Modernizing the Life Insurance Buying Process

How century-old insurance companies are transitioning to a digital experience

October 2020Photo: Shutterstock.com/alphaspirit

Across the life insurance industry, the purchasing process has remained largely unchanged for decades, relying on lengthy processes, complicated paperwork and invasive medical requirements. As a case study on how established firms are transforming their platforms and customer experience, Penn Mutual (established in 1847) focuses on its Accelerated Client Experience (ACE) effort to modernize the drawn-out life insurance purchasing process and create a concise digital experience.

Background

Similar to many companies across the industry, Penn Mutual’s life insurance business was—until August 2017—submitted via paper application. That paper application process generally follows this timeline, which likely resonates with those who have applied for life insurance in the past:

- After consultation with a financial professional, a client decides to apply for life insurance.

- The application process begins with the financial professional completing a paper application and submitting it to the insurer’s office, often by mail, fax or an email attachment.

- Sometimes applications need clarification or additional documentation. This is communicated to the financial professional and then to the client, often adding days to the application review.

- Following paper submission and review, the financial professional and client schedule a paramedical exam.

- A qualified medical personnel visits the applicant in-person to complete a medical questionnaire, capture height and weight measurements, and collect blood and urine samples for lab testing.

- Then there is a wait to receive lab results, which are presented to an underwriter for review. The average time for an underwriting decision is 21 days.

In this traditional process, once the underwriting decision is made, Penn Mutual issues the life insurance policy, prints and mails it to the respective field office, and then sends it to the financial professional. The financial professional would then set up another meeting with the client to sign and return the policy with payment. At this point, it is about 40 days into the process of buying life insurance.

Penn Mutual recognized an opportunity to modernize the purchasing experience to be more responsive to the fast-paced lifestyles of consumers today. ACE transformed all aspects of Penn Mutual’s process to a digital business model. The insurance buying experience is now seamless, fully integrated and inclusive of application, underwriting, electronic signature and payment. What’s more, it also provides a transition to policyholder service through an online client portal.

