well-being might mean managing debt while building savings; for mid-career individuals, balancing competing financial priorities; and for older adults, ensuring income sustainability in retirement. Despite these differences, the core elements of budgeting, saving, borrowing, investing, and spending remain consistent across all generations.

All generations face key life events and with them, critical financial decisions. Whether it’s entering the workforce, buying a home, raising children or navigating retirement, each stage presents crucial decision points that can significantly influence long-term financial outcomes. The availability of timely, relevant and trusted financial education in a digestible format during these life events can greatly impact financial and personal well-being.

Supporting financial literacy early on

Building financial capabilities would ideally start early, and schools could play a critical role in setting the foundation. Across Canada, provinces are expanding financial literacy education in elementary and high schools and embedding topics such as budgeting, borrowing, and rental costs in math and career courses.

In addition to building financial resilience, numerical literacy equips Canadian youth with the skills to interpret data, compare quantities and understand proportions—abilities that are essential for nutritional decision-making. These skills can help youths read food labels, calculate portion sizes and assess the nutritional value of meals. By strengthening their comfort with numbers, young Canadians gain the confidence to make informed choices that support both their physical health and financial well-being.

From knowledge gaps to financial confidence

FOR MORE

Read The Actuary article “Financially Literate?”

Financial literacy is more than a life skill; it is a foundation for stability, resilience and opportunity. As economic conditions, technology, and life stages evolve, knowledge and skills can play an important role in helping Canadians navigate these shifts.

Financial literacy can help Canadians make informed, confident decisions at every stage of life by helping to bridge generational knowledge gaps. This may help strengthen individual outcomes and potentially contribute to the financial resilience and well-being of society as a whole.

Statements of fact and opinions expressed herein are those of the individual authors and are not necessarily those of the Society of Actuaries or the respective authors’ employers.

References:

- 1. Greer, Darryl. Why millennials in Canada are hardest hit by debt. The Canadian Press, March 2023, https://globalnews.ca/news/9579531/millennials-debt-canada/(accessed September 1, 2025) ↩

- 2. Ipsos. Canadians Settling into Stability But Remain Concerned About the Future. IG Wealth Management Financial Confidence Index, November 2024, https://www.ipsos.com/en-ca/2024-ig-financial-confidence-index (accessed September 1, 2025) ↩

- 3. Alini, Erica. Here’s how home prices compare to incomes across Canada. Global News, April 2021, https://globalnews.ca/news/7740756/home-prices-compared-to-income-across-canada/ (accessed September 1, 2025) ↩

- 4. Donnelly, Alan. Understanding the Dot-com bubble and Its Lasting Impact. CGAA, August 2025, Exploring the Dot-com Bubble and Its Long-lasting Effects (accessed September 22, 2025) ↩

- 5. Espeute, Serena, and Rhodri Preece. The Finfluencer Appeal: Investing in the Age of Social Media. CFA Institute of Research & Policy Center, January 2024, https://rpc.cfainstitute.org/sites/default/files/-/media/documents/article/industry-research/finfluencer-report.pdf (accessed September 22, 2025) ↩

Copyright © 2025 by the Society of Actuaries, Chicago, Illinois.