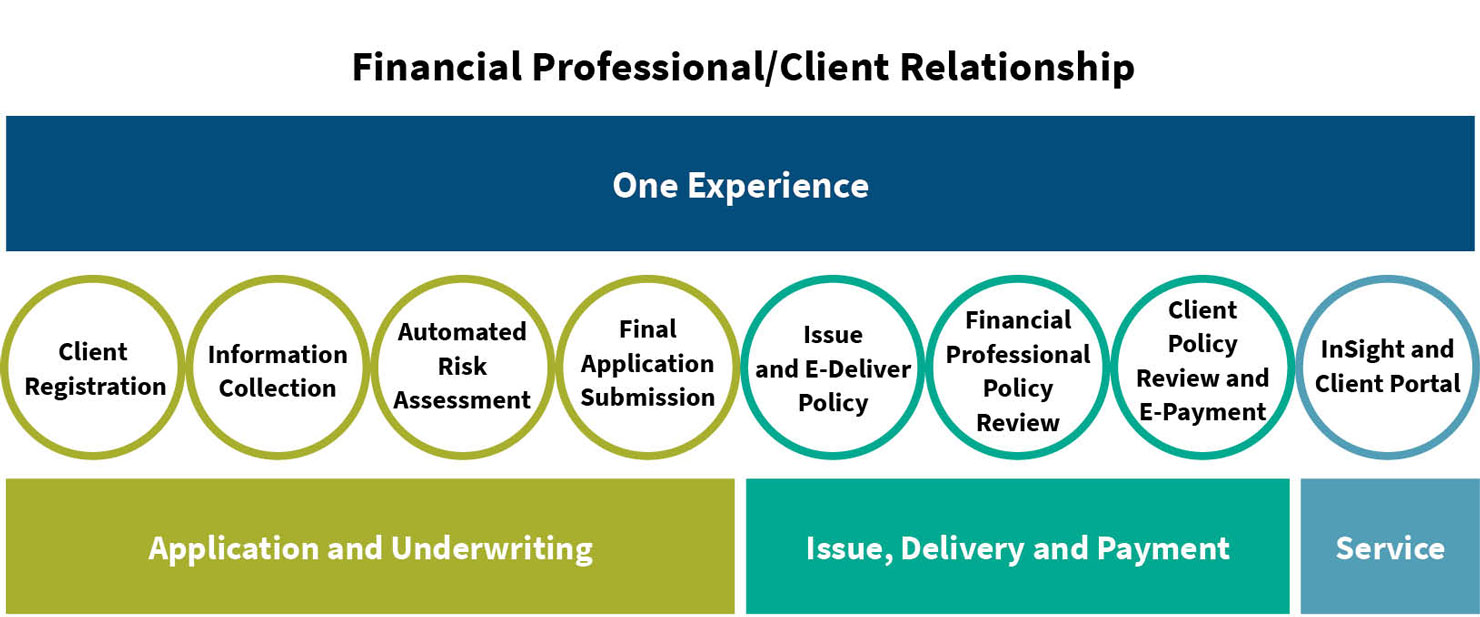

Figure 1: Re-imagining the Experience We Deliver

Source: Penn Mutual

The ACE purchasing experience has greatly reduced the time involved in the life insurance buying process from start to finish. An invasive, multiweek process is now a completely digital experience that can take just a few hours for eligible applicants, providing a fast and simple process for both financial professionals and their clients. This new digital experience reduces cost, minimizes overhead and accelerates the entire process.

The Path to Achievement

In 2016, Penn Mutual discussed bringing the ACE concept to life and established a goal to develop the digital platform and launch it in the summer of 2017. Because ACE spanned the entire purchase process from application to payment and client servicing, Penn Mutual leveraged an agile methodology across seven internal agile teams. Executives were actively engaged throughout the development and delivery processes, regularly participating in demonstrations, offering feedback and removing impediments. With help from external partners, the life insurance purchasing process for Penn Mutual was reimagined within 14 months at a fraction of the cost typically incurred in such transformative initiatives.

An internal team built a framework to enable connectivity and seamless communication across all vendor platforms. Outside help was brought in to re-envision the e-Application and the e-Signature processes. Hannover Re partnered with us to facilitate automated underwriting, and illustration integration into e-Application required support from our illustration vendor. We engaged a fourth vendor for e-Delivery, with a bank providing online payment services.

Simplifying the experience for financial professionals and clients required challenging preconceived notions and long-standing practices. Establishing this untried vision across the organization had to be a deliberate effort. The teams shifted their mindsets to focus on a forward-looking, innovative customer experience.

Shifting our processes was challenging initially, but our company’s culture provided a safe, high-performing environment that encouraged risk-taking. The sheer breadth of the endeavor alone resulted in challenges, and those were compounded by collaborating with partners who leveraged independent implementation methodologies that did not align with our “agile sprints.”

These challenges were mitigated primarily by our most important success factor: clear articulation of ACE as a top priority. Teams were empowered to make decisions and move forward, and all levels of leadership supported them in doing so. A continuous dialogue with vendor partners and across our internal teams allowed us to manage the varying approaches, and consultation with our field partners helped formulate the training plan.

With a targeted delivery date only 12 to 18 months from the project kickoff, we employed a completely agile approach, and our mindset was oriented to deliver a “minimum viable experience.” Program goals and features were organized by what was needed now, next and later. Teams worked to meet the now needs first, while stakeholders established next and later priorities.

In August 2017 (about one year after kickoff), the life insurance purchasing process transformed into a complete digital experience with:

- Electronic application data capture

- Illustration integration

- Data-driven automated underwriting

- Automated policy processing and issue

- Electronic delivery and signature

- Electronic payment

- Servicing in a new online client portal

To launch, a staged rollout was implemented, starting with an initial release to a few select agencies. The initial release was successful enough that a continuous rollout model was adopted based on demand from financial professionals and their desire for their clients to use these new capabilities. Initially, the minimum viable product included our top four products, was available in 43 states and only required that the policyowner be named as the insured on the policy.

Success Metrics

The goal of ACE is to be an industry leader in the purchasing and ongoing experience of life insurance—simplifying the buying process for financial professionals and their clients. Penn Mutual has a commitment to continuous improvement based on financial professional feedback, internal goals and its list of priorities. No different than an app or operating system on your phone, we make regular updates to the functionality of the program. So far, 100+ updates have been produced.

All of the firm’s life insurance business can now be submitted via ACE, and adoption and satisfaction is the truest test of success. As of August 2020, 85 percent of all life insurance applications are running through a platform that has reduced the entire life insurance purchase process from weeks to days, including same-day issuing in some cases (see Figure 2). We created an experience that is powered by people and enabled through technology.

Figure 2: Penn Mutual Life Insurance Applications: Paper vs. ACE

Hover Over Image for Specific Data

Source: Penn Mutual

In addition to financial professional adoption and satisfaction, Penn Mutual has:

- Improved new business and underwriting processing speed

- Reduced new business and underwriting expenses

- Achieved a placement rate greater than 90 percent for accelerated cases

- Continued an increase in life insurance premium, face amount and policy count

- Consistent automated underwriting rate class decisions

Financial professional testimony is a strong indicator of the benefits of the new process. Multiple financial professionals have called ACE a “game-changer.” Because of the accelerated process, financial professionals can expand their reach and provide solutions to a broader market and customer base.

The success of ACE can be boiled down to broad organizational support and a clear articulation of ACE as a top priority for the company. We established a shared vision of experience that included financial professionals and their clients in the design process. It was important to build the product in a fun environment that welcomed collaboration and supported risk-taking. Rather than just releasing a digital product, the focus was on producing a digital “experience,” with an eye on future development using the aforementioned now, next and later guides.

Automated Underwriting

One of our teams focuses on the underwriting component within the transformed life insurance purchasing experience. We partner with Hannover Re and utilize its ReFlex underwriting system. At the launch of ACE, 15 percent of applicants received an automated underwriting decision (a rate class confirmation with no human underwriter review). Using data analytics along with underwriter and financial professional feedback, the underwriting team knows where to direct focus and efforts.

After three years, we’re now using the 16th version of the ACE underwriting system. Significant adaptations to the reflexive underwriting questions and enhancements to the underwriting rules were made—all to improve the client experience. This has helped grow the number of applicants who receive an automated underwriting decision from 15 percent to 30 percent.

All of this has been done with a small team of actuaries, underwriters, a medical doctor and technology associates who are all keenly aware of the goals. More important, the team members are empowered to make decisions and execute those goals. Human intuition continues to be a part of the process. Data is not followed to an endpoint, and the answers coming from the model are consistently challenged as the team keeps asking “why?”

Our company continually reviews new data and risk scoring that could be used in underwriting. Mortality scores, electronic health records and so on are considered in the analysis. It is key to continue to have a relationship and communication with reinsurers, data providers, InsurTech companies and others as the landscape of ideas continues to evolve rapidly.

While analyzing external data sources, internal data also is reviewed. For example, prescription data is received electronically from a vendor, which then is provided to an underwriter in a PDF format. Using this data, an internal prescription model was implemented as part of our ACE underwriting system, which played a part in increasing the percentage of applicants who receive an automated underwriting decision.

Why did our organization do this? After analyzing external prescription data rules and scores, the analysis concluded they worked well for low-risk and high-risk prescription drugs, but they were poor at analyzing moderate-risk drugs, where a large percentage of our applicants fit in. Applicants were back-tested, and the model did a better job of grouping people and their prescriptions into concerning and nonconcerning groups. This is a win-win: Better-expected mortality than our original prescription rules is expected, and more applicants can receive an automated underwriting decision. The model runs in real-time and uses machine learning.

Another predictive underwriting model that is part of the ACE underwriting system also uses real-time underwriting data, and it identifies applicants eligible for fluidless (no blood or urine testing) underwriting prior to their application submission. Those applicants are eligible for a same-day review by a human underwriter. This allows financial professionals to better set expectations with their clients on the next steps of the life insurance purchasing experience. Ninety-nine percent of the time, there are no further medical requirements needed outside of a few clarifying questions. This is a good example of technology and humans working together to balance the client experience and risk selection process.

Looking to the Future

A major challenge for actuaries and underwriters alike is to keep pace with technological and medical advances. The exponential growth in data and computing technology is likely to continue. Within the next decade, wearable devices and digital health data are set to transform the underwriting risk assessment process. Other changes such as epigenetics, nanotechnology and inventions that cannot yet even be imagined will be important in assessing risk factors in the future.

Companies are asking if cases can be fully underwritten with no information from the client other than their identity, and life insurance companies are motivated to continue to work on these big challenges. The industry continues to explore new data, technology and predictive models to transform the life insurance buying process.

Copyright © 2020 by the Society of Actuaries, Chicago, Illinois.